In today’s fast-changing economy, knowing how to set financial goals and achieve them is more than just a useful skill; it’s a foundational step toward financial stability, independence, and long-term success.

Yet, for beginners, the process can feel overwhelming: Where do you start? What goals make sense for your lifestyle? How do you track progress?

In this guide, H2T Funding will walk you through the basics of setting personal, couple, and business financial goals, share real-world examples, and provide tools you can use immediately.

By the end of this article, you’ll not only understand how to set financial goals that align with your values, but you’ll also be equipped to achieve them with clarity and confidence.

Key takeaways

- Financial goals mean giving your money structure and purpose, helping you stay focused on what matters.

- Use the SMART framework, budgeting tools, and milestones to turn big aspirations into actionable steps.

- Balancing short-term needs with mid-term goals and long-term planning builds lasting financial security and overall financial health.

1. What are financial goals?

Financial goals are specific objectives you set for how you want to manage, save, spend, or invest your money over a defined period.

These goals can be short-term (e.g., building an emergency fund), medium-term (e.g., saving for a car), or long-term (e.g., preparing for retirement or achieving financial independence)

Key takeaway: Financial goals give your money a purpose. Without them, it’s easy to lose focus, overspend, or make decisions that delay your progress.

2. Why setting financial goals matters

Understanding how to set financial goals is only valuable if you realise why it matters. Financial goals aren’t just abstract numbers or wishful thinking; they’re tools that give direction to your decisions, habits, and priorities. For beginners and seasoned planners alike, setting goals creates a measurable path to financial success.

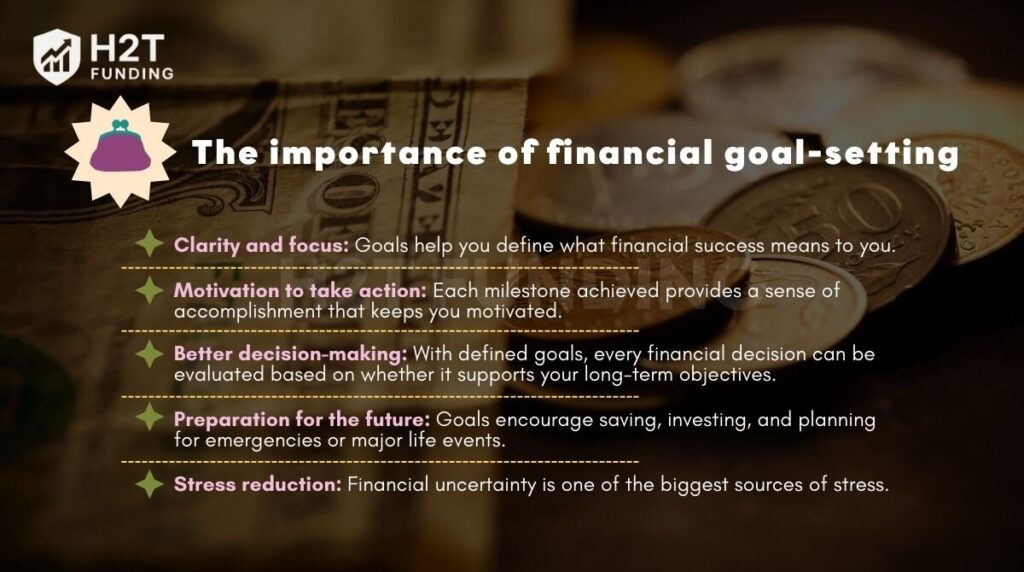

2.1. The importance of financial goal-setting

Here’s why setting financial goals is crucial:

- Clarity and focus: Goals help you define what financial success means to you. Without clear objectives, it’s easy to drift into poor spending habits or delay important financial actions.

- Motivation to take action: When you break down goals into smaller steps, each milestone achieved provides a sense of accomplishment that keeps you motivated.

- Better decision-making: With defined goals, every financial decision, whether it’s a small purchase or a major investment, can be evaluated based on whether it supports your long-term objectives.

