If you’re looking for save money challenge ideas, this guide brings together several simple options you can try right away. You’ll see familiar ideas like the 52-week challenge, the $1-a-day habit, round-up savings, and even the 100-envelope method. Each challenge focuses on one thing: helping you save regularly without feeling like you’re doing something complicated.

You’ll find more than 18 ideas here, from beginner-friendly options to challenges that add a bit of fun to your routine. Pick the one that fits your lifestyle, try it for a few weeks, and you’ll start to see your savings grow throughout 2026.

Key takeaways:

- Saving challenges turn saving money into an engaging habit, making it easier to build financial discipline gradually.

- Starting simple with beginner-friendly challenges like the 52-week or $5 bill savings helps build momentum without overwhelming effort.

- Setting clear, specific goals and using tools like visual trackers boost motivation and make saving purposeful.

- Regular tracking, accountability, and automation are essential for maintaining consistency and overcoming motivation dips.

- After saving, prioritize strengthening your emergency fund and paying down high-interest debt before pursuing other financial goals.

1. Why saving challenges work?

Money-saving challenges are structured methods that help you set aside money consistently through simple daily or weekly rules. They work because you only need to follow an easy, manageable routine.

A large financial goal can feel distant, but small steps repeated each day feel achievable. Once the process no longer feels overwhelming, staying committed becomes much easier.

They also interrupt the automatic spending we all fall into. When you’re in a challenge, you tend to stop for a second before buying something you don’t really need. That pause alone can change a lot.

Most people keep going because these challenges build routine. You’re not relying on motivation, just a habit that grows quietly in the background. Over weeks or months, that routine becomes the reason you stay consistent, not the size of the goal itself.

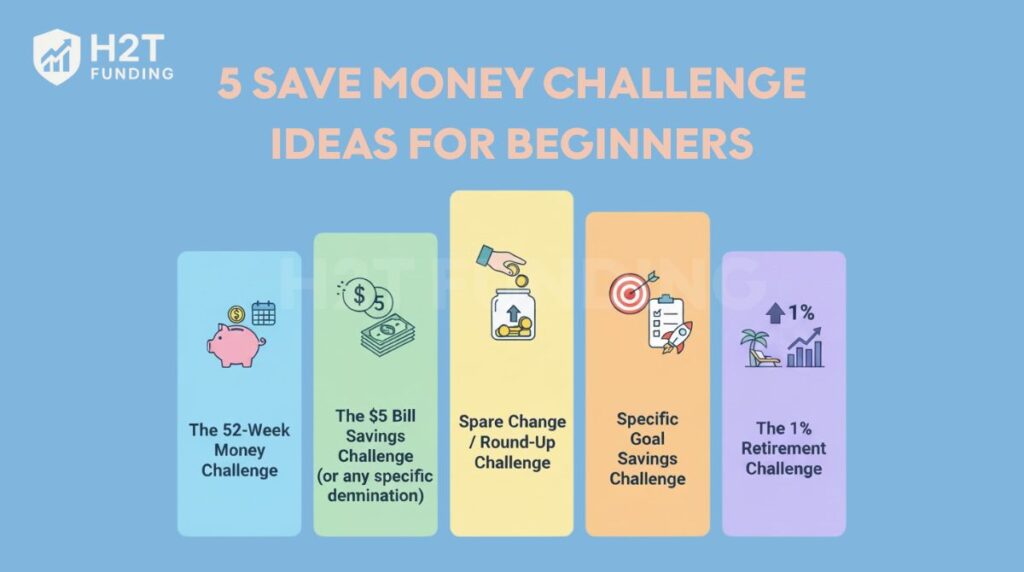

2. 5 save money challenge ideas for beginners

If you’re new to saving, starting with simple challenges can make the process less overwhelming and more rewarding. These savings challenge ideas for beginners focus on easy, low-pressure steps to help you build momentum. Over time, they lay the groundwork for more disciplined financial habits without requiring drastic changes.

