What is compound interest? A simple compound interest definition is that it’s a foundational concept in finance, and truly understanding it is a key part of building long-term wealth. Whether you’re saving for retirement, investing in the stock market, or trading forex, understanding what compound interest is and how it works can help you make smarter financial decisions.

In this beginner’s guide, H2T Funding will break down what is compound interest, how it’s calculated, how it compares to simple interest, and why starting early can make a big difference. Let’s break down how it works.

Key takeaways

- Compound interest is the process of earning interest on both the original principal and the accumulated interest.

- The formula of compounding is A=P(1+r/n)^nt, and more frequent compounding leads to faster growth.

- It helps outpace inflation, build long-term goals (retirement, home), and stretch savings, yet can also magnify debt on credit cards/loans.

- Using calculators, spreadsheets, or budgeting apps makes it easier to plan and apply compound interest effectively.

1. What is compound interest?

Before we get into formulas and calculations, let’s begin with the basics: what is compound interest definition?

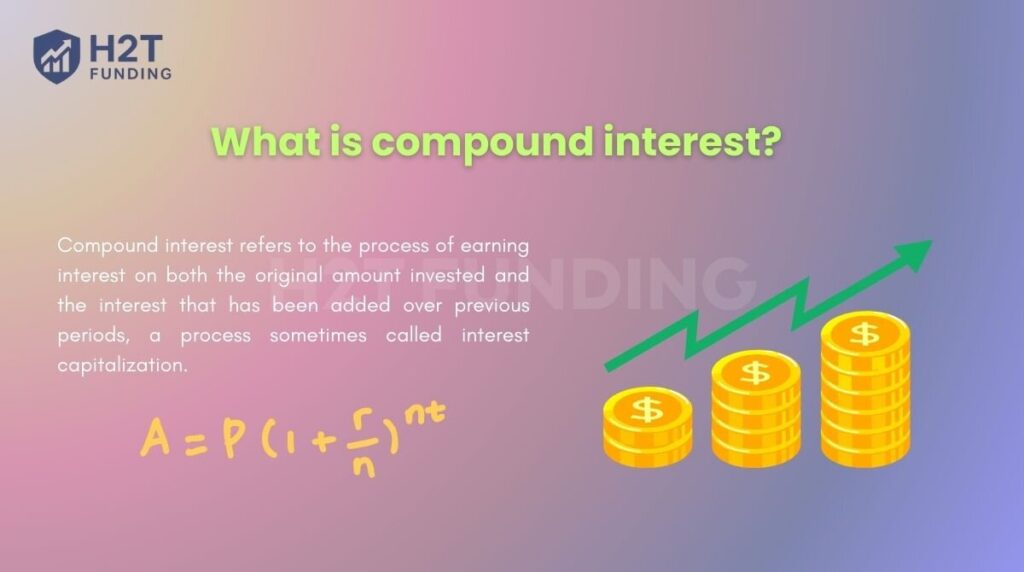

Compound interest refers to the process of earning interest on both the original amount invested and the interest that has been added over previous periods, a process sometimes called interest capitalization. This is where your earnings start generating their own earnings, creating a snowball effect that picks up speed over time.

Put simply, the longer your money is working for you in a compounding account, the more dramatic the growth curve becomes.

1.1. Other terms you might come across

Compound interest is often referred to in several different ways, including:

- Compounding interest

- Compounding of interest

- Compounded interest

- A compound interest system

These terms all describe the same fundamental idea: reinvesting earned interest to grow your total returns over time.

1.2. A simple example

Imagine you put $1,000 into an investment that earns 10% interest per year.

- In Year 1, you earn $100, so your total becomes $1,100.

- In Year 2, you earn 10% of $1,100 ($110), so your total becomes $1,210.

- In Year 3, you earn 10% of $1,210 ($121), and so on.

Instead of earning just $100 each year (as with simple interest), your earnings increase each year because the interest is calculated on a growing balance.

