Reaching 40 can feel like standing at a financial crossroads. Many people are quietly asking themselves, “How much should I have saved by 40, and am I already behind?”. It’s a common question that carries both concern and motivation.

Instead of chasing a “perfect” number, the better question is: what savings level will keep you on track for long-term goals while balancing today’s responsibilities? How much money should you have saved by 40 depends on your income, lifestyle, and plans, but financial benchmarks can give you a solid starting point.

This article breaks down what savings targets look like. It also explores the key factors that shape your finances at this age. Plus, you’ll find practical strategies to boost your money confidence, even if you feel you’re starting late.

Key takeaways

- By age 40, aim to have around three times your annual income saved for retirement.

- Maximize contributions to tax-advantaged accounts such as 401(k) or IRAs.

- Small adjustments like saving raises or bonuses can significantly boost your progress.

- Lifestyle changes, including cutting unnecessary costs, help free up money for long-term goals.

1. Why are your 40s crucial for financial planning?

Your 40s are often described as the midlife financial checkpoint. It is the stage when most people begin thinking seriously about long-term goals such as retirement, college tuition for children, or building lasting assets.

At this age, income often reaches its peak, but so do financial responsibilities. Family expenses tend to rise, from education costs to higher living standards and growing healthcare needs. Without a clear plan, it’s easy for money to slip away faster than it comes in.

That’s why your 40s are the right time to minimize risks by building a stronger financial goal, creating an emergency fund, diversifying investments, and balancing immediate family obligations with future security. The decade sets the foundation for whether you’ll enter your 50s confident or stressed about money.

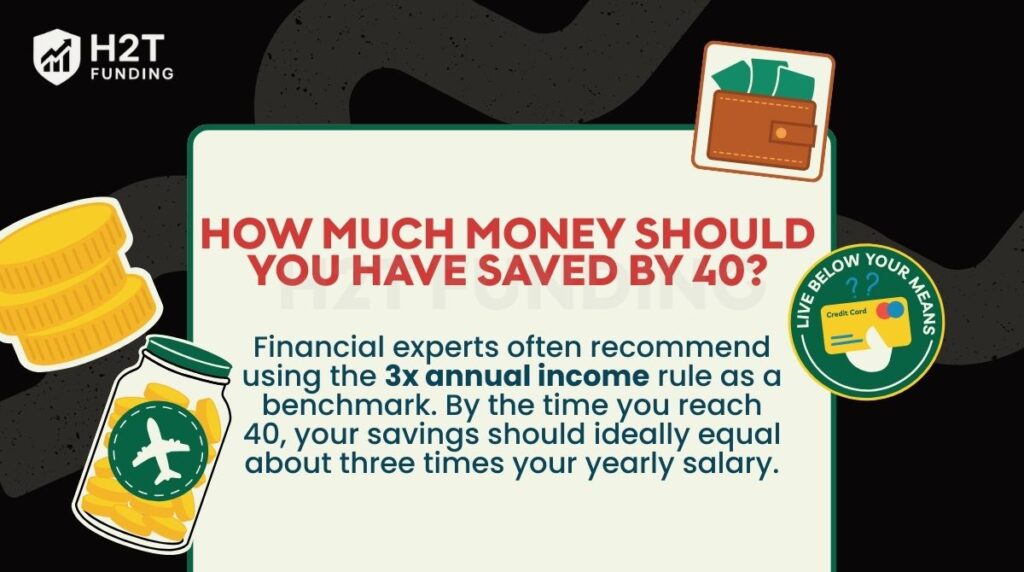

2. How much money should you have saved by 40?

Financial experts often recommend using the 3x annual income rule as a benchmark. By the time you reach 40, your savings should ideally equal about three times your yearly salary.

For example, if you earn $60,000 a year, you’d aim to have around $180,000 saved. This target is designed to keep you on track for retirement while still managing current responsibilities.

So when it comes to the question of how much money should you have saved at 40, let’s be clear: this is a benchmark, not a final exam. Everyone’s financial situation is unique, shaped by career paths, family responsibilities, and what we value most. Use this figure to find your direction, not to judge where you’ve been.

To stay on track, consider applying the 50/30/20 budget rule and regularly track your expenses to adjust your savings plan effectively.

Don’t miss out:

3. Key factors that affect your savings at 40

Reaching 40 is often a turning point in personal finance. Some people arrive at this milestone feeling financially confident, while others are still trying to gain traction. The difference usually lies not in willpower, but in the unique circumstances that shape each person’s money journey.

Understanding these key factors can help you see why your savings may look the way they do and where you can adjust moving forward.

- Income and career path: Your current earnings, job security, and potential for promotions largely determine how quickly you can build wealth. Stable, growing careers often provide more room for long-term savings.

