If you’re 35 and feel a little anxious looking at your savings, you’re not alone. It’s a common milestone where money questions suddenly feel more urgent, whether it’s buying a house, raising kids, or just planning for a future that doesn’t seem so far away anymore.

So the question is: how much savings should I have at 35? Or more simply, how much should I have in savings at 35 to feel secure?

This guide, H2T Funding, will give you benchmarks from trusted financial institutions, help you measure your current progress, and provide practical strategies to build financial security starting today.

Key takeaways

- At 35, a healthy savings target is around twice your annual income, enough to cover both short-term security and long-term goals.

- Types of savings you should consider at 35 include an emergency fund, retirement accounts, short-term goals, and a down payment fund.

- Boosting savings in your 30s requires avoiding lifestyle inflation, saving 20–25% of income, and exploring extra income streams.

- Personal factors like income level, debt, family responsibilities, and risk tolerance shape how much you really need at this stage.

1. Why is age 35 a financial checkpoint?

Turning 35 often marks the shift from early adulthood to financial stability. By now, many in this age group are balancing financial obligations like mortgages, childcare, or education costs. It’s also when your spending habits start to define your long-term financial health.

It’s also the age where you might start looking at your peers and wondering, “Am I on track?”.

At this stage, society also tends to compare progress, making many ask: How much money should I have saved at 35? To ensure your savings align with your goals, it helps to follow a structured approach and learn more about how to set financial goals.

Ultimately, age 35 is less about perfection and more about alignment. It’s the checkpoint where you balance lifestyle choices with future planning, ensuring that your money supports both present needs and tomorrow’s security.

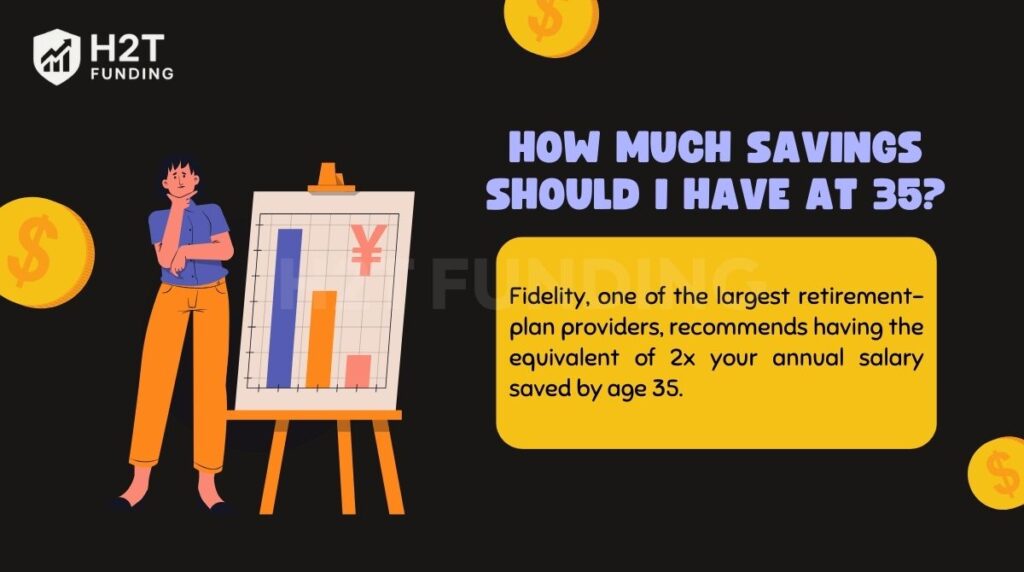

2. How much savings should I have at 35?

Financial experts agree that savings benchmarks are guides, not hard rules. Fidelity, one of the largest retirement-plan providers, recommends having the equivalent of 2x your annual salary saved by age 35.

To put that in perspective: if you earn $50,000 a year, the goal would be to have about $100,000 saved. These savings can include your emergency fund, retirement accounts such as a 401(k) or IRA, employer contributions, and long-term investments.

To see how much you should keep in an emergency fund, try this emergency fund calculator.

To reach that number, Fidelity suggests saving 15% of your annual income between your own contributions and any company match. Importantly, these funds should be invested, not left in low-interest accounts, so compounding interest can grow your money.

Other firms, like T. Rowe Price, recommend a more modest benchmark: 1x to 1.5x your annual income by 35. That means someone earning $60,000 should ideally have $60,000–$90,000 in savings. This highlights that income, lifestyle, and personal goals all influence what’s realistic.

So if you’re asking at age 35 how much should I have saved, the best answer is to view it as a range rather than a rigid figure. A sinking fund can also be a useful tool to manage short-term financial goals alongside long-term savings.