Here are five great money-saving challenge ideas to start with:

- The 52-week money challenge

- The $5 bill savings challenge (or any specific denomination)

- The spare change / round-up challenge

- The specific goal savings challenge

- The 1% retirement challenge

Keep reading to explore how each challenge works and choose the one that fits your lifestyle best.

2.1. The 52-week money challenge: Save $1,378 in a year

You’ve probably seen this one around because it’s simple and it works. The idea is that you save a little more each week for a full year.

How it works:

- Week 1: Put aside $1.

- Week 2: Put aside $2.

- Week 3: Put aside $3…

- Keep going until week 52, when you save $52 for that week.

Stick with it and, by the end of the 52nd week, you’ll have saved $1,378 in total.

Potential savings: If you follow this structure diligently, you’ll have accumulated a significant $1,378 by the end of the year.

Variations:

- Reverse 52-week challenge: For those who prefer starting with higher motivation, this variation has you save $52 in week one, $51 in week two, and so on. The amount decreases each week.

- Fixed amount 52-week challenge: If the rising amounts don’t work for you, pick a number and keep it the same all year. For example, saving $10, $20, or $25 every week. The total will simply depend on the amount you choose.

Best for: It’s a great pick if you like having a simple plan and watching your savings grow bit by bit. You start small, get used to showing up every week, and end up with a clear amount you’re working toward.

2.2. The $5 bill savings challenge (or any specific denomination)

For those who enjoy simplicity and a touch of serendipity in their savings, this is one of the most effortlessly implementable save money challenge ideas.

- How it works: The rule is simple. Every time you receive a specific banknote in your change, set it aside instead of spending it. Traditionally, this is a $5 bill, but it could also be a $10 bill, a $1 bill, or an equivalent in your local currency.

- The surprise element: You’ll likely be astonished at how quickly these found notes accumulate. Without actively budgeting for it, you can build a respectable stash by the end of a month or quarter. It feels less like a sacrifice and more like a fun discovery.

- Best for: Anyone who wants a set-and-forget approach that still adds up. It also pairs nicely with weekly budgeting tips; use it to spot patterns in your cash flow while the savings stack up quietly.

2.3. The spare change/ round-up challenge

This is one of the classic save money challenge ideas that proves even small amounts can make a big difference over time. It’s incredibly accessible to everyone.

How it works: There are two main approaches:

- Physical spare change: Collect all the loose coins you receive as change from cash purchases. Designate a jar, piggy bank, or container specifically for this purpose.

- Digital round-ups: For card transactions, you can mentally or, more conveniently, through banking apps, round up your purchases to the nearest dollar (or chosen currency unit). For instance, if a coffee costs $3.40, you’d round it up to $4.00 and transfer the $0.60 difference to your savings. Many modern banking apps automate this, making it seamless.

Implementation: For physical change, simply empty your pockets or wallet into the designated container daily. For digital round-ups, either manually track and transfer the amounts weekly/monthly or utilize an automated app feature.

Best for: Absolutely everyone, but it’s particularly effective for those who frequently use cash or those who want to save small, almost unnoticeable amounts consistently. This is one of the gentlest save money challenge ideas, making it easy to start and maintain.

2.4. The specific goal savings challenge (e.g., vacation fund, emergency fund)

This is one of the most motivating save money challenge ideas because it ties your saving efforts directly to a tangible and desired outcome.

How it works:

- First, you clearly define a specific financial goal you want to achieve. Your goal might be saving for a car, a vacation, an emergency fund, or a high-value item. Treat it like a simple sinking fund. Then use the pay yourself first approach so money goes to this goal before anything else.

- Next, you break down this larger goal into smaller, more manageable weekly or monthly savings targets. A great way to ensure you hit these targets consistently is to automate your savings, setting up recurring transfers that align with your goal timeline. For example, if you want to save $1,200 for a vacation in a year, your monthly target would be $100, or roughly $25 per week.

