Financial literacy tips for beginners include tracking your spending, creating a budget, understanding credit, starting to save early, managing debt wisely, and learning investment basics.

Mastering your money requires the same core principles needed to succeed in other complex fields: discipline and consistency. Think of your financial journey like that of a trader developing their trading skills; the ultimate goal is to build a system that works, similar to how a trader aims to secure a funded account.

Let’s find out!

Key takeaways:

- Financial literacy is the foundation for making informed decisions about earning, spending, saving, investing, and protecting your money.

- Financial literacy tips for beginners include tracking spending, budgeting, saving early, managing debt, and learning basic investments.

- Success in both personal finance and trading comes from risk management, awareness of hidden costs, and consistency.

1. What does financial literacy mean?

Financial literacy means knowing how money works – how you earn, spend, save, invest, and protect it. For beginners, the 5 principles of financial literacy: Earn, Spend, Save and Invest, Borrow, and Protect, provide a clear guide to budgeting, credit, debt, and saving for better daily financial decisions.

Being financially literate means you’re less likely to fall into debt, miss bill payments, or live paycheck-to-paycheck. According to a 2022 report by the National Financial Educators Council, Americans collectively lost over $436 billion due to financial illiteracy. This is especially true for financial literacy for students, as early money management skills help them avoid mistakes with debt and spending.

Common misconceptions

- I don’t make enough to need a budget. -> A budget is crucial, no matter your income.

- Saving only makes sense when you earn more. -> Small, consistent saving builds habits and security.

- Credit cards are bad. -> Misuse is bad; when used wisely, they can build credit and offer rewards.

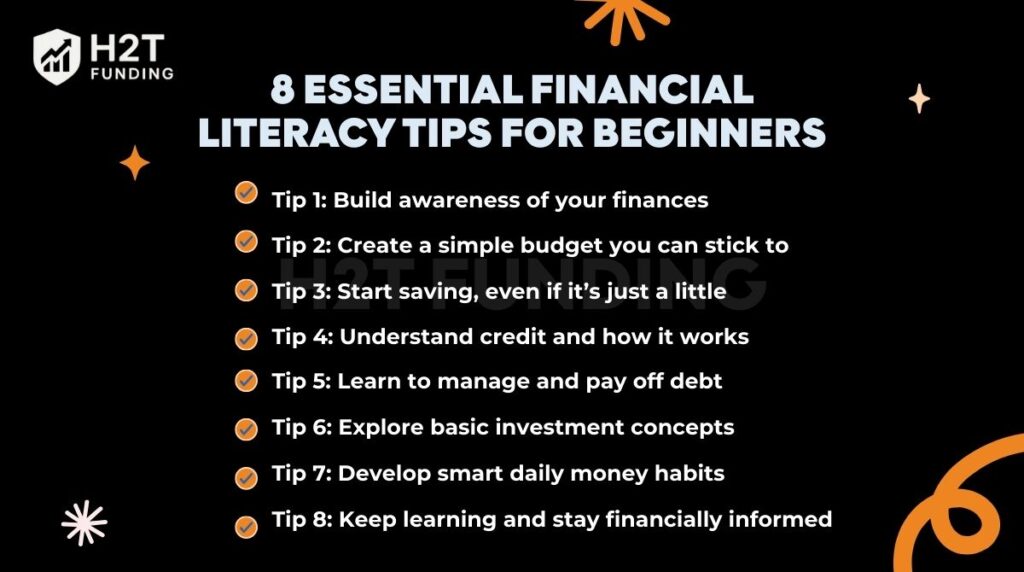

2. 8 Essential financial literacy tips for beginners

Now that you understand the importance of financial literacy, let’s explore 8 actionable tips that every beginner can apply. These aren’t just theories; they’re habits and strategies used by financially successful individuals and endorsed by experts.

Each tip is designed to help you make smarter decisions, avoid common pitfalls, and build a foundation for lifelong financial stability. These are also practical Financial Literacy tips for young adults who want to take control of their money early.

- Tip 1: Build awareness of your finances

- Tip 2: Create a simple budget you can stick to

- Tip 3: Start saving, even if it’s just a little

- Tip 4: Understand credit and how it works

- Tip 5: Learn to manage and pay off debt

- Tip 6: Explore basic investment concepts

- Tip 7: Develop smart daily money habits

- Tip 8: Keep learning and stay financially informed

In fact, smart personal finance shares key principles with disciplined trading. Success in both areas relies on solid risk management. It also requires a sharp awareness of hidden costs. You need a clear understanding of how commission fees or platform fees can impact your bottom line. Let’s dive into each tip and see how you can put them into action.

Tip 1: Build awareness of your finances

Why it matters: You can’t improve what you don’t understand.

- Know where your money goes: Use apps like YNAB, Monarch Money, or even a simple spreadsheet to track every expense for a month.

- Analyze your income and expenses: Break it down by fixed vs. variable costs. This shows where your financial pressure points are and helps you understand how to organize expenses more effectively.

- Identify spending leaks: Do your subscriptions stack up? Are impulse buys eating into your savings? Just as a trader must scrutinize all their trading costs, from data feeds and platform fees to commission fees, you also need to know exactly where your money is going. Unchecked monthly subscriptions and other hidden costs can quietly drain your finances.