- Preparation for the future: Goals encourage saving, investing, and planning for emergencies or major life events like buying a home or starting a business.

- Stress reduction: Financial uncertainty is one of the biggest sources of stress. A clear roadmap reduces anxiety by giving you a sense of control over your future.

2.2. Financial goals in the context of forex and trading

Even for forex traders or investors, setting financial goals is essential. Creating a clear trading plan helps you define and reach those goals. For example, you might aim to:

- Reach a monthly profit target from trading.

- Save a portion of trading profits for long-term investments.

- Build capital to qualify for a prop firm account.

These are financial goals, too; they just exist in a more dynamic, high-risk environment, and they require even more discipline to achieve.

Key takeaway: Whether you’re saving for a rainy day or building wealth through forex, goal-setting brings structure and purpose to your financial journey.

3. 3 types of financial goals

When people talk about financial goals, they usually fall into three main categories:

- Short-term goals (within 1 year)

- Medium-term goals (1–5 years)

- Long-term goals (5+ years)

Each type plays a different role in shaping your financial journey. By knowing the difference, you can plan smarter and move step by step toward lasting stability and growth.

3.1. Short-term goals

Short-term financial goals are the quick wins. They are usually achieved within a year and focus on stability and daily money management. Examples include:

- Creating a monthly budget

- Building a small emergency fund

- Paying off a credit card balance

- Automating savings transfers

Working on short-term goals helps you stay in control of your finances and reduces stress when unexpected expenses come up.

3.2. Mid-term goals

Mid-term goals take more time and planning, often between three to five years. They usually involve bigger commitments and require you to stay disciplined. Examples include:

- Saving for a car or a home down payment

- Paying off student loans

- Setting aside money for professional training

- Building a larger investment fund

Mid-term goals connect the gap between everyday stability and future wealth creation. They keep you moving forward while preparing for bigger milestones.

3.3. Long-term goals

Long-term goals stretch beyond five years and focus on financial independence. They often require patience, consistency, and a vision for the future. Long-term financial goals examples include:

- Planning for retirement

- Paying off a mortgage

- Building generational wealth

- Creating an estate plan

Starting early is key. Time allows your money to grow, and even small steps now can reduce financial pressure later in life.

4. How to set financial goals (the foundation)

Ready to build a plan you can actually stick to? It starts with a strong foundation. Follow these five steps to turn your financial aspirations into reality.

- Assess your current financial situation

- Define your priorities

- Choose SMART goals

- Break down big goals into milestones

- Write them down and visualise progress

Each step builds on the last, helping you create a financial plan you can actually stick to. Keep reading as we go through these steps one by one and show you how to put them into action.

4.1. Assess your current financial situation

Before you set goals, you need to know where you stand. Think of it as your financial “starting point.” Without understanding your income, expenses, savings, and debts, any goal you set will be based on guesswork.

What to review:

- Income: Total monthly income (salary, side hustles, investments).

- Expenses: Fixed and variable costs (rent, bills, groceries, subscriptions).

- Debts: Credit card balances, loans, outstanding payments.

- Savings & Investments: Emergency funds, retirement accounts, trading capital, etc.

Tip: Learn how to track expenses carefully to see where your money goes. You can also try budgeting apps like YNAB or Excel templates to get a complete snapshot.

4.2. Define your priorities

Once you understand your financial landscape, identify what truly matters. Financial goals should reflect your life goals, so think deeply about what you want to accomplish.

Common financial priorities:

- Building an emergency fund

- Paying off high-interest debt

- Saving for a home or vehicle

- Planning for retirement

- Growing a trading account

- Supporting family or starting a business

To stay on track, avoid common budgeting mistakes that can slow down your progress.

