“I make money every month, but I’m not saving any. So how much of my paycheck should I save? Or put another way, how much of your paycheck should you save each month?” That question is more common than you think. Many people see their salary come in, yet their savings account remains empty at the end of the month.

This guide, H2T Funding, will break down the practical rules you can follow, from the classic 50/30/20 formula to flexible strategies tailored to your own situation. You’ll see why saving even a small portion matters and how to make it work, even if money feels tight right now.

Let’s break down the answer and show you how to start saving smart.

Key takeaways

- Saving from your salary builds financial security, funds emergencies, and supports long-term goals.

- Consistency matters more than hitting a fixed number; begin with 5% of your paycheck, raise it to 10% within a year, and aim for 15–20% as your income grows.

- Building a paycheck-saving plan means managing your budget, saving first, setting clear savings goals, cutting waste, and letting investments grow.

- The 50/30/20 rule is a useful guide, but savings should adapt to your lifestyle, debt, and overall financial planning.

1. Salary and the importance of saving

Your salary is often the main income source, and that’s why the question “how much of my paycheck should I save?” matters to almost everyone. Saving a portion of your paycheck is not just about setting money aside; it’s about building stability for both today and the future.

Regular savings help you prepare for emergencies, achieve personal goals, and develop the habit of financial discipline.

- Emergency fund: A savings buffer protects you from unexpected costs like medical bills, car repairs, or sudden job loss.

- Financial goals: Consistent savings make it possible to reach milestones, from buying a car or funding travel to preparing for retirement or a home purchase.

- Financial freedom: With money set aside, you gain the flexibility to change careers, start a business, or simply enjoy more life choices.

- Financial security: A steady savings habit creates peace of mind, ensuring you and your family are protected from financial shocks.

Even saving small percentages regularly can grow into meaningful wealth over time. The earlier you start, the stronger the habit becomes, and the easier it gets to stay on track.

2. Why is saving a portion of your paycheck crucial?

Saving part of your paycheck is more than a financial habit; it’s a foundation for stability, growth, and overall financial wellness.. When you save consistently, you create a buffer that shields you from unexpected shocks, gives you options for the future, and keeps you out of unnecessary debt.

- Financial safety: An emergency fund ensures you can handle sudden expenses like medical bills, home repairs, or even job loss without falling into crisis.

- Future freedom: With consistent savings, you can plan for milestones such as buying a home, funding higher education, or retiring earlier.

- Debt prevention: Having savings means you’re less likely to rely on credit cards or loans in tough times, protecting you from high-interest debt traps.

- Investment base: Savings act as the seed capital for investing, allowing your money to grow and work for you in the long run.

During the COVID-19 crisis, millions faced job losses, and Federal Reserve surveys showed that in 2020, about 45% of laid-off adults couldn’t cover a $400 emergency expense. The inability to handle even a modest shock was highest among those with less education, underscoring the unequal economic impact of the pandemic.

I experienced this myself. My freelance work, which had been steady, suddenly dried up. Having that emergency fund meant I could still cover rent and bills without going into debt. It gave me the freedom to find the right next job, not just the first one available.

Even saving just 5–10% of each paycheck can create the difference between surviving a crisis and falling into debt. Starting small is far better than not starting at all.

Continue reading: 3 fund portfolio allocation by age: Key strategies

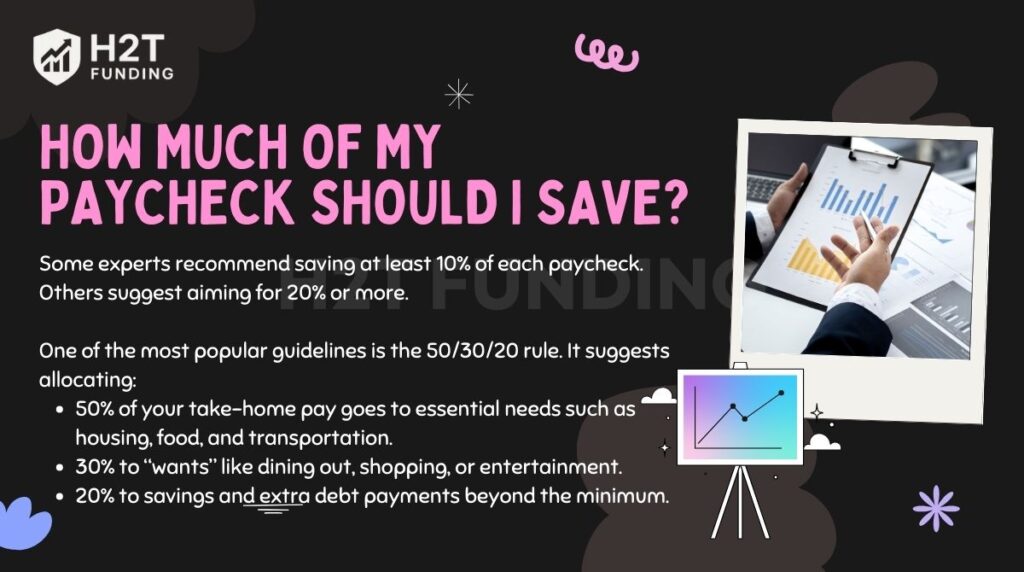

3. How much of my paycheck should I save?

There isn’t a one-size-fits-all answer to how much of my paycheck should I be saving, because the right amount varies by income and goals.