Supporting tools: Use a quick visual: a progress bar on a sheet, a picture you shade in, or a savings thermometer on the fridge. Seeing the bar move keeps you honest and motivated.

Best for: People who like working toward something specific and want saving to feel concrete, not abstract. It’s simple, motivating, and fits neatly into real life.

This approach works especially well for beginners who are learning financial literacy tips for beginners, because it teaches how to align saving with real-life needs.

2.5. The 1% retirement challenge

A gentle way to start saving for the long haul. Begin with just 1% of your income and get used to the habit before you bump it up.

How it works: Set aside 1% of each paycheck into a retirement account or a holding account, then transfer. After a few months, move to 2%, then 3%, and keep nudging it when life allows. Small steps, no shock to your budget.

Why it works: You build the habit first, then the numbers grow. This technique fits perfectly with anyone learning how to create a personal budget, especially if you’re still adjusting your financial priorities.

Tips for success:

- Automate your monthly contributions to remove decision fatigue.

- Use a high-yield savings account or retirement account for better growth.

- Recheck the percentage every 3–6 months and adjust with raises or changes in expenses.

Best for: Beginners, young professionals, or anyone who struggles with big, abstract goals but does well with steady, bite-sized commitments.

Note: Before cranking up retirement contributions too high, make sure your emergency fund is in decent shape. A few months of expenses in cash keep you from undoing progress later.

3. 4 weekly money-saving challenges

Weekly challenges are an easy way to build savings without burning out. Short goals keep you moving, and wins stack up fast. Think of them as practice reps for your money habits.

Here are four weekly money-saving challenges to try:

- The no-spend challenge

- The pantry / eat-at-home challenge

- The cancel-a-subscription challenge

- The $1-a-day challenge

Explore each challenge below to see how they work and choose the one that fits your routine best.

3.1. The no-spend challenge (weekend, week, or month)

This particular choice among save money challenge ideas is more intensive but can deliver rapid results and powerful insights into your spending habits.

How it works: You commit to not spending any money on non-essential items for a predetermined period. This could be a no-spend weekend, a full week, or even an entire month for the truly dedicated. The core idea is to curb all discretionary spending.

Differentiating essentials from non-essentials: This is crucial for success.

- Essentials typically include: Rent or mortgage payments, utility bills (electricity, water, gas), basic groceries for home cooking, essential medication, and minimal transportation costs for work or critical errands.

- Non-essentials cover: Dining out, takeaway coffees, new clothes or accessories, entertainment (movies, concerts), hobbies that incur costs, impulse buys, and any other spending that isn’t strictly necessary for survival or contractual obligations.

Tips for success:

- Plan free activities: Visit the library, go for a hike, explore local parks, have a board game night, or work on a creative project using materials you already own.

- Meal prep: Ensure you have enough food at home to avoid the temptation of ordering in.

- Communicate your challenge: Let friends and family know so they can support you and understand if you decline certain invitations that involve spending.

Best for: Anyone who wants a quick reset, needs to spot waste, or has to trim costs fast. It’s tougher than it looks, but very revealing.

I committed to a no-spend week, which was tougher than I anticipated. The first few days were filled with cravings for my usual coffee runs and takeout dinners. However, I found joy in rediscovering free activities, like hiking and reading at home. By the end of the week, I felt accomplished and saved over $100, which motivated me to continue being mindful of my spending habits.

3.2. The pantry/ eat-at-home challenge

Food is where budgets leak fast. This challenge flips the script: cook from what you already have before buying more. Clear the pantry, fridge, and freezer; get a little creative with leftovers and odd ingredients. For a set period (a week or a month), skip takeout and pre-made meals.

Benefits:

- Significant cost savings: Dining out and takeaways are considerably more expensive than home-cooked meals. This challenge can free up a substantial amount of your food budget.

- Reduced food waste: It forces you to use items before they expire, minimizing the amount of food thrown away.

- Improved cooking skills: You’ll likely experiment with new recipes and learn to make the most of your ingredients.

