Creating a budget isn’t about limiting your freedom. It’s about gaining control over your money so you can live life on your terms.

In this step-by-step guide, you’ll learn how to create a personal budget that works in real life, not just on paper.

Whether you’re saving for a vacation, paying off debt, or just trying to stop living paycheck to paycheck, our article will help you build a financial plan that fits your lifestyle. No matter your situation, learning to create a budget is the first step toward financial stability.

Let’s dive in now!

Key takeaways:

- A personal budget is a financial plan that helps you track income and expenses, giving you control over your money and reducing financial stress.

- Creating a budget follows clear steps: calculate your monthly net income, record and categorize spending, set SMART goals, choose a budgeting method, build your plan, track expenses, and review it monthly.

- Build your personalized budget by assigning numbers to each category and using tools like Excel, Google Sheets, or budgeting apps.

- Use free templates, spreadsheets, and beginner-friendly apps like YNAB or Goodbudget to make budgeting easier and more sustainable.

1. What is a personal budget? Why is budgeting important?

A personal budget is a financial plan that outlines your income, expenses, and spending habits.

It helps you track how much money comes in and where it goes. Instead of wondering where your paycheck disappeared to, a budget gives every dollar a job.

Why is budgeting important? Because it puts you in the driver’s seat of your finances. Many beginners often wonder “what does it mean to make a budget?” or even ask “how do I create a personal budget?” as they try to understand the concept and learn how to apply it in everyday life. With a good budget, you can:

- Start managing your money so it doesn’t end up managing you.

- Reduce financial stress by planning for both expected and unexpected costs

- Set and reach short- and long-term financial goals like buying a home or retiring early

I’ll be transparent: Before I made this my profession, I had my own share of financial anxiety. That end-of-month feeling where you’re not sure if there’s enough to cover everything? I’ve been there. Creating a budget was the moment I finally turned on the lights.

2. Step-by-step guide: How to create a personal budget

Creating a personal budget doesn’t have to be overwhelming. This section guides you through a simple, structured process to build a budget that matches your income, spending habits, and long-term goals. Each step is clear and practical, helping you take action with confidence.

These are the key steps to guide your budgeting journey:

- Step 1: Identify exactly how much money you bring home each month

- Step 2: Record all your expenses and group them into categories

- Step 3: Set realistic financial goals using the SMART method

- Step 4: Select a budgeting method that works for your lifestyle

- Step 5: Build a personalized budget plan tailored to your needs

- Step 6: Track your spending regularly to stay on course

- Step 7: Review and adjust your budget each month as needed

Now, let’s get started with step 1.

2.1. Step 1: Figure out how much money you bring home each month

Before you can build a budget, you need to know exactly how much money you have coming in each month. This is your net income, what’s left after taxes and deductions.

A simple way to think about it is:

Gross income – (Taxes + Insurance premiums + 401(k) contribution) = Take-home pay

If you’re salaried, check your paycheck or bank deposit. For hourly workers, multiply your average hours by your hourly wage and subtract taxes.

Have multiple income streams? Add up all consistent income sources: side gigs, freelance work, child support, or rental income. Just be sure to exclude irregular windfalls like tax refunds or gifts.

2.2. Step 2: Write down everything you spend and group it by type

Now, make a list of all the things you spend money on.

Start with bank statements and receipts. Break your expenses into two main types:

- Fixed costs: Rent, mortgage, loan payments, subscriptions, insurance premiums

- Variable costs: Groceries, gas, entertainment, dining out

Don’t forget hidden or irregular expenses, like:

- Quarterly insurance payments

- Annual subscriptions (e.g., Amazon Prime)

- Healthcare expenses

- Holiday gifts or school supplies

You can smooth out these lumpy costs by setting aside a little each month in a sinking fund.

Example: If your car insurance is $600 every 6 months, set aside $100/month to avoid last-minute panic.

Listing and organizing your spending helps you clearly see where your money goes, which is a critical step in how to create a personal budget that actually works. That’s why many people prefer to create a personal budget using simple tools like a monthly budget spreadsheet for better tracking. In fact, many choose to learn how to create a monthly budget in Excel to organize fixed and variable costs more clearly.

2.3. Step 3: Create S-M-A-R-T financial and savings goals

Budgeting without a goal is like running a race without a finish line. Start by defining your financial priorities using SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound)

Short-term goals (3–12 months):

- Save $1,000 for an emergency fund

- Pay off one credit card

- Stick to a grocery budget for 3 months

Long-term goals (1–5 years or more):

- Save $20,000 toward buying your future home

- Become debt-free

- Build a $100,000 retirement fund

Your goals are what make budgeting meaningful. No matter if you’re working with an app or learning how to create a personal financial budget, the SMART framework ensures your goals remain realistic and measurable. Allocate money toward them monthly, and treat them like required expenses. Once your priorities are clear, it’s much easier to set your budget and stick to it.