2. How does compound interest work?

Compound interest means your money grows not only from the original principal but also from the returns accumulated over time. Unlike simple interest, this reinvestment creates exponential growth that can significantly boost wealth when combined with consistency and time.

To grasp it fully, let’s explore how earnings build on past gains and how compounding appears in different financial contexts below.

2.1. The idea of earning interest on previously accumulated interest

The core idea behind compounding interest is that the interest you earn each period is added to your original investment (the principal), and in the next period, you earn interest on this new, larger balance. This process repeats, causing your investment to grow at an accelerating pace.

Here’s a straightforward example to help explain:

| Year | Starting Balance | Interest (10%) | Ending Balance |

|---|---|---|---|

| 1 | $1,000 | $100 | $1,100 |

| 2 | $1,100 | $110 | $1,210 |

| 3 | $1,210 | $121 | $1,331 |

| 4 | $1,331 | $133.10 | $1,464.10 |

Explanation: Each year, the interest is added to the balance. In year 2, you earn 10% on $1,100 (not just the original $1,000), and so on. This is the essence of what is compounded interest, earning interest on interest.

2.2. Compounding in different financial contexts

Compound interest applies to many areas in personal finance and investing:

- Savings accounts: Banks offer interest that compounds monthly or annually.

- Investment accounts: Dividends or capital gains can be reinvested, leading to compounding returns.

- Forex trading: Profits reinvested over multiple trades may mimic compound growth, especially under strict risk management.

- Loans and credit cards: Unfortunately, compounding can also work against you, as unpaid interest gets added to the balance.

Understanding what a compound interest mechanism is and how it influences various financial products will give you a strategic advantage in managing your money.

See more related articles:

3. The applications of compound interest in real life

Think back to the stories your parents or grandparents tell: “I used to buy a whole bag of groceries for just a few dollars.” Prices don’t stand still: food, rent, and fuel get more expensive every year. That’s inflation. If your money is just sitting in a savings jar or a low-interest account, its value quietly shrinks over time.

This is where compound interest steps in. It works like a silent engine that keeps your wealth growing in the background:

- Beating inflation: As prices rise and the value of money decreases, compounding returns can help your investments outpace inflation, protecting and increasing your wealth over time.

- Saving for big goals: For long-term goals that are 10, 20, or 30 years away, like buying a house or retiring comfortably, compound interest is an incredibly effective tool working in your favor. Even modest monthly contributions can snowball into significant sums as returns generate their own returns year after year.

- Making your retirement last: Compounding doesn’t stop when you stop working. Money left invested after retirement can keep generating returns, stretching your savings further and giving you peace of mind.

- Avoiding financial traps: On the flip side, unpaid credit card balances or loans also compound, showing how powerful (and dangerous) this mechanism can be if you’re not careful.

- Personal financial planning: Compound interest is a key factor when setting up savings strategies, choosing financial instruments, and forecasting future cash flow with online calculators.

In short, what is the meaning of compound interest comes down to “earning interest on interest.” It’s a powerful financial principle that can accelerate your wealth if used wisely, or magnify debt if mismanaged.

Continue reading: How to avoid lifestyle inflation and save more money

4. How do you calculate compound interest?

To effectively harness the power of compound interest, you need to understand the math behind it, specifically, what is the formula of compound interest. While the concept is simple, the compound interest formula, often explained as what is the formula for calculating compound interest, gives you precise control over predicting future value.

Whether you’re saving money or analyzing investment returns, knowing what is the compound interest formula helps you make smarter financial decisions.

4.1. What is compound interest formula?

The following is a simple formula for computing compound interest:

| A = P × (1 + r/n) ^ (nt) |

|---|

Where:

- A = the future value of the investment (including interest)

- P = the principal amount (initial investment)

- r = annual interest rate (in decimal form, so 5% = 0.05)

- n = number of times interest is compounded per year

- t = time in years

This formula, also referred to as what is the formula to calculate compound interest, gives you a way to predict how your investment grows when interest is compounded multiple times per year.