Best for: Anyone who wants to trim daily spending, reduce waste, and sharpen basic cooking skills without a full diet on their lifestyle.

I ran this for a month and forced myself to use the random things hiding in the back shelf. Some dinners were great, a few were just okay, but I spent far less on food. Result: about $80 saved and a couple of new go-to meals.

3.3. Cancel a subscription challenge

In today’s subscription-heavy world, this is one of the most relevant and potentially impactful save money challenge ideas for uncovering hidden drains on your finances.

How it works: Take a thorough inventory of all your recurring monthly or annual subscriptions. This includes streaming services (music, TV, movies), gym memberships, software licenses, app subscriptions, magazine or newspaper subscriptions, subscription boxes, and any other service you pay for regularly. The challenge is to critically evaluate each one and cancel those you rarely use, don’t truly need, or can live without. The money saved from these cancellations is then redirected into your savings.

Tips for execution:

- List them all: Go through your bank and credit card statements to identify every recurring payment. Note down the service and its cost.

- Assess usage honestly: For each subscription, ask yourself how often you genuinely use it and whether it provides value proportionate to its cost. Be ruthless!

Best for: Almost everyone in the modern age, but particularly those who suspect they might be oversubscribed or have signed up for services they’ve forgotten about or no longer use. This is one of the save money challenge ideas that can lead to easy, ongoing monthly savings with minimal lifestyle disruption once set up.

3.4. The $1 a day challenge

The $1 a day challenge is one of the simplest and most approachable save money challenge ideas, perfect for anyone who feels overwhelmed by larger or more complex savings systems. Despite its simplicity, it builds powerful long-term habits and proves how small daily contributions can add up over time.

How it works: Set aside $1 every day, cash, a quick transfer, or a rule in your banking app. Do it for a year, and you’ll have $365 without reshuffling your whole budget.

Variations for higher savings:

- $2/day: $730 a year

- $3/day: $1,095 a year

- $4/day: $1,460 a year

- $5/day: $1,825 a year

You can also pair this with the 52-week challenge for a simple hybrid that lands around $2,000 in a year.

Best for: Beginners, students, or anyone who struggles with traditional budgeting systems. It’s ideal for those who need a low-pressure way to build consistency and momentum in their savings journey.

4. 9 creative & fun money savings challenges

Saving doesn’t have to feel stiff. Add a bit of play, and it’s easier to show up. The ideas below break the routine, keep you engaged, and still move the needle on your goals.

There are eight creative and fun money-saving challenges to try:

- The bad habit jar challenge

- The weather savings challenge

- The digital detox challenge

- The 100-envelope challenge

- The digital wallet challenge

- The 365-day penny challenge

- The guess-your-bills challenge

- The roll-the-dice challenge

- The birthday challenge

Dive into each idea below to see how they work and pick the ones that match your personality and lifestyle.

4.1. The bad habit jar challenge

A simple swap: every time you catch a habit you want to cut, swearing, late fees, doom-scrolling, daily takeout, put a set amount into a jar (or transfer it to savings). The slip costs you, and the money goes somewhere useful.

- How it works: Pick one habit and a fine ($1, $5, your call). Keep the jar where you’ll see it. Tally weekly and move the total to your savings account. This simple system also helps you understand how to prioritize expenses more intentionally.

- Good Habit Jar variation: To make it more positive, you can also implement a Good Habit Jar. Flip it on its head: pay yourself when you do the good version: work out, read 20 pages, meditate, cook at home. Small reward, same jar.

- Best for: People who want savings and self-improvement to happen together. It turns mindless routines into conscious choices and a growing balance.

4.2. The weather savings challenge

If you’re looking for save money challenge ideas that are a bit quirky and less structured, this one adds an element of fun and unpredictability.

How it works: Your savings amount for the day (or week) is determined by the weather. There are several ways to approach this:

- Save an amount based on the day’s highest temperature (e.g., $1 for every 5 degrees Celsius, or $0.50 for every degree Fahrenheit).