4.3. Choose SMART goals

Generic goals like “save more money” or “get rich” are vague and ineffective. Here are SMART financial goals examples:

| SMART Criteria | Example: Vague Goal | Example: SMART Goal |

|---|---|---|

| Specific | Save money | Save $5,000 for an emergency fund |

| Measurable | Invest regularly | Invest $200/month in ETF” |

| Achievable | Make $100k in 2 months | Grow trading capital by 10% in 6 months |

| Relevant | Buy random stocks | Invest based on a long-term retirement plan |

| Time-bound | Eventually retire | Reach $100,000 retirement fund by age 45 |

SMART goals turn your ambitions into something you can act on and track. Now, take a moment to reflect: What are your short-term financial goals, and how can you start working toward them today?

4.4. Break down big goals into milestones

Big financial goals can feel overwhelming. That’s why breaking them into smaller, achievable milestones is key. Milestones keep you motivated and make the goal-setting process less intimidating.

For example:

- Goal: Save $12,000 in one year -> Milestones: $1,000/month or $250/week

- Goal: Pay off $6,000 debt in 6 months -> Milestones: $1,000/month or $250/week

4.5. Write them down & visualise

A goal that only exists in your head is just a dream. The simple act of writing it down makes it real and holds you accountable. Go a step further and visualise your success, a picture of your dream home on the fridge, a savings tracker you colour in. These visual cues keep your motivation high.

Try this:

- Keep a financial journal or spreadsheet to track progress.

- Create a vision board or dashboard showing your goals (vacation, home, debt-free chart, etc.).

- Use habit trackers or financial planning apps.

See more related articles:

5. Examples: how to set financial goals in different scenarios

Setting financial goals can look very different depending on your personal circumstances. Whether you’re managing your own finances, sharing goals with your partner, or running a business, tailoring your approach is essential. Let’s explore practical financial goals, examples of how to set financial goals for various situations.

5.1. Personal financial goals

For individuals, financial goals often revolve around stability, growth, and future planning. These goals can be short-term, like saving for a vacation, or long-term, like building retirement savings.

Here’s an example of financial goals individuals often set to improve their stability and growth:

- Build an emergency fund covering 3–6 months of expenses

- Save $5,000 within 12 months for a down payment on a home

- Pay off credit card debt within 6 months

- Invest regularly in retirement accounts or ETFs

- Track and reduce monthly discretionary spending by 10%

Setting clear, realistic targets and deadlines helps you stay on track and adjust as needed.

5.2. Financial goals for couples

When two people share finances, aligning your financial goals is crucial for harmony and progress. Couples should communicate openly about their money priorities, responsibilities, and timelines.

Key steps for couples:

- Discuss and agree on joint financial priorities (e.g., buying a home, saving for children’s education)

- Set shared budgets and savings targets

- Plan for short-term goals (vacations, debt payoff) and long-term goals (retirement, investments)

- Review and adjust goals regularly together

5.3. Financial goals for a business

Businesses require a structured approach to financial goal setting, focusing on growth, profitability, and sustainability. Clear financial goals help you allocate resources wisely and measure success.

Examples of business financial goals:

- Increase monthly revenue by 15% within 6 months

- Reduce operating costs by 10% in the next quarter

- Build a cash reserve equal to 3 months of operating expenses

- Expand investment in marketing by 20% to drive sales

- Set profit margin targets for each product line

Setting measurable business goals ensures you can evaluate performance and pivot strategies when necessary.

6. Tools & templates to set up financial goals

Having the right tools and templates can make the process of setting and tracking financial goals much easier and more effective. Whether you prefer digital solutions or printable resources, using structured formats helps maintain clarity and motivation.

