In today’s economy, young adults face rising costs, student debt, and unstable career paths. Developing financial literacy for young adults is no longer optional; it’s a core skill for navigating modern life. With the right financial knowledge, you can budget wisely, save consistently, invest with confidence, and protect your financial future.

I remember my early 20s: a mix of freelance gigs and that constant worry before buying groceries. It was exhausting. Learning a few core money management skills was the turning point for me. This guide will share what I learned, blending personal experience with trusted financial principles to help you trade that uncertainty for confidence.

Key takeaways

- Financial literacy for young adults means knowing how to manage money and avoid financial mistakes.

- It is important because it helps with household budgets, reduces debt, and builds confidence.

- In the digital age, tools make money management easier, but a lack of financial literacy in young adults still causes stress.

- Strong money skills bring independence, better decisions, and long-term security.

- Using credit wisely, budgeting, and interactive exercises strengthen financial education for young adults.

1. What is financial literacy for young adults?

Financial literacy for young adults is the ability to understand money and make smart choices about it. This skill helps young people, from high school students to early-career workers, handle daily expenses, plan, and avoid common traps. Lack of financial literacy in young adults often leads to debt, stress, or missed chances to build wealth early.

Instead of guessing, think of it as learning the rules of money. Once you know them, budgeting feels clearer, saving becomes a habit, and investing no longer seems out of reach. To build a strong foundation, focus on five key principles:

- Earning: Understand how to generate income and maximize it. For young adults, this might mean choosing a side hustle, negotiating a starting salary, or exploring freelance opportunities.

- Spending: Spend wisely by prioritizing needs over wants. Young adults can apply this by cutting unnecessary expenses, like canceling unused subscriptions, and sticking to a budget.

- Saving: Set aside money regularly for short- and long-term goals. A young professional might automate $20 a week into a savings account. This helps build an emergency fund and stay prepared for sudden costs like car repairs.

- Investing: Grow your money by putting it into assets that increase in value over time. A young adult could start with a small investment in a low-cost index fund, learning how the stock market works without taking big risks.

- Protecting: Safeguard your finances by managing risks, such as getting insurance or avoiding scams.

For practical tips on stretching every dollar, read our guide on how to budget on a low income, and how to budget on a low income.

2. The importance of financial literacy for young adults

Young adults today face financial pressure earlier than previous generations. Student loans, credit cards, and rising living costs demand smart money choices from the start. Without guidance, it’s easy to overspend, fall into debt, or miss the chance to save for the future.

Key reasons why young adult financial literacy matters are:

- Budgeting and control: Understanding how to track income and expenses helps avoid overspending and creates room for savings.

- Debt management: Knowledge of credit cards, loans, and interest rates reduces the risk of falling into debt traps.

- Smart spending habits: Distinguishing between wants and needs builds discipline and prevents unnecessary financial stress.

- Saving and investing: Learning to build an emergency fund and exploring safe investment options ensures long-term security.

- Building credit history: A good credit score opens doors to better borrowing opportunities and lower costs in the future.

- Confidence and independence: Financial skills give young adults the ability to make decisions without constant stress or dependence on others.

In short, financial literacy for young people is the foundation for freedom and stability. It turns money into a tool for opportunity instead of a source of constant stress.

3. Overview of financial literacy for young adults in the digital age 2026

In 2026, young adults face a far more complex financial reality. Many admit they were never taught how to manage money or build wealth, and some now carry more credit card debt than emergency savings. This lack of early guidance shows how easily young people can slip into financial stress and miss opportunities for stability.

3.1. Lessons from traditional money management

Before the digital era, handling money required discipline and manual effort. Cash was widely used to limit overspending, and people often visited bank branches to update their passbooks or deposit checks.

Bills were paid by mailing checks, and balancing a checkbook was essential to avoid overdrafts. While time-consuming, these methods encouraged careful tracking and responsibility.

3.2. Budgeting in the digital era

Today, mobile banking and fintech tools make managing money faster and easier. Young adults can monitor balances in real time, automate bill payments, transfer money to savings, and receive instant alerts about low funds or unusual transactions. Spending is also categorized automatically, helping users identify habits and improve budgeting.

However, digital convenience has its downsides. Paying with cards or mobile apps can encourage overspending, and automated payments may continue for unused subscriptions. Multiple credit cards or “buy now, pay later” services can also complicate debt management. Staying financially healthy still requires regular attention, even with advanced tools.

Digital tools have transformed personal finance, but discipline remains essential. Young adults need to combine the structure of traditional money habits with the flexibility of modern technology to achieve financial confidence in 2026.