Example: Jenny realized she was spending $150/month on subscriptions she barely used. Canceling those helped her start an emergency fund.

Tip 2: Create a simple budget you can stick to

Why it matters: A realistic budget creates clarity and reduces anxiety.

- The 50/30/20 rule explained. This is a clear priority-based budgeting example that helps you learn how to prioritize spending without feeling restricted.

- 50% → Needs (rent, food)

- 30% → Wants (dining out, Netflix)

- 20% → Savings & debt repayment

- Helpful budgeting apps and tools can simplify your finances:

- YNAB (You Need A Budget) – great for envelope-style budgeting

- PocketGuard: tells you exactly what’s safe to spend right now.

- Budgeting mistakes to avoid:

- Forgetting one-time costs: Things like gifts or car repairs can ruin your budget if unplanned. Think of it like a trader preparing for an evaluation process with a prop firm; they must budget for upfront fees like challenge fees or potential reset fees to avoid derailing their progress.

- Making the budget too strict: This often leads to burnout.

Financial expert Dave Ramsey says, “A budget is telling your money where to go instead of wondering where it went.”

See more related articles:

Tip 3: Start saving, even if it’s just a little

Why it matters: Savings = freedom and security.

- Emergency fund vs. savings account:

- Emergency fund: 3–6 months of essential expenses, in a high-yield savings account

- Regular savings: For vacations, goals, or large purchases

- Easy saving habits you can start today:

- Save $5 a day = $150/month

- Use “round-up” features that send spare change to savings

- Automate your savings for success:

- Set automatic transfers on payday → out of sight, out of mind

- Use tools like Chime or Ally Bank that let you split direct deposits

- Think of it as building a small, funded account for yourself, where every deposit creates future flexibility

Fidelity Investments recommends saving at least 15% of your income for long-term financial goals.

Tip 4: Understand credit and how it works

Why it matters: Your credit affects your ability to rent a home, get a loan, or even qualify for certain jobs.

What’s a credit score?

It’s a number from 300 to 850 that shows how reliably you manage debt. A score above 700 is considered good and opens the door to better financial deals.

How to build credit from scratch

- Start with a secured credit card.

- Become an authorized user on someone else’s card.

- Always pay bills on time.

Smart credit habits

- Pay your balance in full to avoid interest.

- Use less than 30% of your credit limit.

- Skip cash advances, they’re expensive.

- Regularly review your credit report for inaccuracies or anomalies.

- Pay your invoices on time to prevent negatively affecting your credit score.

- Avoid opening many credit accounts in a short amount of time.

FICO reports that payment history makes up 35% of your score – never miss a due date.

Tip 5: Learn to manage and pay off debt

Why it matters: Bad debt can trap you; good debt can grow you.

- Good debt vs. bad debt:

- Good: Student loans, mortgage (if used wisely)

- Bad: High-interest credit cards, payday loans

- Snowball vs. avalanche method:

- Snowball: Pay off smallest balances first → boosts motivation

- Avalanche: Pay highest-interest debts first → saves money

- How to steer clear of debt traps:

- Don’t co-sign loans unless you can repay them yourself

- Avoid payday lenders and rent-to-own schemes

These strategies are part of good personal risk management, helping you avoid financial stress while paying down debt. Consumer Financial Protection Bureau (CFPB) warns: payday loans often carry APRs over 400%, steer clear!

Sticking to a debt repayment plan requires the same kind of emotional discipline and strong risk management that separates successful traders from those who accumulate significant trader losses. It’s about following your strategy, not market panic.

Tip 6: Explore basic investment concepts

Why it matters: Saving grows slowly; investing builds wealth.

- Why investing is more effective than just saving:

- Average inflation is ~3%/year

- Savings account interest: 0.5–4%

- S&P 500 average return: ~7–10% over 30 years

- Beginner-friendly ways to invest with less risk:

- Try index funds like Vanguard VTI or Fidelity ZERO, which spread your investment across many companies.

- Use robo-advisors such as Betterment or Wealthfront, which automatically manage your portfolio based on your goals.

- Consider government-backed bonds like I-Bonds or Treasury bonds, which are stable and designed to protect against inflation.

- For traders, demo trading or instant-funded account programs play a similar role, allowing them to test strategies before risking real capital.

- How to start investing with $100:

- Use Robinhood, M1 Finance, or Acorns

- Fractional shares = buy $5 of Amazon or Tesla

Warren Buffett recommends: “Put your money in a low-cost S&P 500 index fund and forget it.”

Tip 7: Develop smart daily money habits

Why it matters: Daily decisions create lifelong results.

- Give yourself time before buying something you don’t need:

- A 24-hour pause can stop you from overspending.

- Ask: “Will this matter in 30 days?”

- Use cash envelopes or spend limits:

- Allocate cash for categories like food or fun

- When it’s gone, it’s gone

- Reflect on wants vs. needs:

- Need: Rent, food, utilities

- Want: Streaming services, branded clothes, gadgets

Psychologist Dr. Brad Klontz emphasizes: “Our money behaviors are often emotional, not logical.”

