Ever feel like your trading profits vanish as quickly as they appear? You’re not alone. When you’re managing market risks, saving can feel like an afterthought.

But what if you could lock in your gains and build real wealth systematically? There’s a simple but powerful strategy for that: pay yourself first.

Instead of saving what’s left after spending, you flip the script by setting money aside before you even start spending. It’s a mindset shift that helps you build long-term wealth, gain financial discipline, and stay prepared for volatile trading conditions.

In this guide, H2T Funding will break down what is the pay yourself first method, how it works, and how to apply it to your trading or investing journey. You’ll also learn how it compares to other budgeting styles, the best tools to get started, and common mistakes to avoid.

Key takeaways

- The pay yourself first method is a budgeting approach where savings come before any other expenses, helping traders secure long-term stability.

- This method builds discipline by setting aside a fixed percentage of profits first, often 10–20%, before covering trading costs or lifestyle needs.

- Automating transfers ensures consistency, reduces emotional spending, and makes saving a habit rather than a choice.

- Reviewing results regularly allows traders to adjust saving rates, build stronger buffers, and align financial growth with trading goals.

1. What is the pay yourself first method?

A clear pay yourself first definition is that it’s a proactive budgeting approach where you allocate a fixed portion of your income to savings or investments before spending on anything else. Instead of treating savings as an afterthought, you make it your top financial priority.

The idea is rooted in financial self-respect: you work hard for your money, so you should reward your future self before catering to current wants. Whether you’re building an emergency fund, saving for retirement, or funding your trading capital, the concept stays the same: save first, spend later.

In contrast to traditional budgeting, where income is divided among bills, necessities, and finally savings, the pay yourself first budget method ensures your goals don’t get left behind. Compared to creating a personal budget, this method puts savings at the very top of the priority list. It works especially well for:

- Traders looking to set aside consistent capital

- Investors who prioritize steady growth over time

- Anyone aiming to improve money habits and reduce financial stress

By automating savings at the beginning of each pay cycle, the pay yourself first budgeting method turns wealth-building into a habit, not a chore.

2. How to pay yourself first approach to budgeting functions

To truly understand what does pay yourself first strategies do, you need to see how they function in a real-world setting. While the concept sounds simple, save first, spend later, the effectiveness of this method lies in how it’s structured and implemented over time.

Theory is great, but let’s get practical. Here’s how it works day-to-day:

- Determine your savings goals: Start by defining clear, actionable goals such as building a $5,000 emergency fund, contributing to your trading capital, or investing in a long-term ETF portfolio.

- Set a fixed saving percentage: Most financial experts recommend allocating at least 10–20% of your income toward savings. However, if you’re a trader or investor, this amount may vary depending on how much risk capital you need.

- Automate your savings: Set up automatic transfers to designated savings or investment accounts as soon as you receive your income. This ensures savings happen before any spending takes place.

- Cover your essential expenses next: After saving, use the remaining income to cover rent, utilities, food, and other needs. If you find the leftover amount insufficient, it may be time to track your expenses and identify areas to cut back rather than reducing savings.

- Use the remainder for wants or trading activity: Anything left over can be used for non-essential spending or additional trades. The key is that saving remains non-negotiable.

This clear prioritization reflects the core pay yourself first principle: direct your take-home income to savings before covering expenses, so your financial future always comes first.

Here’s a simple pay yourself first example to illustrate how this method works for a trader’s monthly income.

| Monthly Income | Allocation | Amount (USD) |

|---|---|---|

| $3,000 | Save first (20%) | $600 |

| Rent, utilities, food (60%) | $1,800 | |

| Trading fund or wants (20%) | $600 |

Let’s be crystal clear on this: The entire method applies only to your trading profits. Never withdraw from your core capital to “pay yourself first.” Your trading capital is your tool; don’t break it. If you have a losing month, you simply don’t save from trading that month. It’s the most important pay yourself first rule for traders.”

Why does pay yourself first rule work so well?

Unlike other budgeting methods that often leave savings to chance, the pay-yourself-first method builds discipline into your financial system. Automating the process reduces emotional spending and helps reinforce your long-term trading or investing goals.

When integrated with trading platforms or fintech tools that support automation, this method becomes even more effective, especially for Forex traders managing volatile capital.