- Save a fixed amount if it rains, and a different (perhaps smaller) amount if it’s sunny.

- Assign different saving amounts to different weather conditions (cloudy, windy, snowy).

Random and fun: The unpredictability makes it feel less like a chore and more like a game of chance. It can be a lighthearted way to add to your savings without strict adherence to a rigid plan.

Best for: People who enjoy novelty, prefer a less structured approach to saving. Or anyone is looking for savings challenge ideas that inject an element of surprise and lightheartedness into their financial routine. It might not yield massive sums, but every little bit helps!

This quirky challenge added a playful twist to saving money. I saved based on the highest temperature each day, which made me excited to check the weather. Some days I saved a lot, while others were minimal, depending on the weather. It kept me engaged and made the process feel like a game.

4.3. The digital detox savings challenge

In an era of constant online connectivity and targeted advertising, this is one of the save money challenge ideas that addresses modern spending triggers.

How it works: The goal is to cut back on non-essential online time, especially on e-commerce sites, social media, or any platform that encourages impulsive shopping. The money you avoid spending on these unbanned, impulse buys is then notionally (or actually, if you track it) considered saved.

Focus on behavior change: While it’s harder to measure exact savings, the real value is in shifting your behavior from impulsive spending to more mindful buying. This is a key long-term benefit offered by these types of savings challenge ideas.

Tips for success:

- Unsubscribe from promotional emails from retailers you don’t need to hear from regularly.

- Unfollow social media accounts or pages that primarily exist to sell products and frequently trigger your urge to buy.

- Set time limits for browsing shopping apps or websites.

Best for: Individuals who recognize they are prone to frequent, uncontrolled online shopping or are easily swayed by digital marketing. This challenge helps curb that habit, reinforcing more deliberate spending choices.

Reducing my online shopping time was a real eye-opener. I found myself mindlessly scrolling through e-commerce sites, but I replaced that time with hobbies like painting and gardening. I realized how much I could save by avoiding impulsive buys, ultimately saving around $150 over a month.

Make your own challenges

Overall, each challenge taught me valuable lessons about my spending habits and helped me save money while enjoying the process. Beyond these structured save money challenge ideas, remember that you can always get creative and tailor a challenge to your unique lifestyle and spending patterns.

For instance, you might invent a DIY Lunch Challenge, committing to bringing homemade lunch to work or school every day for a month. Or, consider a Transportation Challenge, where you explore cheaper commuting options like cycling, walking, or carpooling. Even a Voucher/Coupon Master Challenge, focused on maximizing discounts on necessary purchases, can free up significant cash.

The most effective money-saving challenge ideas are often those that you personalize, making them both sustainable and enjoyable. The key is to find an approach that doesn’t feel overly restrictive but still pushes you towards your financial goals.

4.4. The 100-envelope challenge

The 100-envelope challenge adds a fun approach to saving and keeps you engaged from start to finish. You prepare 100 envelopes labeled from 1 to 100. Each time you pick an envelope, you save the amount written on it.

- How it works: Shuffle the envelopes to keep things unpredictable. Choose one envelope per day or per week, depending on your schedule. Save the number shown, your daily commitment builds quickly.

- Why it works: The randomness makes it exciting and encourages a stronger savings habit. Watching the envelopes disappear gives you clear visual progress. When completed, you’ll save $5,050 without complex planning.

- Tips for success: Deposit completed amounts into a dedicated savings account or a high-yield savings account for better returns. Make it social by doing the challenge with a friend or partner to build relationship points and stay motivated.

- Best for: People who want a high-impact challenge with a playful twist. It’s ideal for those who enjoy gamified goals and want fast, noticeable savings growth.

4.5. The digital wallet challenge

This modern challenge fits perfectly into cashless lifestyles. Every time you make a digital payment, save a small percentage, usually 5–10%. It’s simple, automatic, and builds steady savings without extra planning.