Example: Emergency Fund Goal – SMART version

Save $1,000 for an emergency fund by setting aside $85 each month for the next 12 months.

- Specific: Save for an emergency fund

- Measurable: $1,000

- Achievable: $85/month is reasonable

- Relevant: Emergency savings improve financial security

- Time-bound: 12 months

Creating SMART goals is at the heart of the budgeting process. Whether you use a budget planner or a simple personal finance spreadsheet, what matters most is consistency and alignment with your priorities.

2.4. Step 4: Choose a budgeting method that fits your lifestyle

There is no best budget, only the budget that works best for you. Think of these methods not as rigid rules, but as proven frameworks. Your job is to find the one that fits your financial personality and lifestyle, and then adapt it.

#1 The 50/30/20 rule

- Allocate 50% of your income to necessary living costs

- Use 30% of your money for fun stuff like dining out and hobbies.

- Budget 20% of your income for savings and debt payments

Example: Let’s walk through a scenario. If your monthly take-home pay is $3,850, you’d spend:

- $1,925 to needs like rent and food (50%)

- $1,155 to wants like gym memberships or Netflix (30%)

- $770 toward your financial goals, like savings or debt repayment (20%)

Great for beginners who want a simple framework.

#2 Zero-based budget

Assign every dollar a purpose. Income – Expenses = $0

Example: Imagine your take-home pay for the month is $4,280

- $1,650 to rent

- $550 to groceries

- $300 to transportation

- $200 to fun money

- $400 to savings

- $1,000 to student loan payments

- Maybe $180 to a Miscellaneous/Buffer category

Best for people who want tight control and visibility over every dollar.

#3 Envelope method

Cash envelope system remains one of the most practical methods, especially for people who struggle with impulse spending. Once the cash runs out, that’s your cue to stop spending. Others combine it with a pay-yourself-first budget for stronger financial capability.

Helps curb impulse purchases, ideal for overspenders.

Example:

You set $400 for groceries and put it in a “Groceries” envelope.

Once the $400 is gone, no more grocery shopping until next month, or you’ll need to adjust another envelope.

#4 Pay-yourself-first approach

Automatically save a set percentage (e.g., 10–20%) before spending anything else.

Perfect if you struggle to save consistently.

Example:

If you make $2,500/month and decide to save 15%, then:

- $375 goes straight into a savings or investment account

- You use the remaining $2,125 for bills, spending, and other expenses

According to a report by the U.S. Consumer Financial Protection Bureau (CFPB, 2021), individuals who set up recurring, automatic transfers to their savings accounts are 1.5 to 3.5 times more likely to hit key savings milestones compared to those who do not automate. This “set it and forget it” approach works because it removes the need for ongoing decisions, making saving a consistent and effortless habit.

Tip: You can stick to one method or blend a couple. The most effective budget is the one you’ll actually follow. If you’re just starting, you might find yourself asking, “What does setting your budget mean?” to better understand how to apply these methods effectively.

2.5. Step 5: Create your personalized budgeting plan

With all your info in hand, you’re ready to build your budget. It’s time to assign actual numbers to each category.

Start with your net income, then subtract fixed expenses, variable expenses, savings, and debt payments. The goal: every dollar is accounted for.

These options can help you create and manage your budget:

- Spreadsheets: Excel, Google Sheets (tons of free templates online). For beginners, tutorials on how to create a monthly budget spreadsheet or how to make a personal budget in Excel can be very useful. You can also download a ready-made personal budget template Excel file to save setup time and start tracking immediately.

- Apps: YNAB (You Need A Budget), Goodbudget

- Printable planners: Ideal for visual learners or those avoiding tech

Tip: If you’re a visual person, use color-coded charts or pie graphs to see where your money’s going.

Remember to budget for fun. Even $50/month for takeout or hobbies helps you stay motivated without feeling deprived.

2.6. Step 6: Track your spending consistently

Making a budget is just the beginning. The real magic happens when you track spending in real time.

Why? Because what you plan and what you actually spend rarely match up 100%.

How to track:

- Manually: Use a spending journal or weekly planner

- Digitally: Link your bank accounts to apps like:

- YNAB (great for zero-based budgeting, $14.99/month)

- Goodbudget (A budgeting app based on the envelope method)

Check in daily or weekly to stay aware. Even a 5-minute check-in can prevent accidental overspending. Using a budget doesn’t mean perfection; it’s about empowerment through awareness of your monthly income and spending trends.

Tracking helps you see patterns, like that daily coffee or recurring subscriptions you forgot about. For many, the best way is to design a system in Excel. Once you know how to create a personal finance spreadsheet, you can monitor patterns visually with charts and summaries.