See more related articles:

3. Benefits of the pay yourself first method for traders and investors

There are several pay yourself first budgeting advantages that make this method particularly appealing for traders and long-term investors. By prioritizing saving and capital preservation before spending, this method empowers you to build a stable financial base, regardless of market volatility.

3.1. Builds an emergency fund fast

Having an emergency fund is essential for every trader and investor. Markets are unpredictable drawdowns, margin calls, or unexpected personal expenses can arise at any time.

By saving first, you automatically contribute to your safety net, allowing you to:

- Avoid liquidating trades prematurely

- Protect yourself from forced borrowing

- Stay emotionally stable during market downturns

For traders, it’s wise to have two types of funds. First, a personal emergency fund for life’s surprises. Second, consider a trading buffer fund. This is money set aside to handle a series of losses (a drawdown) without forcing you to stop trading.

3.2. Aligns with long-term goals

One of the biggest mistakes among new traders is focusing solely on short-term gains. The pay yourself first budgeting method forces you to think in terms of long-term outcomes by:

- Promoting regular deposits into investment portfolios

- Supporting goal-based trading plans (e.g., saving for a $10,000 trading fund)

- Reducing the temptation to overtrade or risk too much capital

That kind of alignment fosters sustainable wealth-building, not just aggressive speculation.

3.3. Improves discipline

Consistency is key in both trading and personal finance. Saving before spending builds the habit of financial discipline, which naturally translates into:

- Improved control over risk in your trading decisions

- Thoughtful allocation of trading capital

- Enhanced ability to make sound choices in high-stress situations

As this discipline becomes second nature, it enhances your performance across both financial and personal domains.

3.4. Compatible with automation tools and systems

Modern traders rely heavily on automation, whether through trading bots, alerts, or portfolio rebalancing tools. The pay-yourself-first method fits seamlessly into this ecosystem.

When you set your savings contributions on autopilot:

- You eliminate emotional decision-making

- You ensure consistency, even with fluctuating income

- You can easily integrate savings into your broader financial tech stack

For traders who use platforms like TradingView, MetaTrader, or budgeting tools like YNAB or Mint, automating this method is a straightforward way to scale up efficiency.

View more:

4. Comparing pay yourself first with other budgeting methods

While the pay yourself first method has gained popularity among financially savvy individuals, it’s important to understand how it differs from traditional budgeting styles. This comparison will help you evaluate whether it aligns better with your lifestyle, goals, and trading habits.

| Budgeting Method | Core Focus | Saving Priority | Ease of Use for Traders | Flexibility |

|---|---|---|---|---|

| Pay Yourself First | Saving before spending | Top priority | High (when automated) | Moderate |

| 50/30/20 Rule | Maintaining harmony among essentials, desires, and financial goals | 20% of income allocated | Moderate | High |

| Zero-Based Budgeting | Giving each dollar a defined role in your budget | Varies by plan | Low (manual adjustments) | Low to moderate |

| Envelope Method | Distributing physical cash into designated spending categories | Low priority | Low | Low (not ideal for digital transactions) |

Main insights:

- The pay yourself first budget method puts saving at the top, making it ideal for traders who want to build a strong foundation of risk capital.

- It works especially well when combined with automated transfers and long-term financial goals, which many traditional methods overlook.

- While other methods like the 50/30/20 rule offer flexibility and simplicity, they often treat saving as optional rather than essential.

In short, if you’re a trader or investor looking to stay financially prepared while still pursuing growth, the pay-yourself-first strategy provides the structure and security you need. Some traders also experiment with a reverse budgeting template, where savings are set first and all other expenses are adjusted afterward.