Tip 8: Keep learning and stay financially informed

Why it matters: Financial education is a journey, not a destination.

- Learn from reliable finance blogs, podcasts, and authors:

- Books: Some popular financial literacy books include “The Simple Path to Wealth” by JL Collins and “Your Money or Your Life” by Vicki Robin.

- Podcasts: Learn on the go with shows like Planet Money and The Dave Ramsey Show

- Blogs: NerdWallet, Mr. Money Mustache

- Follow financial news that affects you:

- Subscribe to Morning Brew, CNBC Make It

- Set Google alerts for interest rate news, student loan changes

- Join online financial communities:

- Reddit: r/personalfinance

- Facebook groups for budgeting or investing

- Discord channels for real-time Q&A

- Educational services provided by prop firms or financial platforms

FINRA’s National Financial Capability Study reveals that people who actively seek out financial knowledge make better decisions with money over time.

3. Real-life financial literacy tips from a beginner’s journey

Sometimes, the most impactful lessons come from personal experience. Here’s my real story showing how learning basic money skills can change everything.

3.1. My wake-up call and first steps

I used to think budgeting was for people with big salaries, not for me. That all changed after I embarrassingly overdrafted my account twice in one month. It was the wake-up call I needed to get serious.

To start, I took a few small steps:

- I downloaded a free budgeting app like PocketGuard to monitor every transaction.

- I separated my expenses into fixed and variable categories. That helped me see that I was spending over $100 each month on dining out.

- I canceled subscriptions I didn’t use and started saving just $10 per week.

3.2. What worked and what didn’t

What helped the most:

- Automating my savings directly from each paycheck made the habit effortless.

- The 50/30/20 budgeting method gave me a clear and manageable structure.

- Reading one personal finance blog every week kept me inspired and informed. In addition, schools and parents should also pay attention to how to improve the financial literacy of students, as this is a crucial foundation for the younger generation.

What didn’t help:

- Setting overly strict budgets made me give up too soon.

- Trying to invest before I had an emergency fund created unnecessary stress.

- Using too many financial apps at once made things more complicated.

3.3. The advice I wish I had heard earlier.

You don’t have to feel ready to take the first step. Focus on building habits before chasing big numbers. And remember that patience is part of the process. The changes might feel small, but over time, they add up.

In the words of Suze Orman: “True financial freedom is not about having millions. It’s about knowing you can handle what life throws at you.”

4. FAQs

It’s knowing how to earn, spend, save, and grow your money. Financial literacy helps you make decisions that support long-term financial health.

It helps you avoid common financial mistakes and gives you confidence in managing your money. Understanding these basics allows you to take control instead of feeling overwhelmed.

You can start by reading beginner-friendly books, following reputable finance blogs, or even taking free online courses. You can also begin by downloading resources such as a financial literacy PDF, which compiles basic concepts and real-life examples.

Most people find the 50/30/20 rule effective. The rule recommends spending 50% on needs, 30% on wants, and 20% on savings or debt. This method maintains balance and flexibility.

You should try to do both. Your first step should be creating a small emergency fund. Then focus on paying off high-interest debt using strategies like the debt snowball or avalanche method while continuing to save consistently.

You can start investing once you have an emergency fund and no high-interest debt. Even small amounts, like $100 in an index fund, can help you get familiar with the process and begin growing your wealth.

Yes. While it won’t make you rich overnight, it helps you build smart habits that protect and grow your money over time. Many successful people started with simple strategies grounded in financial literacy.

The 7% rule in finance is a retirement withdrawal guideline that suggests retirees can withdraw about 7% of their portfolio each year, adjusted for inflation. While it may work in certain cases, it is considered risky because high withdrawal rates can quickly deplete savings, especially during market downturns or long retirements.

The 70/20/10 rule is a simple budgeting method that allocates 70% of income to living expenses, 20% to savings or debt repayment, and 10% to investments or personal development. It helps create balance between daily needs, financial security, and long-term growth.

The five core principles of financial literacy are: earning, spending, saving and investing, borrowing, and protecting. Together, they form the foundation for understanding money, making informed decisions, and building financial stability over time.

The 50/30/20 rule divides income into three categories: 50% for needs, 30% for wants, and 20% for savings or debt repayment. It is a beginner-friendly framework that makes budgeting straightforward while ensuring you prioritize both current living and future security.

5. Conclusion

Learning about money is one of the best investments you can make in yourself. Understanding how to budget, save, use credit, and invest gives you more control and peace of mind.

You don’t have to learn everything right away. Pick one financial habit to start with today. Gradual changes over time can produce big results.

Both in personal finance and trading, discipline and consistency are the foundation. Whether you’re managing a household budget for long-term freedom or aiming for a funded account with fair profit-sharing terms, the principles are the same. You can also refer to a Financial Literacy for Beginners PDF for a well-structured guide that’s easy to follow and put into practice.

If you’re new to managing money, these financial literacy tips for beginners are a great starting point. And if you found these tips helpful, consider sharing them with someone just starting their own journey toward financial confidence.

Explore more financial tips on our Budgeting Strategies at H2T Funding.