Got a big goal coming up in the next six months? Maybe it’s a down payment, a trip you’ve been dreaming of, or simply building your first emergency fund. At first glance, saving $5,000 in 6 months feels overwhelming, but with the right approach, it’s more doable than you think.

In this guide, H2T Funding will break the number down into smaller, realistic steps and share tools that make the process easier. By the end, you’ll see a clear path toward your goal and know exactly how to save 5000 in 6 months without feeling stuck.

Key takeaways

- Saving $5,000 in 6 months equals about $833 per month, $192 per week, or $28 per day.

- The steps for how to save 5000 in 6 months include assessing your finances, cutting expenses, boosting income, automating savings, and tracking progress.

- Cutting expenses and adding extra income are the two fastest ways to stay on track.

- After reaching $5,000, use part of it for your goal, reinvest through index funds or a side project, and keep some in an emergency fund.

1. Why save $5,000 in 6 months?

Setting a clear target like $5,000 in six months gives your savings a purpose. People often ask how to save $5000 in six months. And the answer usually involves linking the money to a goal: paying down debt, building an emergency fund, or preparing for a big move.

Using tools like a free debt payoff tracker can help you visualize your progress toward eliminating debt. An emergency fund calculator makes it easier to see how much you need to save for unexpected expenses.

Having a number and a deadline makes the goal concrete instead of just a vague “save more money.”

Beyond the financial side, hitting this milestone builds confidence. You’ll feel more in control of your money and less anxious about the future. Compared to open-ended saving, a six-month challenge creates urgency, structure, and the motivation you need to actually follow through.

2. Break down your savings goal

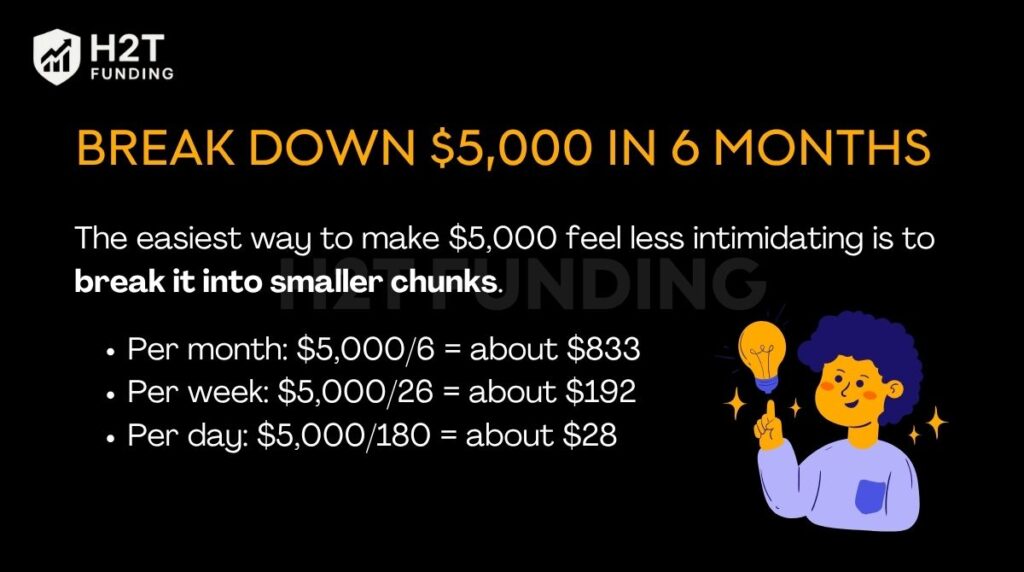

The easiest way to make $5,000 feel less intimidating is to break it into smaller chunks. Many people wonder: How much to save to have $5000 in 6 months? The answer looks simple when broken down.

- Per month: $5,000/6 = about $833

- Per week: $5,000/26 = about $192

- Per day: $5,000/180 = about $28

To make this more relatable, let’s consider typical U.S. living expenses. The average monthly rent for a one-bedroom apartment in a mid-sized city is around $1,200–$1,500. Groceries for one person may cost about $300–$400 per month. Utilities, transportation, and insurance could add another $400–$600.

If your monthly net income is $3,500, saving $833 a month might mean cutting back on dining out, subscriptions, or finding ways to earn extra income on the side.

Creating a simple tracker or a “how to save $5,000 in 6 months” chart can help you visualize your progress. You can also follow weekly budgeting tips to better manage your spending and find areas to save.

Once you know the numbers, the next step is to assess your current situation. Write down your net monthly income and all essential expenses. Compare what you can already save with the numbers above. If there’s a gap, you’ll know whether to cut costs, boost income, or combine both strategies to stay on track.

Continue reading: How much of my paycheck should I save? Smart saving tips

3. How to save 5000 in 6 months

Saving $5,000 in six months may feel like a stretch. But a clear plan makes it possible. If you’ve ever asked yourself: How can I save 5000 in 6 months, the steps are straightforward. Here’s the roadmap you can follow to reach your goal:

- Assess your current financial situation

- Reduce expenses in key categories

- Increase your income

- Use saving tools and automation

- Track progress and stay motivated

Many people use this roadmap to successfully save 5000 in 6 months. Some even challenge themselves to save 5,000 in 6 months or more.