- Family situation: Marriage and children increase household expenses. From daycare to tuition, supporting dependents requires balancing present costs with future financial goals.

- Debt obligations: Mortgages, car loans, and credit cards can eat into savings capacity. Tackling high-interest debt first is essential to free up more money for long-term plans.

- Long-term goals: Aiming for early retirement, funding children’s education, or investing in property all change the level of savings you need by 40.

- Health and insurance: Medical bills or inadequate coverage can derail savings progress. Factoring in healthcare is critical at this age.

- Risk tolerance and investment knowledge: Comfort with risk and understanding of investments affect how much your money grows. Diversification and consistent investing often separate those who stay stagnant from those who build real wealth.

When you consider these factors, it becomes clear why comparing yourself to others rarely tells the full story. What matters most is recognizing your own financial landscape and taking steps to strengthen it. By doing so, you can shift from asking “Am I behind?” to “How do I move ahead?”

Read more:

4. Effective strategies to boost savings and investing in your 40s

By the time you hit your 40s, it’s no longer just about saving what’s left over; it’s about actively shaping your financial future. The right strategies can help you make up for lost time, maximize income, and prepare for major goals like retirement or children’s education.

Below are practical steps to boost savings and investments in this crucial decade.

4.1. Review and optimize your budget

The first step is to re-examine your spending and create a clear monthly budget carefully. Cut back on non-essential expenses and redirect that money toward savings or investments. Even small changes, like adjusting entertainment or dining-out habits, can add up significantly over a year.

You should also optimize recurring bills such as internet, phone plans, or insurance premiums. Negotiating with providers or switching to better deals can free up hundreds of dollars annually without lowering your quality of life.

I’m reminded of a conversation with my own mother. She was convinced her budget was stretched thin, but we spent an afternoon looking at her “automatic” bills. It turned out she was still paying for a premium channel she hadn’t watched in years and was on an old, uncompetitive insurance bundle.

The fix took less than an hour of phone calls, but it freed up over $100 a month. It was a powerful lesson in how the easiest money to save is often the money we’ve forgotten we’re spending.

4.2. Maximize retirement contributions

When asking how much should you have saved by 40 for retirement, these accounts are the engine of your progress. Take full advantage of workplace retirement plans like 401(k) or IRA. These accounts often come with employer matching, which is essentially free money.

If you’re eligible, also consider individual retirement accounts, such as a Roth IRA, to diversify your tax benefits. Increasing your contributions now, even by a few percentage points, can have a powerful compounding effect over the next two decades.

4.3. Diversify your investment portfolio

A common trap I’ve noticed people fall into in their 40s is over-concentration. It’s easy to get excited about a soaring company stock or a popular tech fund and put too much faith in one place.

I’ve learned, both from personal experience and from observing the market, that while this feels great on the way up, it creates a fragile portfolio. Real, lasting wealth is built on a resilient, diversified foundation, not on a single bet.

Pair this strategy with a clear understanding of the pros and cons of saving vs investing to balance risk and return effectively.

May you want to know: 3 fund portfolio allocation by age: Key strategies

4.4. Strengthen active and passive income

Boosting income is often more effective than just cutting expenses. In your 40s, focus on upgrading your skills to qualify for promotions or higher-paying roles. At the same time, explore side hustles or passive income sources, such as freelancing, consulting, or renting out property.

Even a modest side income can accelerate savings when invested in retirement accounts or other assets, creating a compounding advantage over time.

4.5. Manage debt effectively

Think of high-interest debt as a constant headwind pushing against your financial progress. While a mortgage can be a tool to build wealth, credit card debt is often just a drag.

My philosophy is to distinguish between “tool” debt and “drag” debt. Your first mission should be to eliminate that ”drag” debt with intensity. The financial and mental bandwidth you’ll reclaim is enormous.

Once that’s handled, you can look at optimizing your “tool” debt, like refinancing a mortgage for a better rate. But first, cut the anchors holding you back.

Explore more: Free debt payoff tracker printable to stay debt-free

4.6. Create a comprehensive financial plan

Finally, bring everything together into a well-structured financial plan. Define clear goals for retirement and children’s education. For your emergency fund, this is where the question of how much cash should you have saved by 40 becomes critical. Aiming for 3-6 months of living expenses is a non-negotiable part of a solid plan.

Review your plan at least once a year, adjusting for changes in income, expenses, or life events. A written plan not only provides clarity but also keeps you accountable. It turns vague intentions into concrete steps, ensuring your actions align with your long-term vision.

For a simpler start, consider automating your savings with automatic deposits. Consistent, automated contributions make financial discipline easier and less stressful.

In your 40s, saving and investing are less about quick wins and more about consistency. Combining smart budgeting, steady retirement contributions, income growth, and disciplined debt management builds real momentum. With a clear financial plan, you turn this decade into the launchpad for long-term security.