Tip: The Rule of 72 is another way to estimate compound interest. If you divide 72 by your rate of return, you find out how long it will take for your money will double in value. For example, if you have $100 that was earning a 4% return, it would grow to $200 in 18 years (72 / 4 = 18).

4.2. Example calculation

Let’s say you invest $1,000 at a 5% annual interest rate compounded monthly for 3 years.

A = 1000 × (1 + 0.05 / 12) ^ (12 × 3) = 1000 × (1.004167) ^ 36 ≈ $1,161.62

So, after 3 years, your $1,000 becomes approximately $1,161.62 thanks to monthly compounding.

4.3. Understanding each component

Before diving into tools and applications, let’s briefly explain each variable so even beginners can follow:

| Variable | Meaning | Notes |

|---|---|---|

| P | Initial investment | Also called the principal |

| r | Annual interest rate (in decimal) | 5% = 0.05, 8% = 0.08, etc. |

| n | Compounding frequency per year | Monthly = 12, Quarterly = 4, etc. |

| t | Total time in years | Even fractions of a year can be used |

| A | Final amount after compounding | Covers both the original amount and the earned interest |

By mastering what is the formula for compound interest, you’ll be able to model growth over time with confidence, whether for long-term savings, forex portfolio growth, or comparing financial products.

4.4. Compounding interest periods

The compounding interest period refers to the length of time between when interest is calculated and added to the account balance. This period determines how frequently your investment begins to “earn interest on interest.”

Common compounding periods include:

- Annually: Interest is compounded once per year.

- Semiannually: Interest is compounded every 6 months.

- Quarterly: Interest is compounded every 3 months.

- Monthly: Interest is compounded every month.

- Daily: Interest is compounded every day (often used in savings and credit products).

The shorter the compounding period, the more frequently interest is added to your balance, which increases the final return. For example, daily compounding adds interest 365 times per year, allowing your balance to grow faster than annual compounding.

Ultimately, the main thing to remember is that more frequent compounding leads to more growth, assuming all other factors are equal.

4.5. Compounding period frequency

Compounding period frequency refers to how many times in a year interest is compounded. It directly affects how the compound interest formula is applied (in the variable “n” – the number of compounding periods per year).

Here’s a breakdown of common compounding frequencies and their impact:

| Frequency | Times Compounded per Year (n) | Effect on Growth |

|---|---|---|

| Annually | 1 | Slower growth |

| Semiannually | 2 | Slightly faster growth |

| Quarterly | 4 | Moderate compounding |

| Monthly | 12 | Popular in banking |

| Daily | 365 | Maximizes compounding speed |

Example:

If you invest $1,000 at an annual interest rate of 5%, here’s how different frequencies affect your balance after 5 years:

- Annual (1x/year): ~$1,276.28

- Monthly (12x/year): ~$1,284.89

- Daily (365x/year): ~$1,285.00

Even though the difference is small in the short term, it becomes much more significant over decades or with larger amounts.

Pro tip: A good habit when comparing financial products is to look beyond the headline interest rate and always check its compounding frequency.

5. Compound vs. Simple interest: What’s the difference?

If you’re new to personal finance or investing, it’s important to understand what is the difference between simple interest and compounded interest. While both are ways of earning or paying interest, they work very differently, and that difference can significantly impact your long-term financial outcomes.

5.1. Simple interest explained

Simple interest is calculated only on the original principal amount. The formula is:

|

Simple Interest (SI) = P × r × t |

|---|

Where:

- P = initial principal

- r = annual interest rate

- t = time in years

In simple interest, the interest amount stays constant every year because it doesn’t factor in any interest previously earned.

Example: If you invest $1,000 at a 5% simple annual interest for 3 years:

SI = 1000 × 0.05 × 3 = $150

So, your total will be $1,150 after 3 years.