So, if you ready to take action? Let’s dive into each step in detail.

3.1. Assess your current financial situation

Before you start saving, take a close look at your money flow. Knowing exactly what comes in and what goes out will help you spot areas where you can free up cash for your goal.

- List your income sources: Salary, side hustles, freelance work, or any passive income.

- Write down fixed expenses: Rent, utilities, insurance, subscriptions.

- Track variable spending: Food, shopping, entertainment, and travel.

- Spot the leaks: Small charges like ATM fees, unused memberships, or impulse buys can drain more than you realize.

This snapshot shows whether you’re already close to saving $833 a month or if there’s a gap. Once you see the numbers clearly, you can decide what to cut or how much extra income you need to reach $5,000 in six months.

3.2. Reduce expenses: 3 categories to cut down

Cutting costs is often the fastest way to free up money for savings. By focusing on the right categories, you can trim 15–30% of your spending without sacrificing your quality of life.

- Fixed costs: Negotiate lower rent, switch to a cheaper apartment, or review your insurance plans for better rates.

- Flexible costs: Limit dining out, reduce shopping splurges, and swap expensive entertainment for low-cost or free options.

- Non-essential costs: Cancel unused app subscriptions, avoid bank fees or ATM charges, and pause luxury purchases for now.

Even small adjustments in each area can add up quickly. Redirect those savings straight into your dedicated account to stay on pace with your $5,000 goal.

For example, I took a hard look at my bank statement and noticed I was losing about $40 a month on streaming services. One of them was even a free trial I had completely forgotten about.

Just by canceling the subscriptions I wasn’t using and swapping a few takeout nights for home cooking, I freed up an extra $120 each month. That money went straight into my savings.

Read more:

3.3. Increase income: Add an extra $200–500/month

If your current salary isn’t enough to set aside $833 each month, boosting income is the next step. Adding even a few hundred dollars can close the gap and make your savings plan realistic.

- Freelance online: Offer skills like writing, design, translation, or tutoring on platforms such as Upwork or Fiverr.

- Part-time work: Pick up weekend shifts at local cafés, retail shops, or delivery services.

- Sell unused items: Declutter your home and list clothes, gadgets, or furniture on online marketplaces.

- Small business ideas: Try selling handmade products, dropshipping, or simple delivery gigs.

One of my friends, who’s a natural teacher, decided to try teaching English online. She only put in a few hours on the weekends but was able to consistently bring in an extra $300 a month. That one side hustle made a huge dent in her savings goal, covering over a third of what she needed.

For more inspiration, you can explore practical ways to make extra income while working full-time. Even one new income stream, no matter how small, can accelerate your savings and help you reach $5,000 in six months faster.

3.4. Use smart saving tools and automation

Smart systems make saving consistent and less stressful. When you separate your savings and set up automatic processes, you don’t have to rely on willpower alone.

- Open a separate savings account: Keep your $5,000 goal separate from your everyday spending to avoid temptation.

- Automate transfers: Schedule a transfer to savings right after payday so you never forget or overspend.

- Use budgeting apps: Tools like YNAB, GoodBudget, or Money Lover help you track spending, plan categories, and stay on target.

Automation guarantees steady contributions, while apps give you visibility and control. Together, they make it far easier to stick with your six-month plan.

3.5. Stay on track and track your progress

Consistency is key when aiming for a $5,000 goal. Regular check-ins help you see how far you’ve come and keep your motivation alive.

- Use a savings chart or tracker: Mark your progress weekly to visualize growth.

- Celebrate milestones: Reward yourself modestly when reaching $1,000, $2,500, and finally $5,000.

- Record your journey: Keep a spending journal or try systems like the envelope budgeting method to note wins and setbacks.

Small celebrations and regular reviews remind you why you started. Staying engaged with the process ensures you won’t lose momentum during the six-month challenge.

Pulling these steps together gives you a practical framework for saving $5,000 in six months. The key is to stay disciplined and review your progress often. With a clear plan and steady action, reaching $5,000 is not just possible; it’s within your control.

4. Tips to stay motivated for 6 months

Saving for half a year can feel long, so keeping motivation high is just as important as the plan itself. Small tricks can keep you focused and help you avoid losing steam along the way.

- Visualize your goal: Print photos of your dream trip, new home, or car, and place them where you’ll see them daily.

- Tell a friend: Share your goal to create positive accountability. The gentle pressure of someone checking in can keep you consistent.

- Avoid big temptations: Stay away from flash sales, unnecessary loans, or high-interest credit offers that could derail progress.

Motivation fades without reminders. Keeping your goal visible and surrounding yourself with support makes the six-month journey much easier to stick with.

Beyond the common tips above, I also have a trick that works surprisingly well: open a “fun account” linked to your savings goal. Each time you hit a milestone, say $1,000 or $2,500, you move a very small amount (like $20–30) into this account.