Here are the main savings priorities to keep in mind at 35:

- Emergency fund: Aim for at least 3–6 months of monthly spending, though 6–12 months is safer for families or those with dependents. This provides a financial cushion against job loss or unexpected bills.

- 2x income rule: Following Fidelity’s benchmark, target savings equal to two times your salary. For example, an annual income of 500 million VND should translate to about 1 billion VND saved.

- Retirement contributions: Contribute 15–20% of your monthly income to retirement accounts, factoring in any employer match. Starting early is critical since compound growth works in your favor.

- 50/30/20 budgeting rule: Keep 50% of income for needs, 30% for wants, and 20% for savings and debt repayment. Increase the savings portion when your income grows to accelerate progress.

Age 35 is when savings should move beyond just “emergency money” and into serious long-term wealth building. Benchmarks help you gauge progress, but the real goal is creating consistency and growth over time.

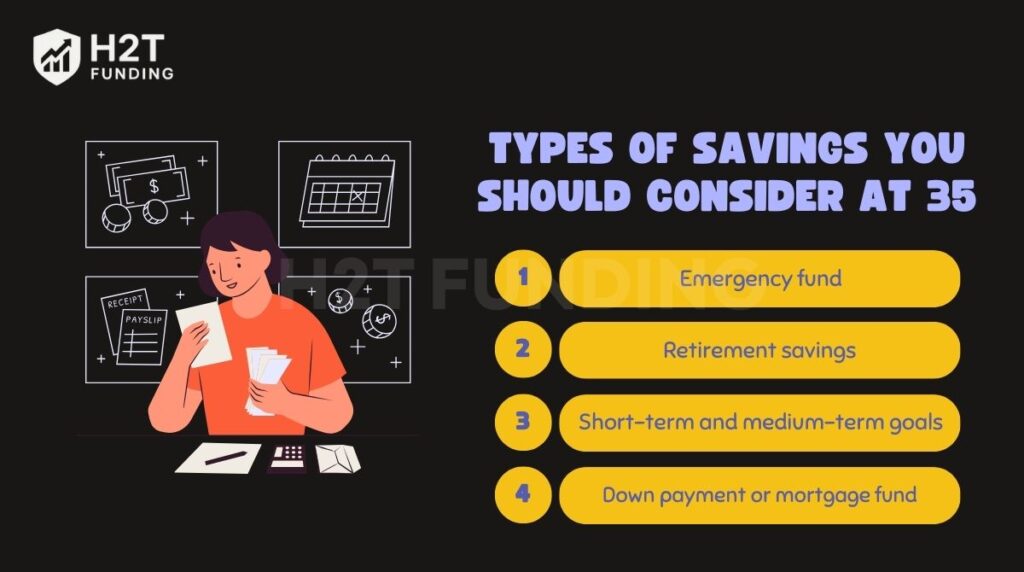

3. Types of savings you should consider at 35

By your mid-30s, savings are no longer just about having a rainy-day fund. At this stage, you need a diversified savings plan that covers emergencies, future security, and lifestyle goals. Here are the main categories to prioritize:

- Emergency fund: Keep at least 3–6 months of living expenses in cash or liquid accounts. For families with children or a single-income household, aim for 6–9 months. This provides stability if job loss, medical bills, or unexpected repairs.

- Retirement savings: Building long-term wealth becomes critical in your 30s. Using accounts like a 401(k) or IRA ensures growth with compound interest, helping you secure retirement income when you reach retirement age. These savings can later supplement Social Security benefits.

- Short-term and medium-term goals: Whether it’s travel, buying a car, or pursuing further education, setting aside a separate fund for these expenses keeps you from dipping into emergency or retirement savings. Planning also reduces reliance on debt.

- Down payment or mortgage fund: For many, the mid-30s is the time to buy a first home. Saving for a down payment not only lowers your loan burden but also prepares you for ongoing maintenance costs, which average several thousand dollars per year.

Well-structured savings at 35 should balance protection, growth, and flexibility. Each category serves a purpose, ensuring you’re financially resilient today and secure for the future. In reality, there’s no single rule for how much savings should you have at 35; it depends on your personal mix of these categories.

See more:

4. What if you’re behind on savings at 35?

First off, if you’re 35 and feel behind on savings, take a deep breath. You are far from alone. Life happens: student loans, unexpected costs, or just starting a bit later. The goal isn’t to panic, but to start making a clear plan.

Here are practical steps to get back on track:

- Increase your savings rate: Start by setting aside 20–25% of your income, even if it means tightening your budget. Consistency will quickly build momentum.