5.2. Compound interest recap

On the other hand, compound interest is calculated on both the principal and the interest that accumulates over time. This creates a “snowball effect” where your earnings grow faster as time progresses, especially with frequent compounding.

In our previous compound interest example ($1,000 at 5% compounded monthly for 3 years), the final amount was $1,161.62 more than the $1,150 you’d earn with simple interest over the same period.

5.3. Key differences between compound and simple interest

Here’s a side-by-side comparison to help you see the distinction clearly:

| Criteria | Simple Interest | Compound Interest |

|---|---|---|

| Calculation | Based only on principle | Based on principal + accumulated interest |

| Interest Amount | Constant over time | Increases over time |

| Returns | Lower, linear growth | Higher, exponential growth |

| Formula | SI = P × r × t | A = P(1 + r/n)<sup>nt</sup> |

| Common Usage | Short-term loans, auto loans | Investments, savings accounts, and forex growth |

5.4. Why this difference matters

Understanding what is compounded interest vs. simple interest is helps you make better decisions, especially when choosing between investment products, loan repayment options, or credit cards. Compound interest rewards patience and early action, while simple interest may be preferable for short-term, low-risk arrangements. This clearly illustrates why compound interest is better than simple interest for long-term wealth building.

6. Why compounding frequency matters for your returns

When it comes to compound interest, most people focus on the rate and time horizon. But there’s another crucial factor that often goes unnoticed: how frequently your interest is compounded. Known as compounding frequency, this detail can significantly influence how much your money earns over time.

What is compounding frequency?

Compounding frequency refers to how often interest is calculated and added to your total balance. The more frequently interest is applied, the faster your capital grows because each cycle builds on a larger base that includes previously earned interest.

Common compounding intervals:

- Annually – Once per year

- Semiannually – Twice a year

- Quarterly – Four times per year

- Monthly – Twelve times a year

- Daily – Every day (365 times a year)

How frequency affects growth:

Let’s compare how a $1,000 investment grows over 5 years at a 5% annual interest rate, under different compounding schedules:

| Compounding frequency | Times per year | Ending value (5 years) |

|---|---|---|

| Annual | 1 | $1,276.28 |

| Semiannual | 2 | $1,282.04 |

| Quarterly | 4 | $1,284.00 |

| Monthly | 12 | $1,284.89 |

| Daily | 365 | $1,285.00 |

What this means for you:

While the differences might appear minimal over a 5-year span, they grow substantially with longer timeframes or larger investments. Even a small difference in frequency can create a noticeable gap in returns when compounded over decades.

So whether you’re choosing a savings account, evaluating a fixed deposit, or analyzing performance data from a prop trading firm, don’t just look at the interest rate; check how often it’s compounded.

7. How compound interest works in everyday life

Understanding compound interest is only the beginning; what truly matters is how it shows up in the real world. Whether you’re saving for a goal or investing for the future, compounding plays a critical role in many financial tools and strategies.