Some experts recommend saving at least 10% of each paycheck. Others suggest aiming for 20% or more. These guidelines help answer related questions like “how much of my income should I be saving” or “what percent of my pay should I save”. The right amount depends on your income level, your fixed expenses, and the goals you’re working toward.

If you’re living paycheck to paycheck, even setting aside a flat amount, like $25 or $50 each pay period, can be a practical first step.

One of the most popular guidelines is the 50/30/20 rule. It suggests allocating:

- 50% of your take-home pay goes to essential needs such as housing, food, and transportation.

- 30% to “wants” like dining out, shopping, or entertainment.

- 20% to savings and extra debt payments beyond the minimum.

Still, the percentages aren’t fixed. For instance, a recent graduate living at home with minimal expenses might save 40–50% for a period of time. On the other hand, someone in a high-cost city may find it difficult to set aside 20% and might need to start with a lower percentage until expenses stabilize.

Your financial goals also shape how much you should save. For short-term aims like a vacation or buying a car, you might increase savings temporarily to hit the target faster. For long-term goals like retirement or a down payment on a house, you may need to put away more than 20% to stay on track with your timeline.

The key takeaway: use rules of thumb like 50/30/20 as a starting point, but adjust based on your real-life situation. What matters most is consistency; saving a portion of every paycheck, no matter the size, builds momentum and long-term security.

4. Factors that affect how much you can save

How much of your paycheck you can realistically save depends on several personal factors. While general rules like 50/30/20 are helpful, your own circumstances ultimately determine what’s possible.

- Income level: Higher income usually means more flexibility to save, but lifestyle inflation, spending more as you earn more, can reduce your savings potential.

- Living expenses: Housing, food, and utilities vary widely. Renting an apartment in a high-cost city leaves less room for savings, while living with family can free up more money to set aside. You can learn how to budget on a low income to manage this better.

- Debt obligations: Student loans, credit card balances, or car payments can limit your ability to save. In some cases, it makes sense to prioritize expenses and pay off high-interest debt before increasing savings.

- Life stage: A new graduate just starting, a young family with childcare costs, or someone preparing for retirement will all face different saving capacities and priorities.

I remember my first job, where my take-home pay was around $2,500 a month. With rent and student loans, I was only able to save about 5%. A few years later, once my loans were paid off and I moved to a more affordable neighborhood, I could increase that savings rate to almost 25%.

That shift taught me that saving isn’t fixed; it grows as your income rises, your debt decreases, and your life stage changes.

See more:

5. What if 20% feels impossible right now?

Not everyone can set aside 20% of their paycheck from the start, and that’s completely normal. If your budget feels too tight, begin with a smaller amount, like 5%, and slowly increase it to 10% or 15% as your situation improves. The key is to start building the habit, even if the amount seems small.

One effective approach is to automate savings. Set up a transfer that moves money from your checking account to a savings account the moment your paycheck arrives. Treat it like a non-negotiable bill; this way, you pay yourself first before spending on anything else.

Cutting back on non-essentials also helps free up extra money. Cooking at home instead of eating out, limiting impulse shopping, or canceling unused subscriptions can easily free up $50–$100 per month. That amount, redirected into savings, adds up faster than you expect.

Another option is to increase your income to boost your savings rate. Freelancing, weekend side gigs, or selling items you no longer need can provide extra cash that goes directly into savings. Over time, these small steps build momentum and move you closer to that 20% goal.

6. How to build a paycheck-saving strategy

Creating a clear strategy helps you turn saving into a consistent part of your financial life. Instead of guessing each month, you’ll know exactly how much to set aside and where it should go. Here are practical steps you can follow:

6.1. Create a detailed budget

Track all income and expenses to see where your money goes. Identifying non-essential spending makes it easier to cut back. Budgeting apps or a simple spreadsheet can provide clarity and keep you accountable.

Personally, I still use YNAB (You Need A Budget) to assign every dollar a job, and I combine it with Google Sheets for a monthly overview. YNAB helps me stay disciplined day-to-day, while the spreadsheet gives me a big-picture view of progress toward long-term goals. This mix of tools keeps me accountable and makes sure I don’t lose track of where my paycheck is really going.