- How it works: Choose a fixed percentage of each digital purchase. Transfer that amount to your savings account, or set up automatic rules if your banking app allows it. The more you use your wallet, the more you save.

- Benefits: You build savings through daily commitment without feeling restricted. It works especially well when paired with a high-yield savings account. Over time, you’ll see consistent visual progress in your growing balance.

- Best for: Anyone who rarely uses cash and prefers automated systems. It suits busy people who want a low-effort, highly effective saving method that blends into their daily routine.

4.6. The 365-day penny challenge

This challenge proves how tiny amounts can grow into real savings. You start with just one penny on Day 1 and increase the amount by one penny each day. At the end of 365 days, you’ll have a total of $667.95.

How it works:

- Day 1 = $0.01, Day 2 = $0.02, Day 3 = $0.03…

- Continue increasing by one penny daily for a full year.

- The gradual rise keeps the challenge easy and manageable.

Tips for success:

- Transfer your weekly total into a savings account.

- A high-yield savings account helps boost the final amount.

- Use a checklist or tracker to maintain daily commitment.

Best for: People who enjoy structured routines and want a gentle, year-long challenge that adds up without feeling overwhelming.

4.7. The guess-your-bills challenge

The Guess-Your-Bills challenge adds a playful twist to managing household expenses. Before opening a monthly bill, guess the amount. If your guess is off, you save the difference. If you guess correctly or get close, save a fixed amount like $5.

How it works: Choose bills such as electricity, water, internet, or phone. Write down your prediction before checking the actual number. The savings created go into a jar or directly into your savings account. It encourages awareness and more mindful spending.

Why it works: Guessing makes the process engaging and reveals how well you understand your spending patterns. It’s a fun approach that strengthens financial awareness while building a savings habit. Watching your accuracy improve becomes its own visual progress.

Tips for success:

- Try competing with a partner or roommate for relationship points.

- Track bill amounts monthly to spot trends.

- Pair the challenge with energy-saving habits for extra savings.

Best for: Anyone who wants a lighthearted way to manage bills and save more at the same time. Great for people who enjoy gamified challenges and want to become more intentional with monthly expenses.

4.8. The roll-the-dice challenge

This challenge adds a fun approach to saving by letting chance decide your daily amount. You simply roll one or two dice and save the number shown. The randomness keeps the challenge exciting and unpredictable.

How it works:

- Roll one die → save $1–$6.

- Roll two dice → save $2–$12.

- Choose a daily or weekly schedule based on your budget.

Why it works: It feels like a small game rather than a strict rule. The element of chance keeps you from getting bored, and you build a consistent routine over time. Many people find it easier to commit when the decision is left to luck.

Tips for success:

- Use a savings jar or tracker to make it more engaging.

- Transfer totals weekly into your savings account.

- Try playing with a partner for extra relationship points.

Best for: Anyone who enjoys gamified challenges or wants a lighthearted way to save. It’s also great for couples or families; rolling the dice together can spark friendly competition and boost relationship points.

4.9. The birthday challenge

This personalized challenge ties your savings to your age or birthday number. It’s easy to remember, meaningful, and great for building long-term financial consistency.

How it works: Save your age monthly. Someone who is 29 saves $29 each month. Or save your birth date weekly, for example, saving $18 every week if you were born on the 18th. Both methods are simple and scale easily with your life.

Tips for success:

- Automate your monthly or weekly transfers to strengthen your savings habit.

- Review the challenge during your birthday month to adjust goals.

- Do it with a partner or family to add relationship points and stay accountable.

Best for: People who prefer meaningful challenges and want a predictable routine that’s easy to maintain. It’s also a great option if you enjoy tying financial goals to personal milestones.