Why use tools and templates? Using financial planning tools offers several advantages:

- Keeps your goals organised and visible

- Helps track progress and deadlines

- Provides reminders and actionable steps

- Simplifies budgeting and forecasting

- Encourages consistency and accountability

Here are some recommended tools to help you set and manage your financial goals:

| Tool name | Type | Key features | Suitable for |

|---|---|---|---|

| YNAB (You Need a Budget) | Paid app & web | Detailed budgeting, goal tracking | Personal & Couples |

| Honeydue | Free app | Shared budgets, bill reminders | Couples |

| Excel or Google Sheets | Template-based | Customizable goal trackers & budgets | Personal, Couples, Business |

| QuickBooks | Paid software | Business accounting, invoicing, and reporting | Small to medium businesses |

If you prefer a more hands-on approach, here are some common templates you can start with:

- Financial goal-setting worksheet: Define your goals, timeline, and steps to achieve them

- Monthly budget planner: Track income, expenses, and savings goals

- Debt payoff calculator: Plan and monitor debt reduction progress

- Investment tracker: Record and evaluate your portfolio performance

Pro Tip: Combining digital tools with printable worksheets can enhance your goal-setting routine by providing flexibility and structure.

Using these tools regularly and updating your progress will keep your financial goals realistic and achievable.

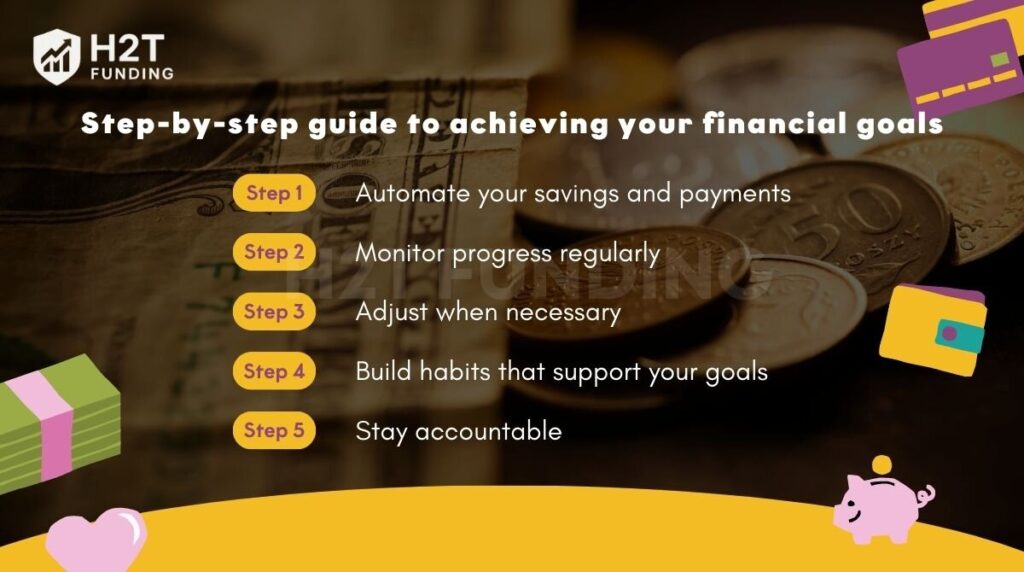

7. Step-by-step guide to achieving your financial goals

A great plan is useless without action. Here’s how to stay on track and see your goals through to the finish line.

7.1. Automate your savings and payments

Automation is one of the most effective ways to stay on track.

- Set up automatic transfers to savings or investment accounts

- Automate bill payments to avoid late fees

- Use goal-based savings features offered by many fintech apps

7.2. Monitor progress regularly

Tracking your progress helps you stay accountable and adapt to changes.

- Set monthly or quarterly check-ins

- Use spreadsheets or apps to log achievements and setbacks

- Celebrate small wins to stay motivated

7.3. Adjust when necessary

Life circumstances change, and your financial goals should adapt to them.

- Reassess goals after major life events (job change, marriage, children)

- Refine timelines or amounts based on new income or priorities

7.4. Build habits that support your goals

Your daily behaviour has a direct impact on long-term success.

- Practice mindful spending

- Track and reduce unnecessary expenses

- Educate yourself on personal finance principles

7.5. Stay accountable

Having support can increase your chances of success.

