Surprise costs can pop up when you least expect them. Medical bills, urgent home repairs, or even sudden job loss may disrupt your financial stability. That’s where an emergency fund calculator becomes essential. It enables you to plan more effectively and establish a safety net tailored to your lifestyle and financial situation.

Keep reading to learn what an emergency fund is, discover the best tools and apps to calculate exactly what you need, and learn how to calculate your emergency fund manually.

Key takeaways

- An emergency fund calculator helps you set a clear savings goal based on your monthly expenses and chosen coverage period.

- A realistic emergency fund amount is three to six months of essential costs, but freelancers or single earners should target nine to twelve months.

- Reviewing and updating your fund every 6–12 months ensures it matches changes in income, expenses, or family needs.

- Budgeting methods such as the zero-based budgeting method make it easier to prioritize savings alongside daily spending.

- Popular calculators include NerdWallet, Fidelity, Ramsey, YNAB, Suze Orman’s method, and the NZ calculator, each offering unique features.

- To build your fund: calculate essential costs, choose a coverage period, multiply to set a target, open a separate account, automate transfers, and monitor progress.

1. What is an emergency fund and an emergency fund calculator?

Here is an easy-to-understand explanation of an emergency fund and an emergency fund calculator.

1.1. What is an emergency fund?

An emergency fund is money saved just for urgent financial situations. These can include unexpected medical treatments, critical home repairs, or periods without income. Knowing exactly when to use an emergency fund is crucial; it should only cover genuine, unavoidable expenses.

Financial experts often recommend saving between three and six months of essential living costs.

However, the ideal amount depends on several personal factors such as your employment type, household size, and financial obligations.

You can learn more about building this type of fund in our article on how to start an emergency fund.

1.2. What does an emergency fund calculator actually do?

An emergency fund calculator is a helpful tool that makes this process easier. It allows you to estimate your ideal savings amount based on your monthly expenses and desired coverage period. By using a calculator, you can create a clear and personalized savings goal without guesswork.

I remember my own experience with this. The first time I used an emergency fund calculator, I was surprised to see my expenses were higher than I’d guessed. The tool gave me a clear, if slightly intimidating, target: save about $4,500 for three months of costs.

But seeing that specific number was the push I needed. I set up automatic transfers right away. That simple step of defining a target and starting small eventually gave me the breathing room to handle the unexpected without falling into debt.

2. Key factors in determining your emergency fund

When calculating how much you should have in your emergency fund, several personal and financial factors come into play. Here are some key factors in determining your emergency fund amount:

- Monthly essential expenses: Add up your basic costs like rent or mortgage, utilities, groceries, insurance, transportation, and debt payments. Multiply this total by the number of months you want to cover, usually three to six months. If you’re a freelancer, see these essential budgeting tips for freelancers to plan for irregular income.

- Job stability: If you have a steady, full-time job with benefits, a smaller fund (around three months) may suffice. If you’re self-employed, freelance, or in a high-risk industry, aim for a larger fund of six to twelve months.

- Household dependents: The more people who rely on your income, the higher your monthly needs. Include children, non-working partners, or aging parents in your calculations.

- Health and insurance coverage: If you or your dependents have medical conditions or high insurance deductibles, build in extra funds to cover potential out-of-pocket costs like emergency room visits or medications.

- Debt obligations: Loans and credit card payments won’t pause during a financial crisis. Your fund should include enough to meet these obligations without falling behind.

- Personal comfort level: Risk tolerance varies. Some people feel safe with three months of savings, while others prefer nine or more. Choose an amount that aligns with your comfort and gives you peace of mind.

The right emergency fund amount depends on your lifestyle, job stability, dependents, health needs, and personal comfort level. Considering these factors carefully, you’ll set a savings goal that covers essential expenses and gives you lasting peace of mind in uncertain times.

Using frameworks like the zero-based budgeting method can also help you allocate income effectively while building your emergency reserves.

3. Recommended emergency fund calculator apps and tools for smart saving

Here are some recommended emergency fund calculator apps and tools to help you quickly estimate your savings goal and stay prepared for unexpected expenses. Many of these platforms also offer a free emergency fund calculator, making it easier for anyone to start without upfront costs.

3.1. NerdWallet emergency fund calculator

NerdWallet’s calculator is all about speed and simplicity. If you want a straightforward answer without the fuss, this is a great place to start. Just plug in your monthly expenses, choose your coverage period, and you’ll get a clear savings target in seconds.

3.2. Fidelity emergency savings calculator

Fidelity digs a bit deeper to offer a more personalized recommendation. By asking about factors like your job stability and household size, its calculator helps tailor a savings goal that truly fits your life’s circumstances, backed by a trusted name in finance.