- Optimize spending: Create a clear personal budget to identify leaks in your cash flow. Redirect even small savings into your accounts instead of lifestyle upgrades.

- Automate transfers: Set up automatic deposits to retirement or investment accounts. This makes saving a habit rather than a decision you need to make each month.

Prioritize long-term investing: If you haven’t begun, now is the time. Focus on retirement accounts and diversified investments where compound growth can work for you. If you’re unsure how to allocate funds during times of market volatility, consulting a financial advisor can provide tailored guidance.

The key is to move from worry to action. Even if you’re behind today, disciplined changes in your mid-30s can put you on a strong financial path within a few years.

5. How to boost your savings in your 30s

Your 30s are a prime time to accelerate wealth building. You’re often earning more than in your 20s, but also facing bigger responsibilities. To make progress, you need strategies that combine discipline with growth.

- Save 20–25% of your income: Channel this amount into savings and investments each month. If that feels high, start smaller and increase gradually as your income grows.

- Avoid lifestyle inflation: Resist the urge to upgrade your lifestyle every time your salary rises. Direct bonuses, raises, or windfalls into savings instead.

- Diversify your income: Explore side hustles such as freelance work, small business ventures, or investment opportunities. Additional income streams provide more room to save.

- Leverage financial tools: Use budgeting apps or expense trackers to monitor progress. Seeing your numbers in real time helps you stay accountable and adjust when needed.

These habits can turn your 30s into a decade of financial acceleration, giving you a stronger base of security and freedom as you move into your 40s.

6. Personal factors that influence savings goals at age 35

Savings benchmarks give you a general target, but personal circumstances shape how much you actually need. At 35, your goals depend on several factors that can either accelerate or slow your progress.

- Income and career potential: Your current salary and expected growth matter. Some people may already exceed the average savings for this stage, while others need to play catch-up depending on their circumstances.

- Living costs and location: Housing, utilities, and daily expenses vary widely depending on where you live. Someone renting in a high-cost city may save less than a homeowner in a smaller town, even with the same salary.

- Debt situation: Mortgages, car loans, credit cards, or student debt can weigh heavily on your savings rate. Paying down high-interest balances should often come before increasing contributions elsewhere.

- Family responsibilities: Raising children introduces ongoing expenses like healthcare, school fees, and daily living costs. Parents may also plan for college savings while balancing retirement goals.

- Personal and family goals: Some aim for early retirement, while others prioritize buying property, upgrading a car, or traveling. Each goal changes how much you need to set aside and in what timeline.

- Risk tolerance and investment knowledge: Comfort with risk affects where you put your money. Those open to equities may build wealth faster, while conservative savers may rely more on cash and bonds for stability.

Recognizing these personal factors ensures your savings plan is realistic, flexible, and aligned with your life stage, not just with generic benchmarks.

Read more helpful articles:

7. FAQs

A healthy net worth at 35 often falls between 1.5x and 2x your annual income. This includes savings, investments, and assets minus any debts. The exact number depends on lifestyle and financial goals.

Experts suggest having at least 1x to 2x your salary in retirement accounts by 35. If you earn $70,000, that means $70,000–$140,000 combined from your contributions and employer match.

Yes, but it requires higher savings rates and disciplined investing. Saving 30% or more of your income, combined with a long-term investment plan, can still make early retirement achievable.

It depends on your income and location. For someone earning $40,000 a year, $50,000 is solid. For someone earning $100,000, it may fall short of benchmarks but is still a valuable foundation.

Aim to save 15–20% of your monthly income. If you need to catch up, push this to 25% or more, adjusting your lifestyle to make room for higher contributions.

Yes. Start aggressively by building an emergency fund first, then allocate at least 20–30% of income to savings and investments. Automating contributions makes the process consistent.

A common guideline is 1x–2.5x your annual salary saved in retirement accounts by this age. The closer you are to 2x or above, the more comfortably you’ll stay on track for retirement.

For most people, $5 million is more than sufficient to retire early, provided you manage spending carefully. However, lifestyle, healthcare costs, and market returns all influence how long the money will last.

8. Conclusion

Turning 35 is often seen as a milestone, but it’s never too late to build financial stability. Whether you’re ahead, behind, or just starting, the most important step is to take action now. Consistent saving and smart planning matter more than a perfect number.

So if you’re wondering how much savings should I have at 35, use the 2x income rule as a benchmark, then take consistent action to grow beyond it. Every decision you make today sets the foundation for financial freedom tomorrow.

For more practical tips on saving, investing, and managing money in your 30s, explore the Cash Flow & Saving Strategies section of H2T Funding and start shaping the future you want with confidence.