2.7. Step 7: Check in on your budget each month and make changes as needed

Budgets need to adjust to life’s ups and downs.

Take a look back each month to see what went well and what didn’t. Did you overspend on groceries but underspend on gas? Adjust the next month’s budget to reflect reality, not perfection. Whether you follow the 50/30/20 rule or the 60/30/10 budget, the idea is to adapt the framework to your real life.

Adjust for:

- A raise, bonus, or income dip

- New expenses (e.g., moving, medical bills)

- Seasonal changes (e.g., holidays, school season)

If you stumble, give yourself grace and move forward.

See more related articles:

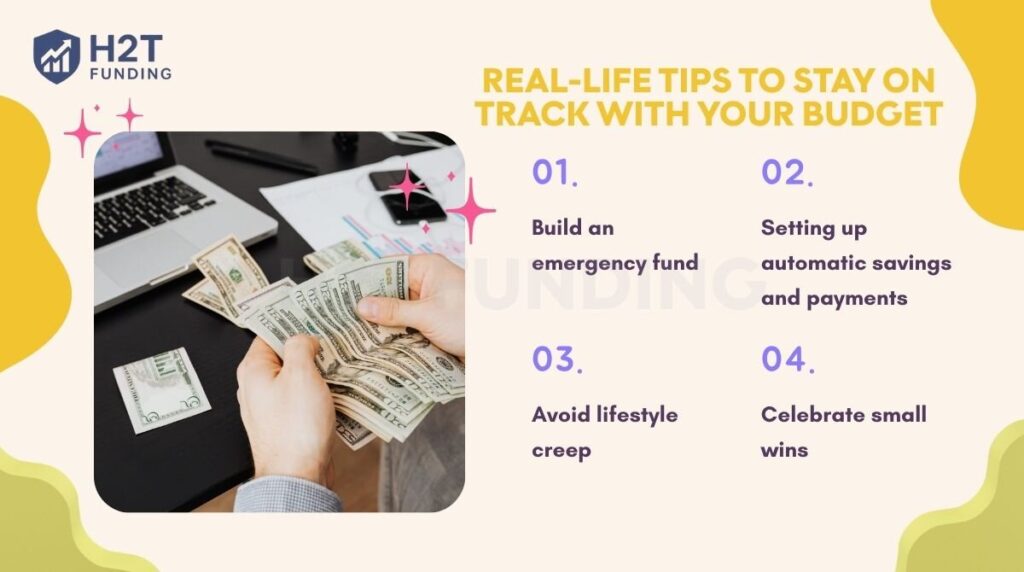

3. Real-life tips to stay on track with your budget

The biggest hurdle I see isn’t the complexity of the budget itself; it’s the psychology of sticking with it. Early on, a single unexpected expense can feel like a total failure, making it tempting to abandon the plan. The strategies below aren’t just “tricks”; they are foundational habits designed to build momentum and resilience.

But over time, I learned a few simple tricks. They helped me stay on track. Most importantly, they didn’t make me feel like I was suffering. And remember, learning how to budget is important for adolescents too, as it builds lifelong money habits early. These are the tips that really worked for me.

- Build an emergency fund

- Set a small target to build momentum, like $500–$1,000, and follow these steps on how to save for an emergency fund.

- Helps you avoid using credit cards for surprise expenses

Example: If your car breaks down and the repair costs $300, your emergency fund can cover it without adding debt.

- Make things easier by setting up automatic savings and payments

- Move money to savings automatically on payday

- Use auto-pay for recurring bills to avoid missed payments

Example: Automatically move $100 into savings on the 1st of each month.

- Avoid lifestyle creep

- Just because you earn more doesn’t mean you should spend more

- Instead, raise your savings rate and keep expenses stable

Example: Get a $200 raise, save $150, and enjoy $50 guilt-free.

- Celebrate small wins

Celebrate small wins to keep your momentum.

Example: After sticking to your grocery budget for three months, treat yourself to a movie or your favorite dessert

Personal insight: A pivotal mindset shift for me was detaching saving from willpower. The real breakthrough came from automation: I set up a modest, recurring transfer, just $50 per paycheck, and effectively “hid“ the money from myself. The account grew without any daily effort on my part. It proved that the most powerful financial systems are the ones you don’t have to think about.

4. Common issues with budgeting and how to handle each

Budgeting isn’t always easy. Here are four common problems people face, and how to deal with each one effectively.

- Irregular income

- Problem: Your monthly income isn’t consistent. Here’s how irregular income budgeting can help you plan better.

- Solution: Base your budget on your lowest-earning month

Example: If income varies from $2,000 to $3,500, plan using $2,000 and save the extra during higher months.