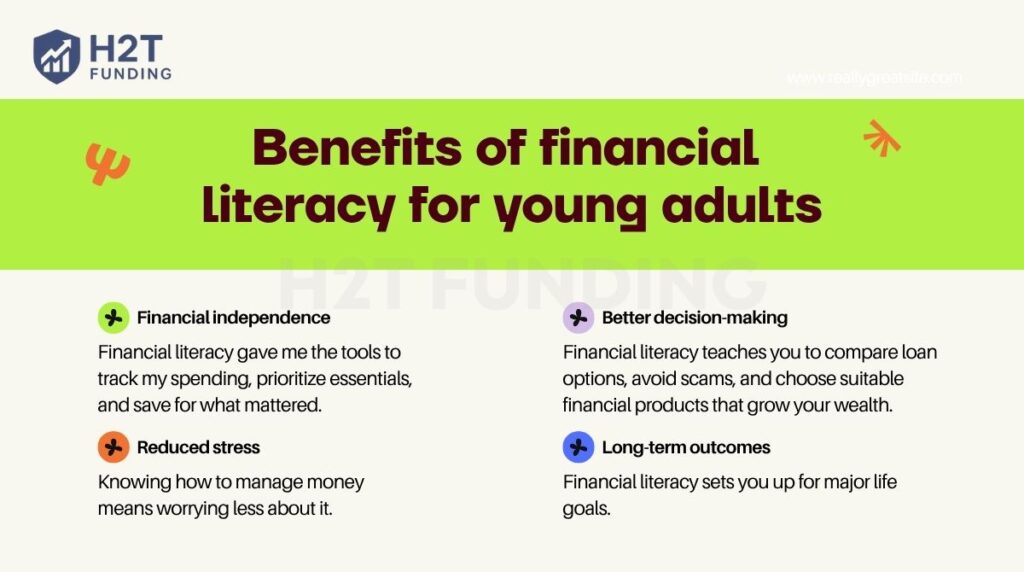

4. Benefits of financial literacy for young adults

Financial literacy equips young adults with the skills to manage money wisely, paving the way for a secure and stress-free future. By understanding budgeting, saving, and investing, you can take control of your finances and achieve big goals.

- Financial independence: I remember the first time I was able to pay my rent and bills entirely on my own; it was a small moment, but it felt like a huge win. Financial literacy gave me the tools to track my spending, prioritize essentials, and save for what mattered.

- Reduced stress: Knowing how to manage money means worrying less about it. A 2023 survey on Ramsey Solutions showed that people “often” (32%) or “sometimes” (42%) felt stress because of money. These numbers also highlight the risks shown in the lack of financial literacy in young adults statistics, where poor money knowledge often leads to debt and anxiety.

- Better decision-making: Understanding money helps you make smarter choices. Financial literacy teaches you to compare loan options, avoid scams, and choose suitable financial products that grow your wealth. It also helps you plan for big purchases, like a car, without falling into debt traps.

- Long-term outcomes: Financial literacy sets you up for major life goals. By saving and investing early, you can retire younger or buy a home sooner. For example, depositing $50 per month into an investment account at age 20 could grow to over $100,000 by age 60. With an 8% return, compound interest turns small savings into significant wealth.

Financial literacy isn’t just about numbers; it’s about building confidence and control. There’s a clear link here: young adults who participate in financial education consistently report feeling more in control and optimistic about their future.

Start learning today, and you’ll be ready to achieve your dreams, stress-free. These points are often highlighted in the importance of financial literacy for young adults’ speech, which can inspire action among students and young professionals.

5. Essential financial skills for young adults

Navigating money as a young adult can feel overwhelming with new responsibilities like rent, student loans, and building a career. Developing a few core skills makes the journey much easier. These include:

- Creating and sticking to a budget

- Saving early and building an emergency fund

- Using credit responsibly

- Starting to invest, even with small amounts

Mastering these basics not only reduces stress but also sets the foundation for long-term financial security.

5.1. How to create and stick to a budget

A budget is a plan for your money. It shows what you earn and what you spend, so you can save for goals like a new phone or moving out.

- Track your money: Write down your income (like your job or allowance) and expenses (like food or rent).

- Use the 50/30/20 rule: Spend 50% on needs (rent, groceries), 30% on wants (movies, clothes), and 20% on savings or debt. For example, if you earn $1,000 a month, that’s $500 for needs, $300 for wants, and $200 for savings.

- Focus on needs over wants: Needs are things you can’t live without, like food. Wants are extras, like eating out. Choosing groceries over takeout saves money.

