Before I discovered the Zero-based budgeting Method (ZBB), I was struggling with irregular expenses, constantly caught off guard by unexpected costs, and barely managing to save anything. Money felt chaotic, and I had no clear control over where it was going.

Because of that, I’m here to share the experience and lessons I learned from using ZBB. After just three months of applying this method, I was able to save 25% more, stop overspending, and finally feel in control of my finances.

In this guide, I’ll walk you through exactly how ZBB works, why it’s more effective than traditional budgeting methods, and how you can apply it to your personal finances, even if you’re just looking for a zero-based budgeting example or trying to improve your zero-based budgeting personal finance strategy.

1. What is the Zero-based budgeting method?

Zero-based budgeting (ZBB) is a method where every dollar of income is assigned a specific job. This could mean saving, spending, or investing. The goal is to allocate every dollar so that your budget balances out to zero. This doesn’t mean you have no money; it means every dollar has a purpose.

How it stands out from other budgeting techniques

Unlike traditional budgeting, which rolls over previous budgets or starts with rough estimates, ZBB starts from scratch each month. It forces intentionality:

- You must justify every expense, not just adjust past ones.

- No category gets funded automatically.

- It works especially well for irregular income or fluctuating expenses.

Read more:

2. What you need to create a Zero-based budgeting

To get started with the zero-based budgeting method, you’ll need:

- A record of last month’s income and expenses (bank statements help).

- Budgeting tools like spreadsheets, apps (e.g., YNAB – You Need a Budget, EveryDollar), or pen and paper.

- Clear financial goals, such as debt payoff, savings, or investment targets.

3. Step-by-step guide to creating a Zero-based budget

Creating a zero-based budget is easier when broken into clear steps. Here’s a practical approach to get it done well.

Step 1: Track your earnings and costs

Before assigning any roles to your income, you need to clearly understand your cash flow. This step is about gathering, recording, and organizing your money data from the past month.

- Gather all your income sources from the past month (e.g., salary, freelance, side jobs).

- Collect all your expenses using bank statements, receipts, or budgeting apps.

- Record each transaction manually in a spreadsheet or app.

- Group expenses into categories like rent, groceries, transportation, utilities, entertainment, and subscriptions.

Zero-based budgeting example: The total income for the month is $4,000. Your expenses include $1,200 for rent, $600 for groceries, $300 for utilities, $500 for transportation, $200 for dining out, and $200 for miscellaneous items.

Step 2: Categorize spending

Before building your budget, it’s essential to understand your spending patterns. This step helps you see where your money goes and where you might cut back.

- Split your expenses into:

- Fixed expenses: rent, insurance, loans

- Variable expenses: groceries, dining out, gas, entertainment

- Highlight any categories with non-essential or excessive spending.

- Consider using colors or tags in your tracker for better visibility.

Tip: Color-code fixed vs. variable costs to spot overspending quickly.

Step 3: Give every dollar a purpose

Now that you know your income and expenses, it’s time to allocate your money intentionally. The goal of the zero-based budgeting method is to ensure every dollar is accounted for and used with purpose.

This is where zero-based budgeting personal finance principles shine—forcing clarity and purpose into every line item.

- Take your total income for the month.

- Start assigning money to essential categories first: rent, utilities, transportation, and groceries.

- Next, allocate to savings and debt repayment.

- Assign leftover funds to discretionary categories like entertainment or a buffer.

- Keep adjusting until your total income equals total expenses—zero remains unassigned.

Example: With $4,000 income, you might allocate:

- $1,200 for Rent

- $300 for Utilities

- $500 for Transportation

- $600 for Groceries

- $800 for Debt repayment

- $300 for Savings

- $300 for Entertainment and emergency buffer

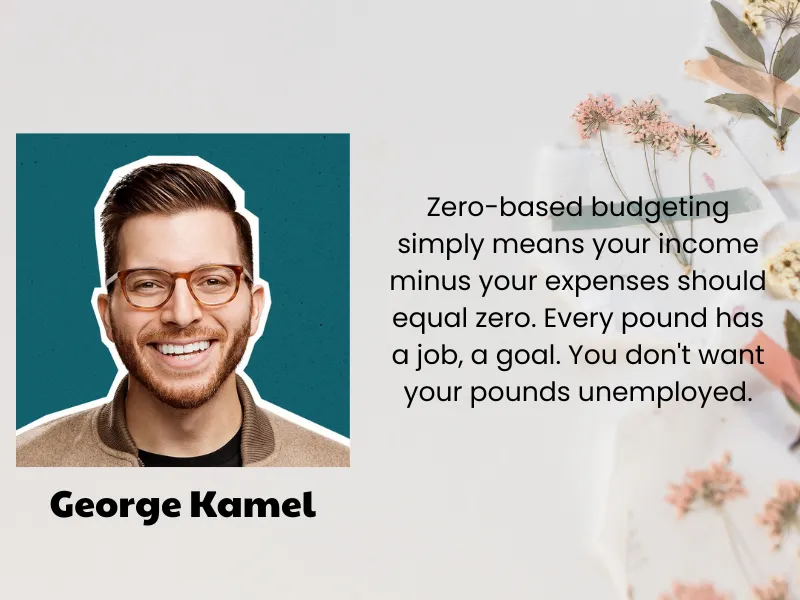

George Kamel, co-host of The Ramsey Show, shares: “Zero-based budgeting simply means your income minus your expenses should equal zero. Every pound has a job, a goal. You don’t want your pounds unemployed.”

Step 4: Adjust and review

Your budget is a living tool. Regular check-ins help you stay on track and adapt to unexpected changes or new priorities.

- Set a weekly reminder to review your actual spending.

- Compare planned vs. actual for each category.

- If you overspend in one category, cut from another to maintain the zero-based approach.

- Update your plan for the next month based on what you’ve learned.

Pro Tip: Use budget apps with alerts to notify you when you approach spending limits.

See more related articles:

4. Zero-based budgeting vs. other budgeting methods

To understand how Zero-based budgeting stands apart, it’s helpful to compare it with other popular methods. The table below outlines key differences between ZBB, traditional budgeting, and the 50/30/20 rule.

| Feature | Zero-based budgeting | Traditional budgeting | 50/30/20 rule |

|---|---|---|---|

| Starting Point | Every month from scratch | Previous month’s budget | Fixed percentages (needs/wants/saving) |

| Expense Justification | Must justify every expense | Often adjusts existing amounts | No detailed tracking |

| Flexibility | High | Medium | Low |

| Best For | Irregular income, control | Predictable income | Beginners |

| Goal-Oriented | Strong focus | Moderate | General guideline |

5. Positive and negative points of Zero-based budgeting method

Zero-based budgeting Method is a powerful strategy, but it comes with its own set of strengths and weaknesses. Before committing to this method, it’s important to understand both sides clearly. Here’s a breakdown of the key benefits and common challenges you may face.

Benefits

- Full control: You decide exactly where every dollar goes.

- Efficiency: No money is left unaccounted for.

- Intentionality: Forces you to evaluate spending decisions consciously.

- Goal alignment: Helps fund priorities like debt repayment or saving.

Challenges

- Time-consuming: Requires tracking and reviewing frequently.

- Complex for variable income: May need frequent adjustments.

- Learning curve: New users may feel overwhelmed initially.

6. FAQs

You control every dollar. This method eliminates mindless spending and aligns your spending with your values.

Yes! Freelancers and commission-based earners benefit greatly because ZBB starts fresh each month.

Absolutely. ZBB enhances cost control and aligns expenses with strategic priorities.

Weekly is ideal, monthly at a minimum. Real-time feedback via apps keeps you on track.

Reevaluate priorities. Cut non-essentials or explore ways to increase income. ZBB highlights where to adjust first.

Not necessarily. A simple spreadsheet works. But apps like YNAB or EveryDollar make it easier and more automated.

7. Conclusion

As someone who applied Zero-based budgeting during a financially stressful time, I can attest to its effectiveness. This method helped me eliminate wasteful spending and build a healthy emergency fund.

Zero-based budgeting goes beyond being just a method. It’s a mindset that forces intentionality, increases savings, and helps you cut waste.

If you found this guide helpful, save it, comment on your experience, or share it with a friend. I personally use EveryDollar and it transformed how I approach money.

Enhance your money management skills by reading more in the Strategy Section and Budgeting Strategies at H2T Funding.