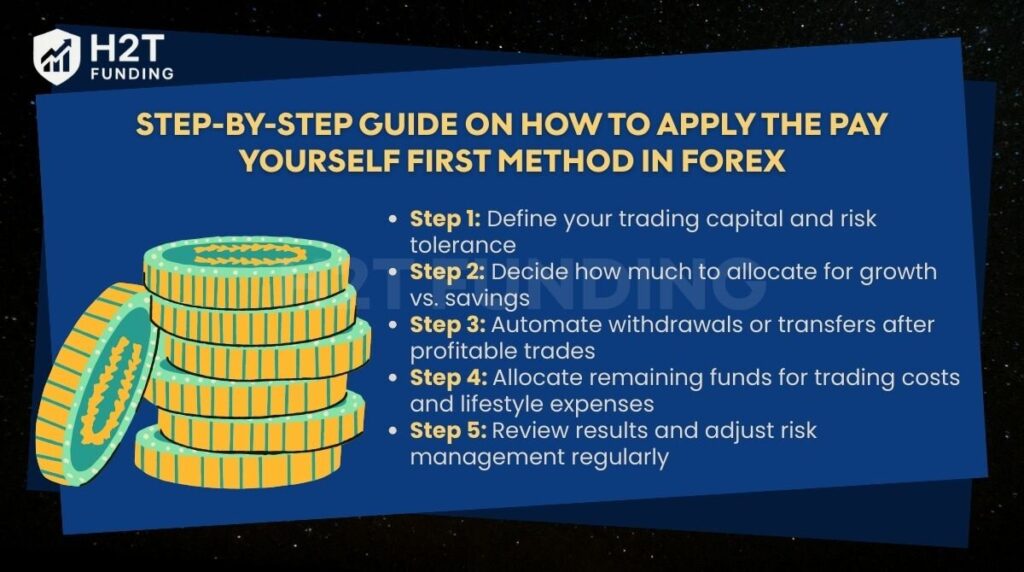

5. Step-by-step guide on how to apply the pay yourself first method in Forex

Now, let’s apply this concept directly to the trading floor. For traders, paying yourself first is about creating a system to protect and grow your profits sustainably. Here’s how you can structure it:

- Step 1: Define your trading capital and risk tolerance

- Step 2: Decide how much to allocate for growth vs. savings

- Step 3: Automate withdrawals or transfers after profitable trades

- Step 4: Allocate remaining funds for trading costs and lifestyle expenses

- Step 5: Review results and adjust risk management regularly

Go take a closer look at how each step works in practice.

5.1. Step 1: Define your trading capital and risk tolerance

Before entering the market, calculate how much capital you’re willing to risk. That includes money you can afford to lose without affecting essential living expenses. Traders often limit risk per trade to 1–2% of account balance to preserve longevity.

5.2. Step 2: Decide how much to allocate for growth vs. savings

Here, you face the classic trader’s dilemma. Do you withdraw profits to secure them, or let them ride to grow your account faster? The pay yourself first method helps you do both. A common approach is a 20/80 split: withdraw 20% of profits to your savings, and reinvest the remaining 80% to compound your trading capital.

Take a case where the monthly profit reaches $500:

- $100 (20%) is moved to a savings account.

- $400 is left in the trading account to support larger position sizes and compounding growth.

5.3. Step 3: Automate withdrawals or transfers after profitable trades

Don’t wait until emotions take over. Schedule automatic transfers of profits to a savings or investment account; this locks in gains and prevents overtrading. Many brokers allow recurring withdrawals, which makes the process seamless.

5.4. Step 4: Allocate remaining funds for trading costs and lifestyle expenses

What’s left after saving should cover trading fees (commissions, swaps, VPS, data tools) and personal spending. Keeping expenses in check ensures you don’t dip back into savings.

Imagine a trader earning $800 a month:

- $160 (20%) saved immediately.

- $100 covers trading tools like VPS or charting software.

- The remaining $540 is available for reinvestment or personal use.

5.5. Step 5: Review results and adjust risk management regularly

At least every quarter, analyze your results. Are you hitting growth targets? If profits exceed expectations, increase the “pay yourself” percentage. If not, reassess your strategy and risk parameters.

In summary, paying yourself first in Forex means saving a fixed part of profits before anything else. Use the rest for trading costs and daily needs. This habit locks in gains and supports steady growth.

6. Best accounts to combine with the pay-yourself-first method

To make the pay-yourself-first method truly effective, where you park your money matters just as much as how much you save. Choosing the right types of accounts can amplify your returns, protect your capital, and keep your financial goals on track.