5.2. The importance of saving early

Saving early helps you prepare for surprises and grow your money over time with compound interest, where your savings earn interest, and that interest grows too.

- Start an emergency fund: Save $500-$1,000 for unexpected costs, like car repairs. Keep it in a savings account you can access easily.

- Save a little each month: Even $20 a week adds up. Set up automatic transfers to a savings account to make it easy.

- Cut small expenses: Skip one coffee a week or cancel an unused app subscription to boost your savings.

For example, I saving $50 a month at age 20 with 5% interest could grow to over $40,000 by age 60.

5.3. Using credit responsibly

Credit lets you borrow money, like with a credit card, but you need to use it carefully to avoid debt and build a good credit score (a number showing how reliable you are with money).

- Understand credit: Credit cards let you spend now and pay later, but unpaid balances charge high interest (15-25%). A good credit score (670+) helps you get loans or apartments.

- Pay on time: Always pay your full credit card bill each month to avoid extra costs. For example, paying off a $100 grocery bill right away keeps you debt-free.

- Check your credit report: Look at your credit report once a year for free at AnnualCreditReport.com to spot mistakes or fraud.

5.4. Introduction to investing

Investing means using your money to buy things that grow in value, like stocks.

It’s a way to build wealth, even if you start small.

- The stock market made simple: Buying a stock means owning a tiny part of a company. If the company grows, your money does too.

- Try low-risk options: Index funds or ETFs spread your money across many companies, reducing risk. They’re great for beginners.

- Start small, keep going: Invest $20 a month in an index fund through platforms like Fidelity. With an 8% return, $20 monthly could grow to $30,000 in 30 years.

Learning how to budget, save, use credit wisely, and start investing gives young adults a strong foundation for independence. With practice and consistency, financial literacy becomes a powerful tool for building stability and freedom.

See more related articles:

6. Tools and resources for financial literacy

Learning to manage money doesn’t have to be complicated or costly. Many free or affordable options are available to help young adults strengthen financial skills.

According to global benchmarks like OECD Financial Literacy, building money knowledge early helps reduce long-term risks while supporting healthier financial behavior. These resources simplify budgeting, saving, and investing, preparing you for a stable financial future.

Popular tools include:

- Budgeting apps for tracking income and expenses

- Online courses with free lessons on money basics

- Books offering practical financial advice

- Spreadsheets to create custom budgets

- Banking features that categorize and analyze spending

Start small by picking one tool today and using it consistently to build lasting financial habits.

6.1. Budgeting and expense tracking tools

Keeping track of your money is the first step to financial success. These tools help you see where your money goes and plan your spending.

- Popular apps:

- PocketGuard: A free app that connects to your bank accounts can show how much money you have left after bills and savings. It’s great for beginners and has a simple “In My Pocket” feature to prevent overspending. A premium version costs $7.99/month for extra features like subscription tracking.

- YNAB (You Need a Budget): Uses a zero-based budgeting method, where every dollar has a purpose. It’s hands-on but offers a free year for college students and a 34-day free trial for others. After that, it’s $14.99/month or $99/year.

- Goodbudget: Based on the envelope system, where you assign money to categories like groceries or fun. The free version supports one account and limited categories, while the premium version ($8/month) allows more flexibility.

- Free spreadsheet templates: Spreadsheets are a no-cost way to budget. Sites like Vertex42 and Tiller offer free Excel or Google Sheets templates where you can input income and expenses. They’re customizable and great if you want full control without app subscriptions.

- Bank and credit card tools: Many banks, like Bank of America or Chase, offer free budgeting tools in their apps to track spending and categorize expenses (e.g., groceries, gas). Credit card providers like Capital One or Discover often include spending trackers that show where your money goes, helping you spot trends like overspending on takeout.

I’ll admit I was skeptical of budgeting apps, thinking they were overly complicated. On a whim, I tried one and connected my accounts. The result wasn’t just a chart; it was a clear picture showing over $100 a month vanishing into late-night food delivery and forgotten subscriptions. Seeing it laid out like that was the simple, non-judgmental nudge I needed to make a change.

6.2. Free financial literacy courses for young adults

Free courses are a great way to learn money basics at your own pace. You can also find a variety of Financial literacy for young adults PDF resources online, which summarize key lessons into downloadable, easy-to-read formats. These platforms and programs offer practical lessons tailored for young adults.

- Coursera: Offers free courses like “Financial Planning for Young Adults” from the University of Illinois. Topics include budgeting, saving, and credit. You can audit the course for free, though certificates cost extra. It’s perfect to take about 19 hours to complete for beginners.