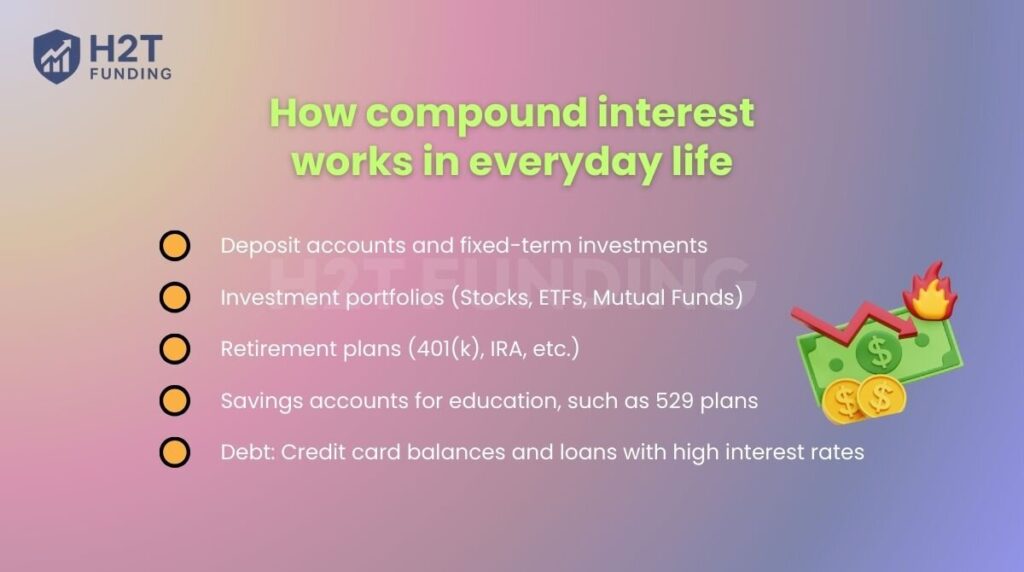

Where you’ll encounter compound interest: Compound interest is more than a theoretical idea. It underpins many of the financial products you use (or may use) every day. Here are some key areas where compounding comes into play:

- Deposit accounts and fixed-term investments: Many banks offer compound interest on savings accounts and Certificates of Deposit (CDs). The frequency of compounding daily, monthly, or quarterly can significantly boost your balance without any extra effort on your part.

- Investment portfolios (Stocks, ETFs, Mutual Funds): When dividends are reinvested and your returns are left untouched, compound growth kicks in. This is a core strategy used by long-term investors to gradually build substantial wealth.

- Retirement plans (401(k), IRA, etc.): Retirement accounts benefit immensely from compound growth over decades. Even modest, consistent contributions can grow into a sizeable retirement fund, thanks to the power of time and compounding.

- Savings accounts for education, such as 529 plans: Just like retirement funds, education savings accounts thrive on early contributions and compounding returns. The earlier you start, the more your savings can grow before you need them.

- Debt: Credit card balances and loans with high interest rates. However, one must also be aware of the disadvantages of compound interest, since it can cause debt to grow quickly if left unmanaged through compounding interest payments. Knowing how compounding works can help you stay ahead of these traps.

Quick comparison: when compound interest helps vs. hurts

| Scenario | Impact of compound interest |

|---|---|

| High-yield savings account | Grows your savings automatically |

| Long-term investment portfolio | Amplifies returns over time |

| Retirement savings | Creates a solid foundation for financial stability |

| Credit card debt | Quickly increases what you owe |

| Payday or predatory loans | Can lead to a debt spiral |

8. The significant benefits of beginning early

One key reason why compound interest is important lies in how strongly it responds to time. Even small, early contributions can grow into much larger outcomes. This is also what the definition of compound interest in practice is: money that accelerates growth the longer it is invested.

The real power of compound interest is unlocked by time. The more time your money has to grow, the more cycles of compounding it can go through, allowing your gains to build on themselves.

Let’s explain this using an example:

| Investor | Contribution Years | Total Amount Invested | Value at Age 65 (7% Annual Return) |

|---|---|---|---|

| Investor A | 20–30 (10 years) | $20,000 | ~$288,000 |

| Investor B | 30–65 (35 years) | $70,000 | ~$280,000 |

Although Investor A invests for only 10 years and puts in far less than Investor B, they end up with more at retirement, all because they started earlier and gave compound interest more time to work.

The example of the two investors brings a few key lessons into focus. It shows that starting early often matters more than the total amount you contribute. Even a delay of a few years can significantly reduce your potential growth, so it’s wise to begin with small, consistent contributions as soon as you can.

In essence, compound interest rewards patience and consistency. The longer your money stays invested, the stronger the effect becomes, turning time to become a major factor in your financial growth. And if you’re wondering when it’s better to save or invest, our guide on saving vs investing pros and cons will help you weigh the options.

9. Resources to assist with compound interest calculations

Knowing how compound interest works is a solid foundation, but turning that knowledge into actionable financial decisions calls for the right tools. Thanks to modern technology, you don’t need to crunch numbers manually; instead, you can rely on a compound interest calculator and spreadsheets to forecast your investment growth with ease.