5. Financial goals to focus on in your 40s

Your 40s are a decade where financial clarity matters most. At this stage, your savings and investment decisions have a direct impact on how comfortably you’ll live by the age of 50 and beyond.

Many people wonder “how much money should you have saved by 40?”, but the answer often depends on whether you’re hitting the right goals, not just the right number.

Key financial goals include:

- Expand your retirement funds: Take advantage of 401(k), IRA, or pension insurance to grow future security. The earlier you increase contributions, the more compounding works in your favor.

- Build a college fund for children: Saving for education now prevents future debt and reduces stress when tuition bills arrive.

- Invest in income-generating assets: Stocks, index funds, and real estate offer growth potential and diversify your portfolio beyond traditional savings.

- Protect with life insurance and estate planning: Ensure your family is financially secure and that wealth is transferred smoothly if unexpected events occur.

At the same time, be mindful of bad habits that can quietly slow your progress. Quitting them in your 40s can be just as powerful as hitting new savings goals:

- Overspending on lifestyle upgrades: Constantly chasing bigger houses, newer cars, or luxury items can drain resources meant for the future.

- Relying too much on credit cards: High-interest debt eats away at your ability to save and invest effectively.

- Skipping retirement contributions: Delaying savings now makes it harder to catch up later when the time to compound is shorter.

- Avoiding investments out of fear: Staying only in cash or low-yield accounts keeps your money from growing with inflation.

- Neglecting an emergency fund: Without a safety net, unexpected expenses may force you into debt at the worst possible time.

Breaking free from these habits not only protects your financial health but also accelerates your progress toward long-term stability.

6. How to boost your savings in your 40s

Even if you feel behind, your 40s are still a powerful decade to grow wealth. By combining smart tax moves, extra income, and disciplined spending, you can accelerate savings and close the gap before retirement.

- Leverage tax-advantaged accounts: Max out contributions to 401(k), IRA, or similar plans. These accounts reduce taxable income while letting your money grow tax-deferred, giving you a double benefit.

- Create additional income streams: Explore freelancing, side businesses, or small-scale investments. Even a few hundred dollars a month, when invested, can significantly strengthen your retirement outlook.

- Reinvest your profits: Put dividends, interest, or side income back into investments instead of spending them. This allows compound interest to do the heavy lifting over time.

- Cut unnecessary expenses: Review your lifestyle and trim costs that don’t add real value. Redirecting this cash flow toward savings ensures every dollar works harder for your future. Start small by using budgeting apps or cashback tools to stretch your income further.

When applied consistently, these strategies can transform your 40s from a decade of financial worry into one of confident progress.

Continue reading: 8 the best way to invest 20K short-term success

7. FAQs

No, it’s not too late. While starting earlier is ideal, your 40s still give you 20–25 years to build wealth. With consistent contributions, smart investing, and disciplined spending, you can make significant progress toward retirement security.

A healthy net worth varies by lifestyle and income, but many experts suggest aiming for 2–3 times your annual salary. This includes savings, investments, and assets minus any debts. The key is steady growth, not hitting a “perfect” number.

Financial planners often recommend having about three times your annual income saved in retirement accounts by 40. This helps you stay on track for long-term goals, though personal factors like debt and family costs can shift this target.

Yes, $100k in savings at 40 is a solid achievement, especially if paired with retirement accounts and investments. The real question is whether this amount aligns with your future expenses and retirement goals. For some, it’s enough; for others, it’s just a starting point.

Retiring at 40 with $2 million is possible, but it depends on your spending habits, location, and lifestyle. If you keep expenses low and invest wisely, it may work. However, healthcare, inflation, and unexpected costs must be factored in carefully.

Having $1 million in savings is rare. Studies show that only a small percentage of Americans, often less than 10%, reach this milestone. It’s a high bar, but steady saving and long-term investing can help you join that group.

At 40, you should do both. Savings give you safety and liquidity for emergencies, while investments provide growth for retirement. A balanced approach ensures you’re protected in the short term and prepared for the long term.

8. Conclude

Turning 40 is not too late to build a stable financial future. This stage of life offers both challenges and opportunities, but with the right strategies, you can still create lasting security for yourself and your family.

No matter where you are today, you can start fresh or adjust your financial plan. What matters most is consistency, reviewing your current situation, setting clear goals, and taking steady action.

If you’ve been asking how much money should you have saved by 40, begin by reviewing your current numbers. Set specific targets. Take steady, repeatable actions that compound over time.

For next steps, explore H2T Funding’s Cash Flow & Saving Strategies hub for practical guides on saving, investing, and debt management, so your 40s become the launchpad for long-term security.