- Khan Academy: Provides a free, self-paced financial literacy course with videos and exercises on budgeting, credit, and investing. Lessons are short and easy to follow, making it ideal for teens or young professionals starting out.

- FDIC’s Money Smart: A government-backed program with free curricula for grades 9-12, covering real-world topics like car purchases and college financing. It includes educator guides, student activities, available in English or Spanish, perfect for self-study or classroom use.

- Nonprofits and financial institutions:

- Practical Money Skills by Visa offers free downloadable lessons, games, plus comics on budgeting and saving. These are engaging for young adults and include guides for managing credit.

- Better Money Habits by Bank of America provides free videos and articles on topics like debt management or building credit, designed for young adults navigating their finances.

6.3. Financial literacy books for young adults

Books offer actionable advice and inspiring stories to help young adults master money. Choosing the right Financial literacy for young adults book can provide step-by-step guidance and relatable examples tailored to your stage of life. These beginner-friendly picks are easy to read and packed with practical tips.

- “I Will Teach You to Be Rich” by Ramit Sethi: This bestseller offers a six-week plan for young adults in their 20s or 30s to pay off debt, save, and invest. It’s written in a fun, conversational style with steps like automating savings and negotiating bills.

- “The Millionaire Next Door” by Thomas J. Stanley and William D. Danko: This book reveals how ordinary people build wealth through simple habits like saving and investing. It’s great for young adults because it shows that you don’t need a big income to become financially secure, just smart choices.

- Why these books work: Both books break down complex ideas into easy steps, like setting up a budget or starting to invest. They use real-life examples, like how to save for a car or avoid credit card debt, making them relatable for young adults starting their financial journey.

“I Will Teach You to Be Rich” was actually the first finance book I ever finished, and it changed how I viewed money. I remember following Ramit Sethi’s advice to automate my savings. Within a few months, I had my first emergency fund. Before that, saving felt impossible. The book permitted me to enjoy spending, as long as I was intentional about it

7. Financial literacy FAQs

Financial literacy of young adults means knowing how to handle money wisely. It’s about learning skills like budgeting, saving, managing debt, and investing to make smart financial choices. For example, it’s understanding how to pay bills on time or save for a big goal like a car.

Financial literacy helps young adults avoid debt traps, like high-interest credit card bills, and build wealth over time, such as saving for a house. It gives you confidence to make choices, like picking a low-cost loan. Studies often show a strong connection: young adults with financial skills are significantly more likely to have savings, which directly reduces stress and boosts their sense of security.

Start with free resources like Khan Academy’s financial literacy course or the FDIC’s Money Smart program. Use apps like PocketGuard to track spending. Set small goals, like saving $20 a week or creating a simple budget. Reading books like “I Will Teach You to Be Rich” can also help you learn practical tips.

Teaching financial literacy works best when it’s practical and connected to real life. Encourage young adults to start with simple habits like tracking expenses, creating a budget, and setting savings goals. Parents, schools, or mentors can use tools such as budgeting apps, role-playing scenarios, or even giving small allowances tied to planning tasks.

Financial literacy is important because it gives young adults the skills to manage money wisely and avoid costly mistakes. Without it, many face debt, stress, or poor financial habits that follow them for years. By learning how to budget, save, invest, and use credit responsibly, young adults can achieve independence and create a secure foundation for future goals.

The five core principles are earning, spending, saving, investing, and protecting. Earning focuses on building income. Spending means controlling expenses and avoiding waste. Saving is setting money aside for both short- and long-term needs. Investing grows wealth over time. Protecting involves managing risks through insurance, fraud awareness, and smart financial choices. Together, these principles shape strong money habits.

The 50/30/20 rule is a simple budgeting framework. It suggests using 50% of your income for needs such as rent, groceries, or utilities. Then, 30% goes to wants like dining out or entertainment. The final 20% is reserved for savings or debt repayment.

8. Conclusion: Taking the first step toward financial literacy

Financial literacy for young adults is the key to unlocking a stress-free, secure future. By learning to budget, save, use credit wisely, and invest early, you can avoid debt, build wealth, or gain confidence in your financial decisions.

Think of it less as a problem to solve overnight and more as a skill to build over time. Starting now, even with the smallest step, is how you build momentum. It’s not about achieving perfection, but about making consistent progress toward a future where you are in control.

Ready to take control? Start today by creating a simple budget, signing up for a free financial literacy course like Khan Academy’s, or downloading an app like PocketGuard. Want to dive deeper? Explore more tips at Strategies and Budgeting Strategies on H2T Funding to grow your wealth. Take the first step now and build a brighter financial future!