Why use compound interest calculators:

Trying to compute compound interest by hand can be complex and prone to mistakes, especially when dealing with changing interest rates, different compounding intervals, or long-term investments. Digital calculators take the guesswork out, providing fast and accurate estimates of your potential returns.

Top tools for compound interest calculations:

Here are a few highly regarded tools, both web-based and offline, that simplify the process and help you visualize your future wealth:

1. Web-based compound interest calculators

These tools are simple to use: just enter your initial investment, annual interest rate, compounding frequency, and time period.

- Compound interest calculator from Investopedia: Delivers in-depth projections with helpful visual charts.

- Compound interest calculator offered by Bankrate: Ideal for comparing multiple investment scenarios.

- Compound interest calculator provided by the SEC: A straightforward, reliable tool backed by a reputable institution.

2. Excel or Google Sheets

If you prefer spreadsheets, the FV (Future Value) function in Excel or Google Sheets lets you model growth scenarios. This option gives you the flexibility to customize assumptions and compare outcomes.

3. Budgeting and financial planning apps

In addition to calculators, budgeting apps such as YNAB or PocketGuard can help you apply compounding in real life. They allow you to track savings goals, simulate investment growth, and adjust monthly contributions so you stay consistent. This way, you’re not just crunching numbers; you’re actively managing your financial plan.

Pro Tips:

- Always match the compounding frequency in your inputs (e.g., monthly, yearly).

- Test multiple scenarios to understand how changes in rate or duration affect your returns.

- Bookmark trusted tools for regular planning and adjustments.

Whether you’re calculating returns on savings or evaluating a long-term investment, these tools simplify the complex math behind compounding of interest.

Read more:

10. FAQ

Compound interest is the process of earning interest on both the original amount (principal) and the interest that has already been added. Over time, this leads to faster growth of your money compared to simple interest, which only applies to the original amount.

You can check if interest is compounded by reviewing the terms of the financial product. Look for mentions of “compounding frequency” (e.g., daily, monthly, annually). If the interest is added to the balance periodically and then future interest is calculated on the new total, it’s compound interest.

A 12% compounded interest rate means your money earns 12% per year, with the interest being calculated and added back at regular intervals (e.g., monthly or annually). For example, with annual compounding, your investment grows by 12% once per year. With monthly compounding, the 12% rate is divided into 12 monthly periods, and the effect of compounding makes the total return slightly higher than 12% annually.

Compound interest can be both good and bad, depending on the context. It’s beneficial when you’re earning it, like in savings accounts or investments, because your wealth grows faster over time. However, it can be harmful when you’re paying it like on credit cards or high-interest loans because debt can grow quickly if unpaid.

Compound interest simply means you earn interest not only on the money you originally put in, but also on the interest that gets added along the way. In other words, it’s “interest on interest,” which makes your money grow faster over time compared to simple interest.

If you earn 5% simple interest on $5,000 for one year, you’ll make $250 (because 5% of 5,000 = 250). With compound interest, the calculation depends on how often the interest is added. For example, if it’s compounded annually, after one year you’d still have $5,250, but in the second year, the 5% applies to $5,250, so you’d earn $262.50 instead of just $250.

At the end of the first year, you will have $1,060. By the end of the second year, you earn interest not just on the original $1,000 but also on the $60 from the first year, giving you a total of about $1,123.60.

11. Conclusion

Understanding what is compound interest is more than just knowing a formula; it’s about unlocking a powerful concept that can accelerate your financial growth over time. Whether you’re saving for the future, investing, or managing profits from trading, it’s one of the most effective concepts to have on your side.

At H2T Funding, we believe that financial success starts with financial knowledge. That’s why we create in-depth, beginner-friendly resources, like this one on the Cash Flow & Saving Strategies section, to help you take control of your money with confidence and clarity.