6.2. Automate your savings (Pay Yourself First)

The Pay Yourself First principle is a powerful tool. It simply means you treat your savings contribution as a required bill. Just like you pay your rent, you “pay” your savings account first, before you spend on other things. By doing this, you ensure consistent progress toward goals and remove the temptation to spend first.

I personally use this approach: as soon as my paycheck arrives, 15% is automatically moved into a separate account. Because I never see that money in my “spending” balance, I don’t feel tempted to use it.

6.3. Separate accounts for different goals

Create dedicated savings accounts for purposes such as an emergency fund, retirement, or big purchases like a home or vacation. Dividing your savings makes progress easier to track and prevents mixing long-term goals with short-term needs.

6.4. Cut back on unnecessary spending

Cook at home instead of eating out, limit impulse shopping, and cancel unused subscriptions. A simple rule I follow is the 24-hour wait for online shopping. If I want to buy something that isn’t essential, I add it to my cart and wait 24 hours.

Very often, I find the urge to buy has passed, and I end up saving that money instead. These small habits are powerful when you’re learning how to stop overspending.

6.5. Boost your income

Side hustles, freelance work, or part-time jobs can provide extra cash flow. Upskilling or pursuing certifications may also lead to higher-paying roles and long-term income growth. These are all effective ways to improve your personal cash flow.

6.6. Start investing wisely

Once an emergency fund is established, begin investing to grow your savings. Options like index funds, bonds, or diversified portfolios allow your money to compound over time.

Building a paycheck-saving strategy is about combining discipline and flexibility. By budgeting carefully, automating savings, and balancing both spending cuts and income growth, you create a system that supports your goals in any life stage.

Read more helpful articles:

7. What percentage of my income should I save for retirement?

Most experts recommend saving 10% to 15% of your income for retirement, a clear guideline for anyone wondering how much to set aside each month. This steady habit helps grow wealth over time and ensures a meaningful portion of your salary can be replaced once retirement begins.

Starting early makes a huge difference; thanks to compounding, small contributions in your 20s can grow into a substantial nest egg by your 60s. If you start in your 30s, you may need to raise savings to 15%–20% to catch up. In your 40s or later, higher contributions or working longer may be necessary.

Example: $3,000 monthly salary, saved for 30 years

(6% average annual return, compounded monthly)

| Savings Rate | Monthly Contribution | Value After 30 Years |

|---|---|---|

| 10% | $300 | ~$302,000 |

| 15% | $450 | ~$453,000 |

| 20% | $600 | ~$604,000 |

This shows how a small change in savings rate can greatly increase your retirement balance. The earlier you begin, the more compounding works in your favor.

To reach these targets, choose the right tools. Employer-sponsored plans like a 401(k) often include matching contributions, essentially free money that accelerates progress. If such plans aren’t available, individual retirement accounts (IRAs) or diversified investment portfolios can serve the same role.

The key is consistency. Even if 15% feels out of reach today, saving something every paycheck builds momentum. Increasing contributions with each raise or bonus will gradually bring you closer to the recommended level.

8. FAQs

Start small, even $20 or $50 per paycheck, builds the habit. Focus on cutting non-essentials, automating transfers, and prioritizing an emergency fund first.

If the debt is high-interest, like credit cards, prioritize paying it down while still saving a small amount. This balances reducing interest costs and building financial security.

In this case, aim for tiny contributions, 1%–5%, and review your budget closely. Even a small buffer protects you from relying on debt when emergencies strike.

It’s a solid start, especially if you begin early. Over time, aim to raise it toward 15%–20% as your income grows or expenses ease.

Save a little while paying off debt. An emergency fund prevents new debt if unexpected expenses appear. Then focus on debt repayment more aggressively.

Start with micro-savings, rounding up purchases or saving $5 each week. Look for side income opportunities and focus on breaking the cycle step by step.

Set up an automatic transfer on payday from your checking account to a savings or investment account. This “pay yourself first” approach keeps saving consistently.

Yes. Direct at least part of every raise or bonus into savings. This prevents lifestyle inflation and steadily grows your savings rate without feeling the pinch.

Most experts recommend 10%–15%. The right number depends on your goals, debt, and living costs, but consistency matters more than hitting the perfect percentage.

Yes, over time, it’s powerful. At a 6% annual return, $500 monthly grows to over $500,000 in 30 years. Even without investing, it creates a strong safety net.

9. Conclusion

It doesn’t matter whether you start with a small or large amount; what matters is building the habit and sticking with it. Even saving just 5% of your paycheck today can turn into meaningful results tomorrow if you stay consistent.

So if you’re still asking how much of my paycheck should I save, the answer is: as much as you can, and as regularly as possible. Over time, steady contributions create both security and freedom.

To keep improving your money habits, explore more tips in the Cash Flow & Saving Strategies section of H2T Funding. You’ll find practical guidance to help you budget smarter, save consistently, and work toward lasting financial stability.