3.3. Ramsey emergency fund calculator

The Ramsey emergency fund calculator is integrated with a budgeting app that tracks your spending habits. It not only helps you set a savings goal but also monitors your progress over time. The free version is sufficient for basic budgeting, making it a practical choice for those who want to start managing their money without upfront costs.

3.4. YNAB (You Need A Budget)

YNAB is a comprehensive budgeting platform that includes powerful tools for emergency fund planning. It focuses on goal-setting and proactive money management, encouraging users to prioritize savings alongside daily expenses. With its 34-day free trial, you can explore its full suite of features before deciding on a subscription.

3.5. Suze Orman emergency fund calculator

Suze Orman does not provide a dedicated emergency fund calculator on her website, but she promotes a very clear approach. She advises calculating your total essential monthly expenses, then building an emergency fund equal to 8–12 months of that amount.

This method goes beyond the common 3–6 month rule, offering greater protection against long-term challenges such as job loss or major life disruptions. You can use her budget analysis tools or any general emergency fund calculator, then multiply the result by 8–12 to set your personal savings target.

3.6. Emergency fund calculator NZ

For those living in New Zealand, the emergency fund calculator NZ is a useful tool that takes into account the local cost of living and typical household expenses. It allows you to enter your monthly spending and preferred coverage period, then provides a savings target suited to New Zealand conditions. This makes it easier for individuals and families to prepare a realistic safety net that matches their lifestyle and financial obligations in the local context.

Tip: Pick the budgeting app that works best for you. If you want simplicity, go with NerdWallet or Fidelity. If you prefer full budgeting integration, try YNAB or EveryDollar.

See more related articles:

4. How to calculate your emergency fund manually

Although the Emergency Savings Calculator offers a quick solution, it is important to understand how to calculate your emergency fund manually. This gives you a clearer view of your financial priorities.

4.1. Multiply monthly essentials by coverage period

The basic formula to estimate your emergency fund is simple. This is sometimes referred to as the emergency fund ratio formula, which helps standardize your savings goal.

Monthly Essential Expenses × Number of Months

For example, if your monthly spending on necessary items is $2,500 and you want to prepare for six months, your target should be:

$2,500 x 6 = $15,000

This number represents your emergency fund goal.

4.2. Rule of thumb compared to customized estimations

Many advisors suggest using the “three-six-twelve” framework:

- Save enough for three months if you have a stable dual-income household. You can quickly figure out this target by using a 3-month emergency fund calculator to get an accurate estimate.

- When you’re the only one bringing in money, build a six-month cushion.

- Save up to twelve months if you are self-employed or your income is highly variable.

Still, a personalized approach is more accurate. Assess your actual needs rather than relying only on general rules.

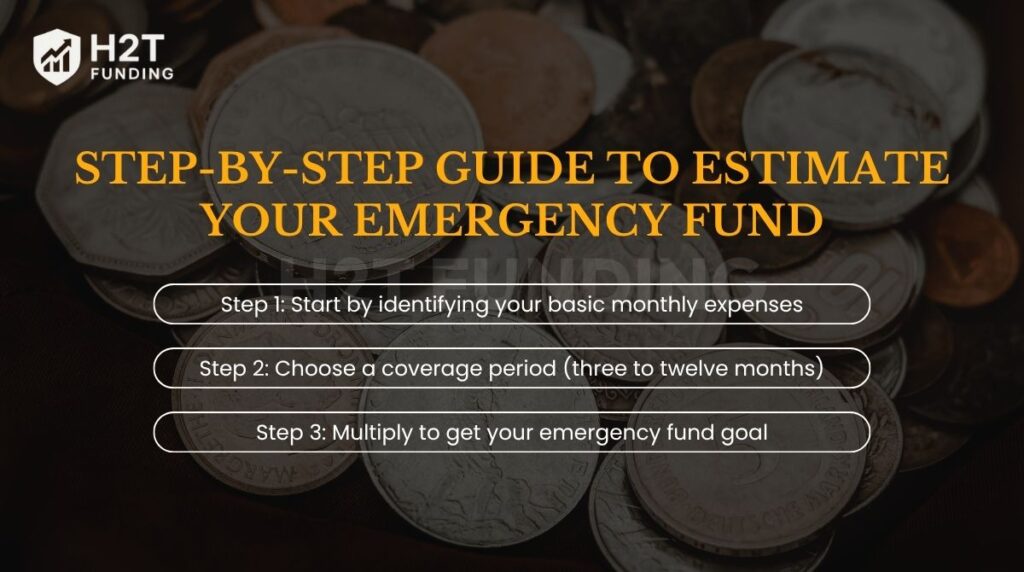

5. Step-by-step guide to estimate your emergency fund

This section walks you through a clear method to estimate your emergency fund based on your actual needs and lifestyle.