- Share your goals with a trusted partner or friend

- Join online communities or financial coaching groups

- Use accountability tools or reminders

Example: Applying this framework

| Goal | Step Taken | Outcome |

|---|---|---|

| Save $10,000 in 12 months for a car down payment. | Automated a weekly transfer of $200. Cut back on two streaming services. | Reached goal in 13 months after an unexpected vet bill paused savings for a month. |

| Pay off $5,000 credit card debt in 6 months. | Used the snowball method, putting any extra income toward the balance. | Paid off in 7 months. Slower than planned, but still a huge win! |

Consistency beats intensity. Even small steps taken regularly lead to real progress over time. By following this system, you create a strong foundation that connects planning with action, a critical link many people overlook.

View more:

8. Common mistakes to avoid

Even with the best intentions, many people struggle to reach their financial goals because of avoidable missteps. Understanding these common mistakes can help you stay on the right path and make smarter financial decisions from the start.

Before diving deeper into your planning, make sure to avoid these pitfalls:

8.1. Setting vague or unrealistic goals

Without clarity, your goals become difficult to achieve.

- Example: “I want to be rich.”

- Better: “I want to save $20,000 in 2 years for a house down payment.”

Use the SMART framework to ensure goals are Specific, Measurable, Achievable, Relevant, and Time-bound.

8.2. Ignoring your current financial reality

You can’t plan effectively without a realistic understanding of where you stand.

- Avoid setting goals without reviewing your income, expenses, or debt

- Unrealistic expectations lead to frustration and early burnout

Tip: If budgeting feels overwhelming, try these methods to stop spending when budgeting doesn’t work.

8.3. Not tracking or reviewing progress

Failing to measure progress can result in drifting off course.

- Regular check-ins help identify what’s working and what needs adjusting

- Use financial apps or spreadsheets to monitor performance

8.4. Lacking an emergency fund

Unexpected expenses can derail your plans.

- Always build a small emergency fund before working on long-term goals

- Aim for at least 3–6 months’ worth of essential expenses

- Use a simple emergency fund calculator to figure out how much you really need

8.5. Following trends or others’ goals

Your financial journey should be personal, not a copy of someone else’s.

- Don’t save or invest based on social media hype or peer pressure

- Focus on goals that align with your own values and life plans

8.6. Being inconsistent

Even the best goal is meaningless without consistent action.

- Progress requires discipline, not perfection

- Avoid “all-or-nothing” thinking; small steps are still steps

Staying aware of these mistakes helps you practice better debt management and smart prioritisation. By aligning your actions with mid-term goals and long-term aspirations, you strengthen both financial security and financial health. This foundation paves the way for lasting wealth creation.

9. Final tips for beginners

Starting your financial goal-setting journey can feel overwhelming, but it doesn’t have to be. By following a few practical principles, even beginners can build strong habits and make meaningful progress toward a more secure future.

Let’s explore some actionable tips to help you stay focused and motivated:

9.1. Start small, then build momentum

You don’t need to overhaul your entire life overnight.

- Begin with one or two simple, achievable goals

- Example: Save an extra $50 per month or reduce one recurring expense

Small wins boost confidence and create momentum for bigger goals.

9.2. Schedule monthly financial check-ins

Regular reviews help you catch issues early and adjust your plan.

- Pick a recurring date (e.g., first Sunday of each month)

- Review spending, progress, and any changes in priorities

9.3. Automate where possible

Remove friction from your goals by automating savings and payments.

- Use automatic transfers to savings or investment accounts

- Set bill reminders to avoid late fees

9.4. Use visual motivation tools

Seeing your progress makes it easier to stay committed.

- Try goal-tracking apps, printable savings charts, or whiteboards

- Visual reminders keep your “why” top of mind

9.6. Don’t be afraid to adjust

Life changes, and your financial goals should adapt too.

- Reevaluate your goals every 6–12 months

- Celebrate completed goals and replace them with new ones

9.7. Keep learning

Financial literacy is a long-term journey.