See more useful articles:

5. 6 steps on how to start a money-saving challenge

Getting started with a money-saving challenge is easier when you follow a clear, step-by-step approach. Before you begin, make sure you understand the basics of how to stop overspending and build healthy habits with simple financial literacy tips for beginners. Here’s a quick overview of the steps you’ll follow:

- Step 1: Choose a challenge that fits your lifestyle

- Step 2: Set SMART financial goals

- Step 3: Track your progress consistently

- Step 4: Use accountability and automation

- Step 5: Visualize your outcome and reward milestones

- Step 6: Stay flexible and review regularly

Scroll down for the full breakdown of each step and how to apply them effectively.

5.1. Step 1: Choose a challenge that fits your lifestyle

Savings challenges aren’t one-size-fits-all. If you’re a meticulous planner, you may enjoy structured goals like a weekly savings tracker. If you’re more spontaneous, a flexible no-spend weekend challenge may be more effective. The key is to match the format with your routines and money mindset. Starting with a simple plan increases your chance of success.

5.2. Step 2: Set SMART financial goals

Clear, measurable goals give you something to work toward and a way to track progress. The SMART framework ensures your objectives are structured for long-term results.

| SMART Element | Example |

|---|---|

| Specific | Save $1,000 for an emergency fund |

| Measurable | Track progress monthly in a spreadsheet or app |

| Achievable | Save $100/month by cutting dining-out expenses |

| Relevant | Aligns with the broader goal of financial security |

| Time-bound | Complete the challenge in 10 months |

Setting up your savings challenge ideas with this clarity helps build consistency and momentum over time.

5.3. Step 3: Track your progress consistently

Tracking keeps you accountable. Whether through a digital budgeting app, a spreadsheet, or even a printed savings tracker, regular updates allow you to see growth, however gradual, which reinforces your commitment.

5.4. Step 4: Use accountability and automation to your advantage

An accountability partner, even just one friend or colleague, can offer the encouragement you need when motivation dips. Automating your transfers on payday also removes the decision-making friction and makes saving a default action.

5.5. Step 5: Visualize your outcome and reward milestones

Keeping your goal visible helps maintain focus. A printed photo of your travel destination, new laptop, or debt-free vision board can be a powerful motivator. Celebrate milestones with small, non-financial rewards, like a relaxing evening or time for a favorite hobby, to maintain morale without derailing your progress.

5.6. Step 6: Stay flexible and review regularly

If your current plan no longer fits your life or feels overwhelming, it’s okay to adjust. Flexibility is often the reason some savings challenge ideas succeed where others fail. Reassess, realign, and keep moving forward.

6. What to do with the money you’ve saved?

Once you’ve completed your savings challenge, start by reinforcing your financial foundation. Use the funds to build or top up your emergency fund, ideally covering 3–6 months of expenses. If high-interest debt is holding you back, consider paying it down to reduce future financial strain.

7. FAQs

The easiest challenge is the $1 a day challenge, because it only requires saving one dollar each day. It’s simple, low-pressure, and helps you build consistency without forcing major lifestyle changes.

Most people can save $50–$300 in 30 days, depending on the challenge they choose. A no-spend weekend or pantry challenge can create quick savings, while small daily deposits provide steady progress.

The 100 Envelope Challenge typically generates the highest total, up to $5,050, when all envelopes are completed. It’s ideal for those who want fast, high-impact results.

Yes. They make saving more engaging, help you build strong habits, and increase awareness of spending patterns. Even small challenges can lead to significant improvements over time.

Absolutely. Many people combine the $1 a day challenge with a weekly round-up or no-spend weekend. Just ensure the mix fits your budget so you don’t feel overwhelmed.

Choose a challenge that matches your lifestyle, automate transfers whenever possible, and track your progress visually. Small wins keep you motivated, and accountability partners help you stay on track.

8. Conclusion

Exploring save money challenge ideas is a simple yet powerful way to improve your financial habits. From the 52-week challenge to no-spend weekends, these strategies turn saving into a fun, achievable goal while helping you gain better control over your spending.

Start building healthy financial habits today with practical tips from the Budgeting Strategies section of H2T Funding. Which save money challenge will you try first? Let us know in the comments!