- Overspending

- Problem: You go over budget in flexible categories like food or entertainment

- Solution: Create a small buffer or “miscellaneous” category for unexpected spending

Example: Add $100 as a flex buffer so going over in one area doesn’t throw off the whole plan.

- Partner or family resistance

- Problem: Your spouse or family isn’t on the same page financially

- Solution: Set shared goals and allow each person some individual spending freedom

Example: Give each partner a $100 personal spending budget, no questions asked.

- Budget burnout

- Problem: You feel tired or overwhelmed by tracking every detail

- Solution: Simplify your budget with fewer categories and realistic expectations

Example: Use just five core categories: housing, food, transportation, savings, and personal.

Personal insight: Early in my journey, I fell into the trap of micromanaging my budget, tracking every single transaction. It led to quick burnout. I shifted my approach from granular tracking to a high-level weekly review with just five core categories. This 80/20 approach gave me all the necessary oversight without the mental fatigue, making the entire process sustainable for the long haul.

5. Tools and templates to make budgeting easier

Having the right tools can turn budgeting from a chore into a habit you enjoy. Whether you prefer apps, spreadsheets, or pen and paper, there’s a solution for everyone.

Free budgeting templates

- Google Sheets Template: A budget template like Google Sheets lets you track spending from anywhere with an internet connection.

- Printable planners

Best beginner-friendly apps

- YNAB (You Need A Budget): Based on the zero-based budgeting method. Best for goal-setters.

- Goodbudget: This app brings envelope budgeting into the digital world. Great if you’re a cash-budgeting fan.

Some users prefer learning how to create a personal budget on Excel, while others download apps to handle the details. Both approaches can build strong financial capability as long as you stick with them.

6. FAQs

Begin by writing down every purchase. Then look for one small area to cut, like takeout or streaming services, and redirect that money into savings. Even $20 a week adds up over time.

Begin with your post-tax monthly earnings. List your fixed and variable expenses, then subtract those from your income. Set realistic goals, choose a budgeting method that fits your lifestyle, and track your spending regularly. Adjust your plan each month based on what’s working.

This rule divides your income into three categories: 50% for needs (like rent and food), 30% for wants (like entertainment or hobbies), and 20% for savings and debt repayment. It’s a beginner-friendly way to build structure without overcomplicating your budget.

A good budget is realistic, flexible, and reflects your priorities. It should help you cover essentials, make progress on savings or debt, and still leave room for enjoyment. The most effective budget is one you’ll keep using.

No single rule works for everyone’s money. Many people find success with the 50/30/20 rule, but others prefer the zero-based budget or pay-yourself-first approach. Choose a method that matches your habits and financial goals.

Start with a plan. Know how much you earn and spend, set financial goals, automate savings, and avoid unnecessary debt. Check how your budget’s doing every month. It’s the little things done regularly that add up.

Schedule a casual money conversation. Agree on shared priorities like housing or travel goals. Give each person freedom to manage some categories individually to avoid tension.

Don’t panic. Overspending is common, especially when starting. Look at why it happened and adjust next month’s budget. You’re learning, not failing.

Start by listing your after-tax income and tracking real spending for at least 2–4 weeks to see where money actually goes. Group expenses into needs, wants, and savings/debt, then pick a simple framework (such as the 50/30/20 rule). Automate savings and bill payments, and review your budget monthly to make adjustments. Building an emergency fund early is also essential.

The 50/30/20 rule divides your after-tax income into three parts: 50% for needs, 30% for wants, and 20% for savings and debt repayment. It’s a popular starting point that you can adjust to fit your personal circumstances.

The 70/20/10 rule money guideline allocates 70% of after-tax income to living expenses, 20% to savings or investments, and 10% to extra debt payments or charitable giving. It’s designed for people who want more flexibility in their daily spending while still building financial security.

The 10/20/30/40 rule is a budgeting method that splits income into four parts: 40% for necessities, 30% for discretionary spending, 20% for savings and debt repayment, and 10% for giving or investing. It helps balance essential costs, lifestyle choices, financial security, and long-term growth. Unlike the 50/30/20 rule, this framework makes generosity and investing a distinct priority.

7. Conclusion

Creating a personal budget is a simple but powerful way to take charge of your money. It helps you reduce stress, stay focused on your goals, and spend with more confidence.

When I finally learned how to create a personal budget, I didn’t expect it to make such a difference. But even a basic plan gave me clarity and helped me stop living paycheck to paycheck.

Learn more about money management on our Budgeting Strategies at H2T Funding, where we share practical insights to help you make smarter financial decisions.

If this article was useful to you, leave a like, share it with someone who needs it, or drop a comment below. Your experience might inspire someone else to get started, too.