That money is only for guilt-free rewards, like a nice dinner or a movie night. It keeps you excited to reach the next milestone, while still protecting the bulk of your savings.

5. What to do with $5,000 after saving

Reaching your $5,000 target is a big achievement, but you may already be thinking ahead. If you’re wondering how to save 6000 in 6 months, the same principles apply, just push your monthly savings a little higher and reinvest smartly.

A balanced way to manage the funds is to split them into three parts, similar to the 50/30/20 method:

- 50% for your main goal: Use it for the purpose you saved, like a trip, a down payment, or paying off debt.

- 30% for investments: Put money into index funds, mutual funds, or a long-term savings account to grow your wealth.

- 20% for emergencies: Keep this in a high-yield savings account to cover unexpected expenses.

You can also set aside a portion for personal growth, such as courses, certifications, or tools that increase your earning potential. Turning savings into an investment in yourself often brings the best long-term return.

6. Potential challenges and how to overcome them

Even with a solid plan, saving $5,000 in six months comes with obstacles. Knowing what to expect helps you prepare mentally and practically.

6.1. Limiting spending

Cutting back on expenses is often harder than it looks. Daily habits, peer pressure, or lifestyle upgrades can make it feel restrictive. Over time, decision fatigue sets in, and even small purchases like snacks or subscriptions add up and sabotage progress.

Solution: Create clear spending rules and stick to them. Use the 24-hour rule before buying non-essentials, set cash limits for weekly expenses, and replace costly habits with free or low-cost alternatives. Finding joy in simple activities keeps saving sustainable.

Learning from budgeting mistakes to avoid can also help you stay consistent.

6.2. Unstable income

For freelancers, gig workers, or those on commission, income can vary widely from month to month. High-earning periods make it easy to save, but lean months create stress and can derail your plan. Without consistency, hitting the $833 monthly target becomes unpredictable.

Solution: Base your savings goal on your lowest expected income month. Save a percentage of every paycheck instead of a fixed sum, and build a small buffer fund to smooth out fluctuations. Diversifying income streams or taking quick side gigs can also stabilize cash flow.

For more ideas, check out budgeting for irregular income.

6.3. Losing motivation

Motivation often drops after the initial excitement. Progress may feel slow, or unexpected slip-ups can make you want to quit. Comparing yourself to others who seem to save faster can also drain your energy and confidence.

Solution: Break the journey into smaller milestones and celebrate each one. Use visual trackers or savings charts to see progress at a glance. Share your goal with a friend for accountability, and build habits around saving so it becomes automatic rather than a constant battle.

6.4. Unexpected expenses

Life has a way of throwing curveballs, medical bills, car repairs, or family emergencies. These sudden costs can eat into savings and tempt you to dip into your $5,000 fund. Without preparation, one big expense can set you back weeks.

Solution: Rely on your emergency fund if you have one. If not, adjust your budget temporarily and work to replace the lost amount in the following month. Look for quick ways to bring in extra income or negotiate payment plans for large bills to avoid high-interest debt.

Overcoming challenges is part of the savings journey. Whether it’s cutting expenses, handling unstable income, or staying motivated, each obstacle can be managed with the right mindset and tools. Treat setbacks as temporary, not permanent, and adjust your approach instead of giving up.

7. FAQs

Yes, it’s realistic if you earn enough to save around $833 each month. For someone with a steady income and discipline, cutting expenses and adding side income makes this target very achievable.

The fastest way is to automate savings right after payday. Treat savings like a bill you must pay, then cut flexible spending such as dining out and shopping. This ensures you hit your monthly target before spending on anything else.

It depends on the type of debt. High-interest debt, like credit cards, should be prioritized before aggressive saving. For lower-interest loans, you can balance both, continue making minimum payments, while setting aside money for your savings goal.

Budgeting apps such as YNAB, GoodBudget, and Money Lover make it easier to track spending and allocate funds. A separate savings account with automatic transfers also helps protect your money from being spent impulsively.

The fastest approach for anyone searching for how to save 5,000 in 6 months combines three actions: cutting unnecessary expenses, boosting income with side hustles, and automating transfers. Together, they create consistent progress and reduce the risk of falling behind.

The 100-envelope challenge is a fun way to save. Write numbers 1 to 100 on envelopes, and each day pick one at random. Deposit that amount in the envelope. After 100 days, you’ll have $5,050 saved, just enough to hit the six-month goal ahead of schedule.

8. Conclusion

With the right plan and steady commitment, how to save 5000 in 6 months is completely within reach. Breaking the number into smaller goals, trimming expenses, and boosting income give you a clear roadmap to follow.

It’s all about shifting your mindset. There’s an old saying that goes, “You don’t need to be rich to save, but you need to save to get rich.” Keeping that idea in mind can be a powerful motivator every step of the way.

For more proven methods to manage money and grow your savings, check out the Cash Flow & Saving Strategies section at H2T Funding. You’ll find detailed guides, tips, and tools to keep building your financial foundation.