- Follow reputable sources like Investopedia, Babypips, or H2T Funding

- Learn about budgeting, saving, investing, and risk management

10. FAQs about how to set financial goals

The best way to set financial goals is to use the SMART method – Specific, Measurable, Achievable, Relevant, and Time-bound. Start by assessing your financial situation, identifying your priorities, and breaking big goals into smaller, trackable milestones.

To set and achieve financial goals, consistency is key. Write your goals down, create an action plan, review your progress regularly, and adjust when necessary. Tools like budgeting apps and goal-tracking templates can help keep you on track.

If you’re new to goal-setting, begin with simple personal financial goals such as building an emergency fund or paying off debt. Focus on short-term, achievable wins first, and gradually move toward long-term goals like retirement or investment planning.

How to set financial goals as a couple involves honest communication and shared vision. Schedule regular money talks, align priorities, and create joint goals like buying a house or saving for children’s education while also respecting individual financial needs.

To set business-related goals, start by evaluating your cash flow, expenses, and revenue projections. Define goals such as expanding operations, improving profitability, or growing your customer base. Make sure each business goal aligns with your broader financial strategy.

How to set realistic financial goals means ensuring your targets align with your income, lifestyle, and timeline. Unrealistic goals often lack proper planning, clear metrics, or feasible deadlines. Avoid overwhelm by keeping your goals grounded and practical.

Absolutely. Your financial goals should evolve with life changes new job, marriage, business growth, etc. Regularly reviewing your progress helps you adjust and stay focused on what truly matters.

Yes, many free tools and templates exist online to guide you in setting up financial goals. They often include worksheets for budgeting, tracking savings, or mapping out SMART goals. (Check our upcoming free download section soon!)

That depends on your financial stage. Start with short-term goals (3–6 months), then medium-term (1–5 years), and long-term goals (5+ years). Planning for the future is crucial if you’re thinking about how to set financial goals for your future or retirement.

There’s no one-size-fits-all, but combining a clear vision, SMART goals, regular reviews, and strong habits will always give you an edge. Whether you’re focused on how to set financial goals for personal success, business growth, or long-term stability, structure and intention are key.

The best way to set financial goals is to use the SMART framework: Specific, Measurable, Achievable, Relevant, and Time-bound. Start by reviewing your income, expenses, and debts, then define clear priorities. Breaking big goals into smaller milestones makes them easier to track and achieve.

The 50/30/20 rule means spend 50% of income on needs, 30% on wants, and save or invest 20%. This balance helps you cover essentials while still building long-term savings.

The 1-2-3-4 financial rule is a budgeting method using 10% for insurance, 20% for savings and investments, 30% for housing, and 40% for daily expenses. This structure helps balance protection, growth, and lifestyle needs.

The 5 keys to building strong financial goals include applying the SMART method (Specific, Measurable, Achievable, Relevant, Time-bound) to shape clear targets, dividing big objectives into smaller milestones, designing a budget that aligns with those goals, reviewing your progress often, and staying adaptable so your goals fit life’s changes.

11. Conclusion

Learning how to set financial goals is one of the most powerful steps you can take to secure your financial future. Whether you’re saving for an emergency fund, planning for retirement, or growing your business, having a clear roadmap gives you direction, discipline, and purpose.

Remember:

- Begin with a solid understanding of your current financial situation.

- Use SMART goals to make your vision actionable and trackable.

- Customise your goals to suit your lifestyle, whether personal, couple-based, or business-focused.

- Use tools, templates, and habit-building strategies to stay on course.

- Most importantly, stay flexible and keep learning as your financial journey evolves.

At H2T Funding, we believe in providing unbiased, practical guidance that empowers traders and investors at every stage. This guide was crafted for beginners who are ready to turn intention into action and build a sustainable financial plan that aligns with their goals.

And don’t forget to check out our Budgeting Strategies category for practical guides on managing money, avoiding mistakes, and building long-term financial stability.

Now that you know how to set and achieve financial goals, the next step is simple: Start today.