Here are the best account types to consider when applying this budgeting strategy:

| Account Type | Purpose | Best For |

|---|---|---|

| High-yield savings account | Generates higher returns compared to regular savings accounts | Funds for emergencies and short-term financial objectives |

| Traditional savings account | Safe and accessible place for savings with low risk | Everyday savings and short-term goals |

| Money market account | Provides higher interest with limited check-writing privileges | Balancing liquidity and better returns |

| Certificate of Deposit (CD) | Locks in funds for a fixed term at a higher interest rate | Medium-term goals that don’t need liquidity |

| 401(k) or Individual Retirement Account (IRA) | Tax-deferred growth for retirement savings | Long-term investing and retirement planning |

| Education savings account | Tax-advantaged savings for future education expenses | Parents or students preparing for tuition costs |

| Health savings account (HSA) | Triple tax advantage: contributions, growth, withdrawals | Covering qualified medical expenses |

| Flexible spending account (FSA) | Pre-tax savings for healthcare or dependent care | Short-term medical or dependent care costs |

| Tax-advantaged accounts (general) | Offers tax deferral or deductions (e.g., IRA, 401(k)) | Investing for the long haul and preparing for retirement |

| Brokerage account | For investing in ETFs, stocks, or diversified funds | Growing wealth with moderate risk over time |

| Forex reserve account | A non-trading account for building future trading capital | Increasing prop trading size or funding challenges |

Tip: If you’re trading internationally or managing multiple currencies, consider using multi-currency accounts (like Wise or Revolut) to reduce exchange rate losses when saving across borders.

Combining these accounts strategically, you build a financial “ecosystem” where each dollar saved supports your Forex goals, whether that’s surviving a market dip or scaling your trading portfolio.

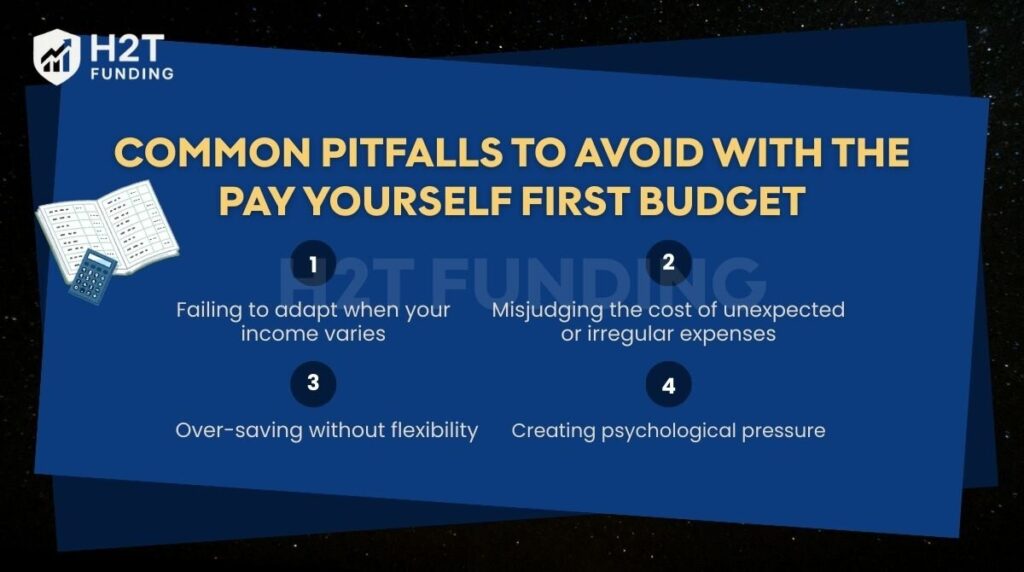

7. Common pitfalls to avoid with the pay yourself first budget

Like any method, there are pay yourself first budget pros and cons that traders should weigh before fully committing. Some traders highlight pay yourself first budget disadvantages, such as a lack of flexibility when income drops or when unexpected costs arise. Here’s what to watch out for:

7.1. Failing to adapt when your income varies

It’s easy to stick to a fixed savings amount, but life and income change. Whether you earn more from trading wins or less due to drawdowns, your savings percentage should reflect those fluctuations.

Tip: Set your savings as a percentage of your net profits, not a fixed dollar amount. In months with no profit, you save nothing from your trading. Your goal then is to protect your capital.