5.1. Step 1 – Start by identifying your basic monthly expenses

Begin by calculating the total amount you need each month to cover necessary living costs. This includes rent, groceries, utility bills, transportation, health insurance, and other critical items.

Use the table below to organize your expenses:

| Expense Category | Monthly Cost (USD) |

|---|---|

| Rent or Mortgage | |

| Utilities | |

| Food and Groceries | |

| Insurance and Medical | |

| Transportation | |

| Other Essentials | |

| Total |

Accurately listing your current monthly costs is the foundation for calculating your emergency fund.

5.2. Step 2 – Choose a coverage period (three to twelve months)

The ideal coverage period depends on your financial stability and personal circumstances.

Here are a few recommendations:

| Situation | Suggested Timeframe |

|---|---|

| Two reliable sources of income | 3 months |

| Living off one source of earnings | 6 months |

| Freelancers or contract workers | 6 to 12 months |

| Those with health risks or dependents | 9 to 12 months |

Example: Annabella works independently as a graphic designer. She experiences irregular income from month to month. To stay financially secure, she decides to save enough to cover her expenses for ten months.

5.3. Step 3 – Multiply to get your emergency fund goal

Once you know your total monthly essentials and preferred coverage period, multiply the two numbers together.

Example Calculation:

- Monthly essential costs: $2,000

- Desired coverage: 6 months

- Emergency fund goal: $2,000 × 6 = $12,000

This final amount becomes your personal savings target for emergencies. For some households with higher expenses or multiple dependents, this number could be much larger; for example, a $30,000 emergency fund might be more appropriate.

Read more:

6. FAQs

It is a digital tool that helps you estimate the ideal savings amount for emergencies. It calculates your target based on current expenses and your selected coverage period.

Multiply your total essential monthly expenses by the number of months you want to cover. For example, $2,000 in expenses over six months equals a $12,000 savings goal.

For many people with stable jobs and dual incomes, three months is a good start. However, those with unstable income should aim for six to twelve months.

Yes. Include all fixed financial obligations, such as minimum debt repayments, to avoid credit score damage during a crisis.

There are several trustworthy tools available to help you calculate your emergency fund. Popular options include: NerdWallet Emergency Fund Calculator EveryDollar by Ramsey Solutions Fidelity emergency savings calculator. YNAB (You Need a Budget) These apps offer simple interfaces, personalized recommendations based on your expenses, and some even come with budgeting features. Choose the one that best fits your financial habits and lifestyle. Some people also share their experiences and recommend tools through communities like emergency fund calculator Reddit discussions, where you can find real-life tips.

A realistic amount is three to six months’ worth of essential living expenses. If your income is unstable or you have dependents, aim for more.

Review your emergency fund every 6 to 12 months, or whenever you have a major life or income change, like a new job, move, or added expense.

The 3-6-9 rule is a guideline for building financial security. It means three months of expenses in cash, six months in liquid investments, and nine months in longer-term assets. This layered approach helps balance accessibility with growth.

To calculate your emergency fund, start by listing all essential monthly expenses such as rent, groceries, utilities, insurance, and debt payments. Multiply this total by the number of months you want to cover, typically three to six. Using an emergency fund calculator can simplify this process and provide a clear savings target.

At age 30, the right amount depends on your situation. If you have a steady income and no dependents, three months of expenses may be enough. With a family, mortgage, or variable income, aim for six to nine months.

Whether $10,000 is too much depends on your situation. If your monthly expenses are $2,000, then $10,000 covers about five months, an appropriate amount for most people. However, if your costs are lower, it may be more than necessary. In that case, consider keeping a smaller emergency fund and investing the rest for long-term growth.

7. Conclusion

Think of your emergency fund as a personal financial shield. It protects you from surprise costs and brings peace of mind. Using an emergency fund calculator or calculating manually helps you set a realistic goal and avoid underestimating your needs.

Start by tracking your expenses, choose the right coverage period, and then build your fund step by step. Deciding where to keep an emergency fund is just as important as calculating it. Opt for accounts that are safe, accessible, and offer some interest. Store it safely, review it regularly, and remember that financial security is a journey, not a destination.

If you are ready to build or adjust your safety net, let this guide and our tools lead the way.

For comprehensive guidance on proven methods, explore our Budgeting Strategies or visit H2T Funding for more resources.