7.2. Misjudging the cost of unexpected or irregular expenses

Ignoring annual costs like trading software subscriptions, taxes, or surprise margin calls can force you to dip into your savings. This defeats the purpose of paying yourself first.

Solution: Add a buffer for “known unknowns” in your monthly budget and build a sinking fund for irregular expenses.

7.3. Over-saving without flexibility

Yes, saving aggressively is good, but not if it leads to stress, debt, or skipping opportunities (like a great course or a low-drawdown prop firm challenge). Balance is key.

Reminder: Pay yourself, but don’t punish yourself. Saving should support your financial journey, not suffocate it.

7.4. Creating psychological pressure

Feeling forced to hit a profit target just to meet a savings goal is dangerous. This pressure can lead to over-trading or taking bad risks.

Remember: Trade your strategy first. If it results in a profit, then apply the pay yourself first rule.

8. Resources and tools to help you begin

Getting started with the pay yourself first budgeting method doesn’t require complicated tools, just consistency and the right resources. Here’s what traders and investors can use to make the most of this strategy:

8.1. Budgeting apps that include automated features

To succeed with this method, automation is your best friend. These budgeting apps and finance tools let you set up recurring transfers, track progress, and adjust quickly:

- YNAB (You Need A Budget): Offers goal-focused budgeting with a strong emphasis on a saving-first mentality.

- PocketGuard: Helps you see what’s “safe to spend” after saving and fixed costs.

- GoodBudget: A simple envelope system app that works well for those who prefer category-based saving.

- Revolut / N26 / Monzo: Modern fintech banks with “savings vaults” and instant transfers.

8.2. Bank accounts and broker platforms

For Forex traders, keeping funds segmented is essential. Use:

- High-yield savings accounts: For emergency or goal-based saving.

- Brokerage accounts with no minimums: Allocate funds for long-term investment goals.

- Multi-currency wallets: Useful for traders managing different currency pairs or prop firm payouts.

8.3. Financial planning tools

A few powerful platforms for planning:

- TradingView: Not just for charts. You can visualize long-term financial goals with custom indicators.

- Excel or Google Sheets templates: For traders who prefer manual control with custom categories.

- Compound interest calculators: Help project how fast your savings grow over time when applied consistently.

For deeper insights, you can also explore the Pay Yourself First book that explains this budgeting method in detail.

Pro tip: Set a calendar reminder to review your savings and trading withdrawals every month. Adjust contributions as your income grows or market conditions shift.

9. FAQs

The pay yourself first method is a budgeting strategy where you allocate a fixed portion of your take-home income to savings or investments before covering any expenses. This approach builds a strong savings habit and ensures your financial goals are prioritized.

The 50/30/20 rule divides your income into three categories: 50% for needs (rent, bills, food), 30% for wants (entertainment, lifestyle), and 20% for savings or debt repayment. It’s a simple framework to balance spending and saving.

The pay yourself first concept formula is straightforward: Income – Savings = Expenses. Instead of saving what’s left after spending, you set aside savings first, then live within the remaining spending limits.

The 70-10-10-10 rule suggests splitting your income into 70% for living expenses, 10% for savings, 10% for investments, and 10% for charitable giving. It encourages disciplined money management while balancing personal use, growth, and contribution.

Two advantages of the pay yourself first method are the ability to establish a strong savings habit and the reduction of financial stress. By prioritizing savings before expenses, you secure your future goals while maintaining better control over discretionary spending.

10. Final thoughts: Make saving a habit, not a struggle

Mastering the pay yourself first method is about more than just budgeting – it’s about building a sustainable habit that supports your financial freedom and trading goals. By prioritizing your savings before any other expenses, you create a safety net that empowers you to take smarter risks and stay disciplined over the long term.

Remember, consistency is key. Even small, regular contributions grow into significant savings over time thanks to the power of compounding. Automating your savings helps remove the temptation to spend what you should be saving and keeps your financial plan on track without stress.

For traders and investors, this approach aligns perfectly with the mindset needed to succeed in volatile markets – patience, discipline, and preparation. Start today by paying yourself first, and watch how this simple change can transform your financial journey.

To deepen your understanding and implement effective budgeting strategies, explore more expert insights and tools on Budgeting Strategies of H2T Funding. Make saving a habit, not a struggle, and take control of your financial future.